When a crypto investor manages to sell Bitcoin at a market peak, the next challenge is deciding where to park those profits. The goal shifts from aggressive growth to wealth preservation, keeping the hard-earned gains safe from volatility and erosion.

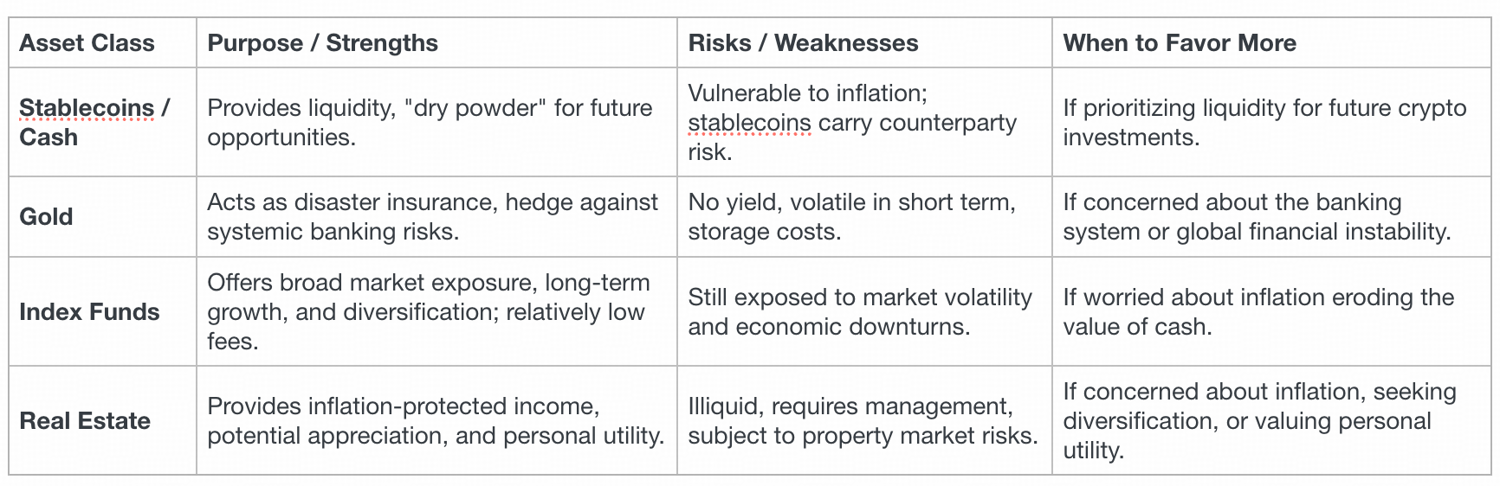

Four popular asset classes often considered are stablecoins, gold, index fund, and real estate. Each offers a different mix of stability, risk, liquidity, and inflation protection. In this article, we provide an overview of each asset class, examine their pros and cons for someone coming out of crypto.

Stablecoins

For a crypto investor, stablecoins essentially act as a digital equivalent of cash, a place to store value without the wild swings of Bitcoin or other coins.

If you wish to remain in the crypto ecosystem, stablecoins are convenient. You can quickly convert Bitcoin into a stablecoin like USDT/USDC on exchanges to lock in gains. Your wealth stays on-chain, ready to deploy in the next opportunity without going through banks.

Unlike holding cash in a zero-interest account, stablecoins can be put to work. Crypto platforms and DeFi protocols allow lending, staking, or providing liquidity with stablecoins to earn interest. In addition, there are now on-chain treasury products that provide yields in the 3%–4% range.

Related Reading: What are Stablecoins?

Despite their stability, stablecoins carry specific risks and downsides for those looking to preserve wealth.

Stablecoins are tied to fiat currencies, so while they avoid crypto volatility, they also inherit fiat currency inflation. If the USD loses purchasing power (say 5% inflation per year), a USD stablecoin will similarly lose real value. Over years, sitting purely in stablecoins could erode your crypto gains in real terms. They preserve nominal wealth, but do not appreciate on their own. Any growth would have to come from external yields, which may or may not outpace inflation.

Gold

