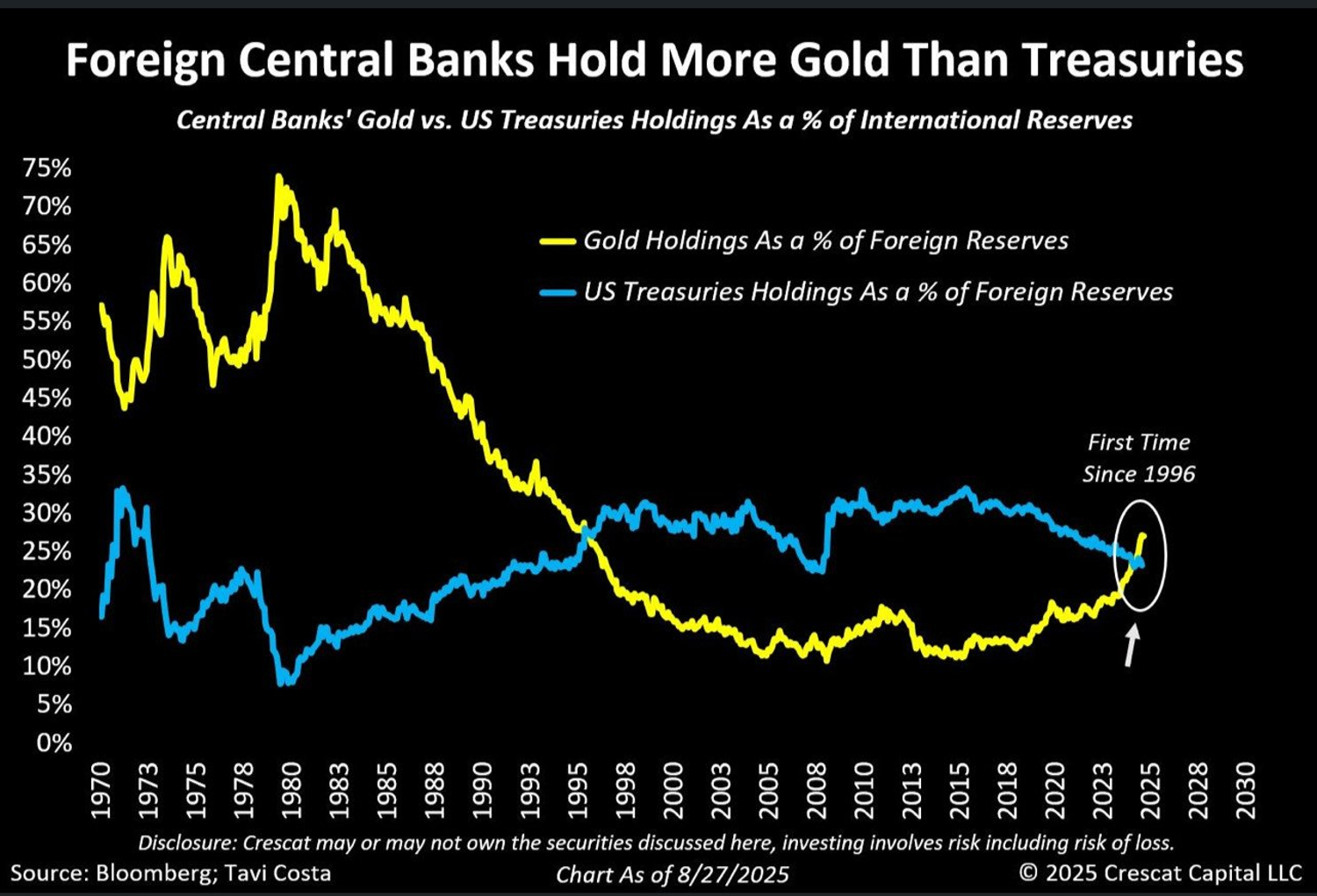

A Landmark Shift: Non-US Central Banks Collectively Turn to Gold

While many investors were still enjoying their summer vacation, precious metals traders had already returned to work early. After four months of consolidation, gold prices showed signs of a trending market. With the arrival of September, the price officially broke through $3,500 per ounce, setting a new all-time high. However, some data hidden behind the price details is even more interesting. After nearly 50 years of weakness, gold's position in central bank balance sheets has rapidly recovered over the past decade. This year, gold officially surpassed US Treasuries to become a higher-ranking asset on non-US central banks' balance sheets for the first time since 1996.

Source: Tradingview

During the Cold War, gold was often the preferred choice of central banks. Government bonds from different countries were difficult to use as collateral or reserves for each other because the risk of war significantly increased the probability of default. In the post-Cold War era, with the expansion of credit money and the development of globalisation, the risk of total war has dropped to an all-time low, leading to a rapid increase in central bank reserves backed by government bonds in the 1990s.

Obviously, government bonds offer numerous advantages: their liquidity far exceeds that of physical gold, significantly reducing the average financing cost and time for central banks. Whether for regulating exchange rates or hedging cross-border financial risks, government bonds are generally a more practical tool than gold. As the dominant force in the international financial system, US Treasuries have become the preferred choice for central banks worldwide.

However, there are two prerequisites for central banks to do so:

- First, the probability of default on US Treasuries is lower than that of other countries. Since US Treasuries surpassed gold in 1995, with the exception of a few extreme cases (such as the 2008 financial crisis), the average duration of US Treasuries has remained above 55 months. Throughout the 2010s, the average duration has consistently remained above 60 months, meaning that the proportion of short-term bonds in the overall debt burden remains relatively low, indicating relatively low credit risk.

- Furthermore, the relative independence of the Federal Reserve is a key consideration for central banks. An independent Fed means that US Treasuries serve as a relatively fair "asset pricing anchor," and interest rates, yields, and even government bonds themselves cannot be fully weaponised for political reasons.

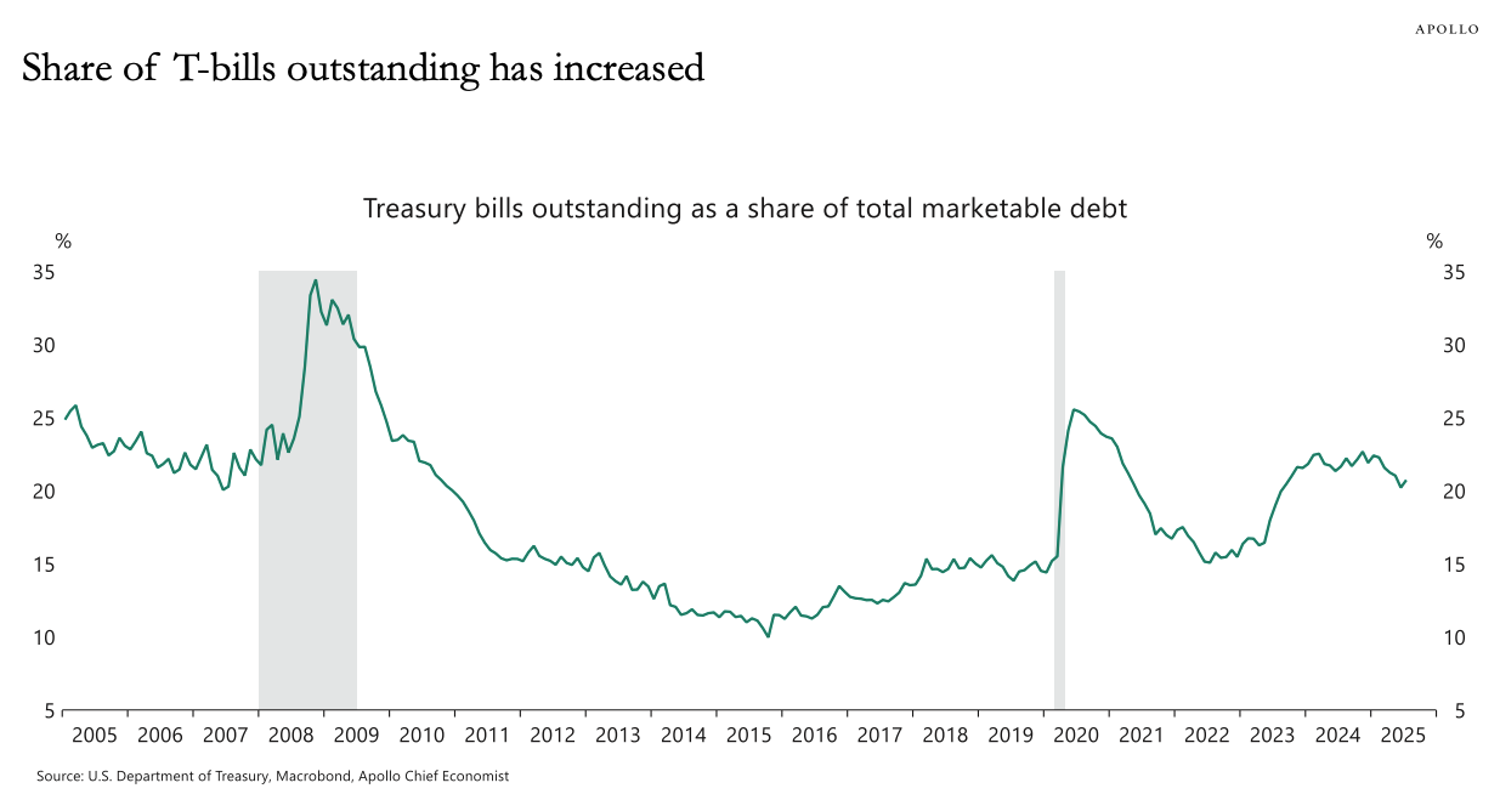

Clearly, the premise above is gradually being shattered under the Trump administration:

- Since 2016, the proportion of T-bills in total marketable debt has been steadily rising. Furthermore, with repeated debt ceiling increases and the passage of the OBBBA Act, this share of T-bills is likely to continue rising for years to come, even exceeding the 2007 level. An increase in the proportion of short-term financing generally indicates a growing risk of debt unsustainability.

- As the Trump administration gradually shifts from "globalisation" to "domestication," the Federal Reserve's independence is also being challenged. By 2026, the Trump administration may gain greater influence over the Federal Reserve, even to the point of influencing monetary policy. Given that the Trump administration is not afraid to weaponise monetary policy and Treasury bonds under the pretext of "national security," non-US central banks need to consider reverting to their former "Cold War paradigm" to ensure their own economic security.

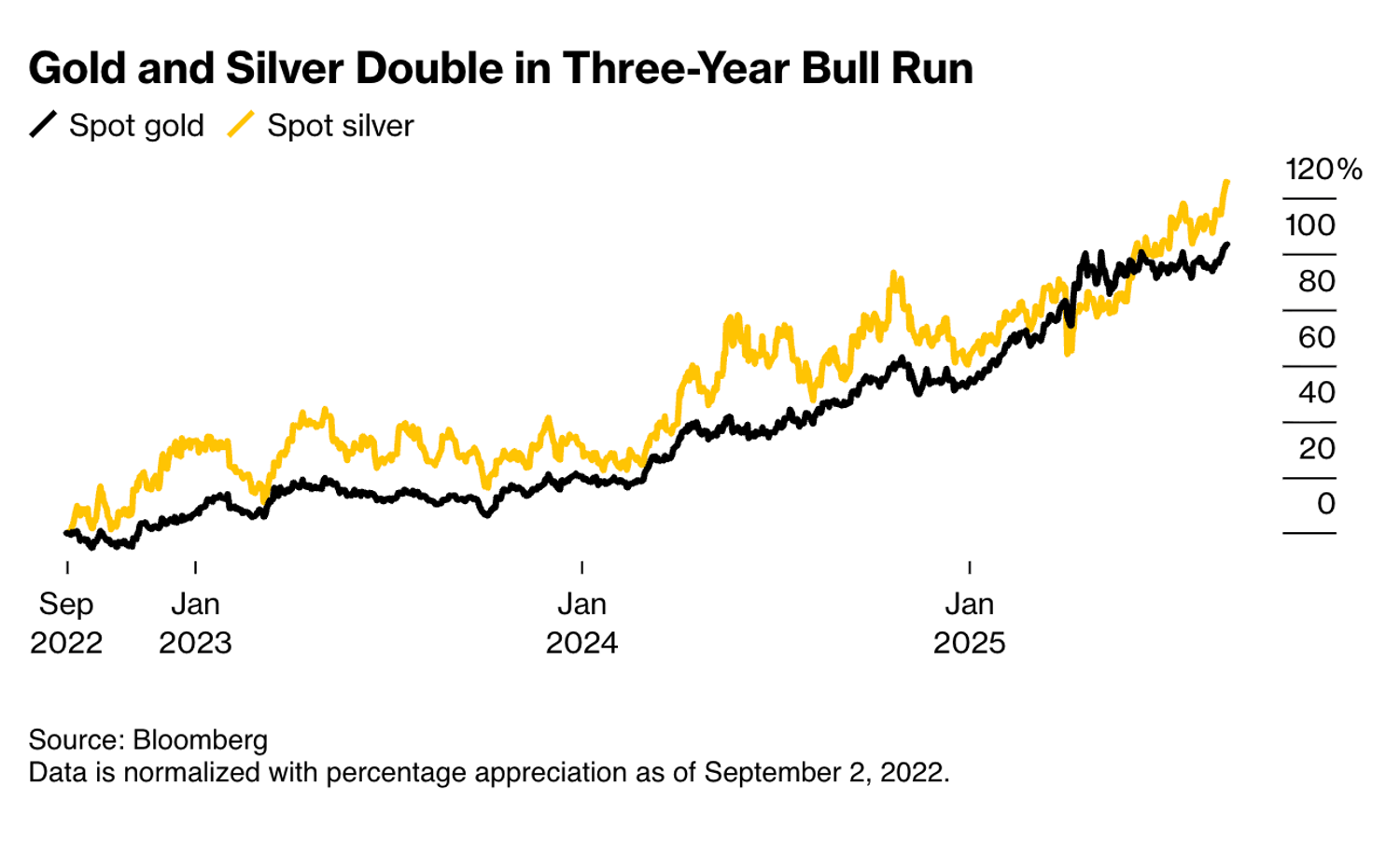

The Trump administration's policies are also further pushing central banks around the world toward a "Cold War paradigm." In a recent Department of the Interior press release, silver was added to the "critical minerals list" for the first time since 2017. Silver has the dual attributes of "store of value" and "industrial application", and the White House's approach has undoubtedly increased investors' attention to the "store of value" attribute of silver and other precious metals.

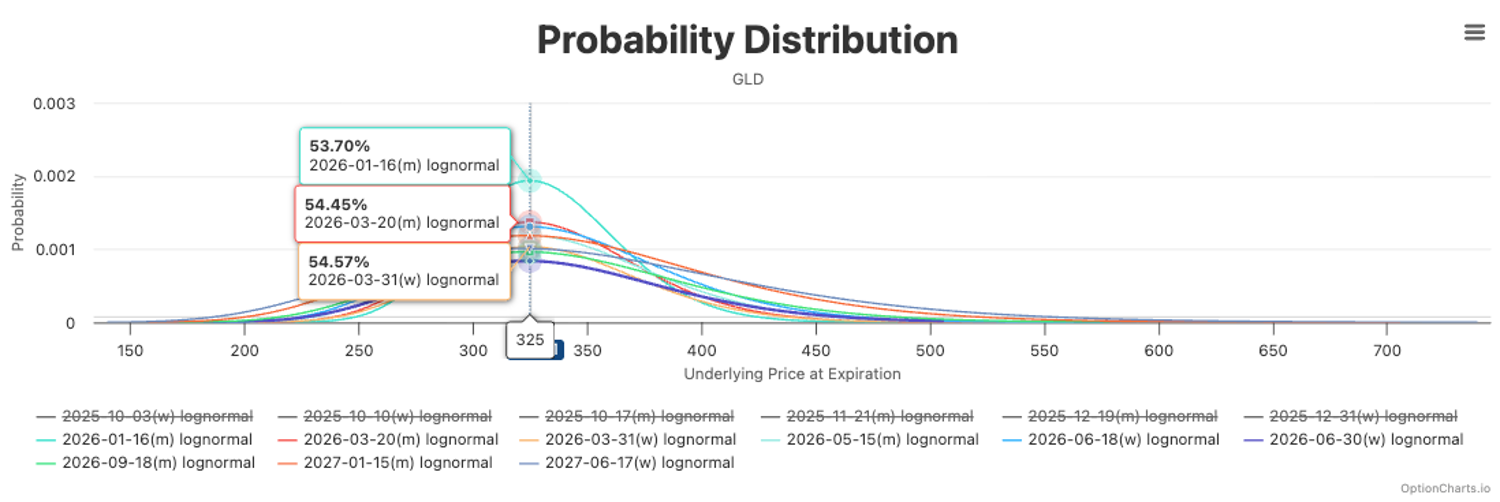

Naturally, derivatives traders have also grasped this trend. As investors flock to gold and silver ETFs, pricing in far-month GLD options has already priced in higher bullish expectations. One implied consensus is that there's about a 55% probability that gold will be higher than its current price in March 2026, and in the worst-case scenario, it won't fall below its level around March 2025. The shift in global central banks' preference is creating a "qualitative shift," injecting upside momentum into gold prices that will last for years, if not longer.

Source: optioncharts.io

Source: optioncharts.io

Will “Digital Gold” Also Benefit?

Let's turn our attention back to Bitcoin. As "digital gold," the precious metal's resurgence has also provided strong support for Bitcoin's price. As central banks increasingly favour holding more gold, and gold prices rise, investors are actively seeking "gold alternatives" to hedge against the risk of the US dollar and US Treasury bonds. Unlike physical gold, Bitcoin's offshore nature and improved liquidity lend it additional appeal, making it an emerging option for hedging bond risks.

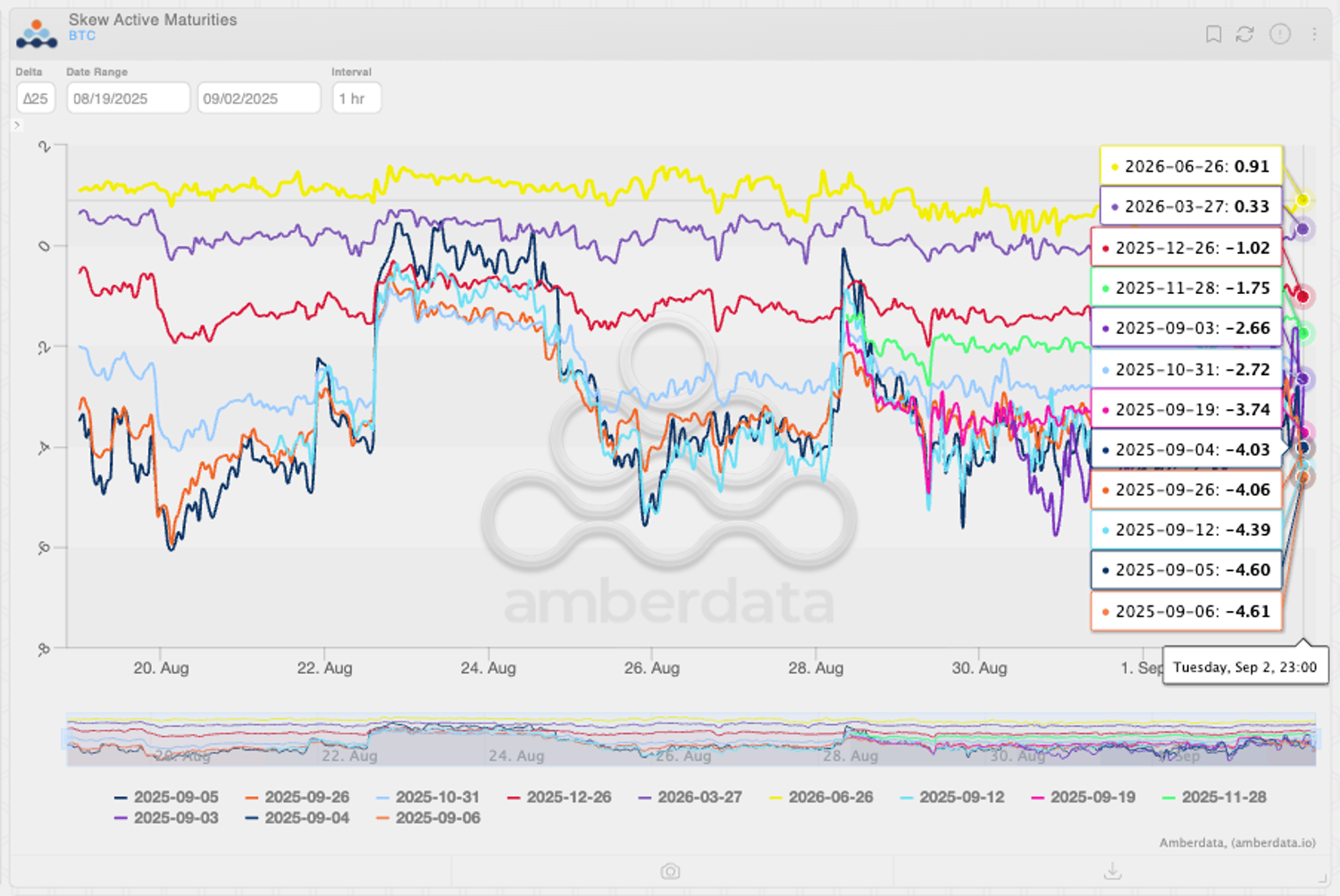

Source: Amberdata Derivatives

Interestingly, derivatives traders haven't shown the same bullish sentiment towards Bitcoin as they do towards gold. Implied expectations in the options market suggest that traders don't anticipate Bitcoin's appreciation in the coming months, while showing significant bullish sentiment towards gold.

Source: Amberdata Derivatives

BTC's high leverage relative to gold may be one source of traders' caution: Due to this significant leverage, Bitcoin's price has already reached its target level significantly ahead of gold, resulting in a lack of momentum for further gains. Furthermore, leverage itself can be considered an inherent property of Bitcoin. This means that when market leverage is high, BTC's safe-haven and store-of-value properties become obscured, while the unwinding of leverage helps to highlight these two properties.

Therefore, in the long term, BTC will continue to benefit from continued increases in precious metal prices due to similar fundamentals. However, unlike precious metals, BTC's hedging capacity in a portfolio depends mainly on its current leverage level, which requires relatively higher timing and leverage management skills. Taken together, BTC may still be the preferred choice for investors with a relatively high risk appetite, while precious metals are more suitable for the general public.

Economic Calendar of This Week

Tuesday 09:00

- EU Inflation Rate YoY Flash

Tuesday 14:00

- US ISM Manufacturing PMI

Wednesday 14:00

- US JOLTs Job Openings

Thursday 14:00

- US ISM Services PMI

Friday 06:00

- UK Retail Sales MoM

Friday 12:30

- US Non-Farm Payrolls

- US Unemployment Rate

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.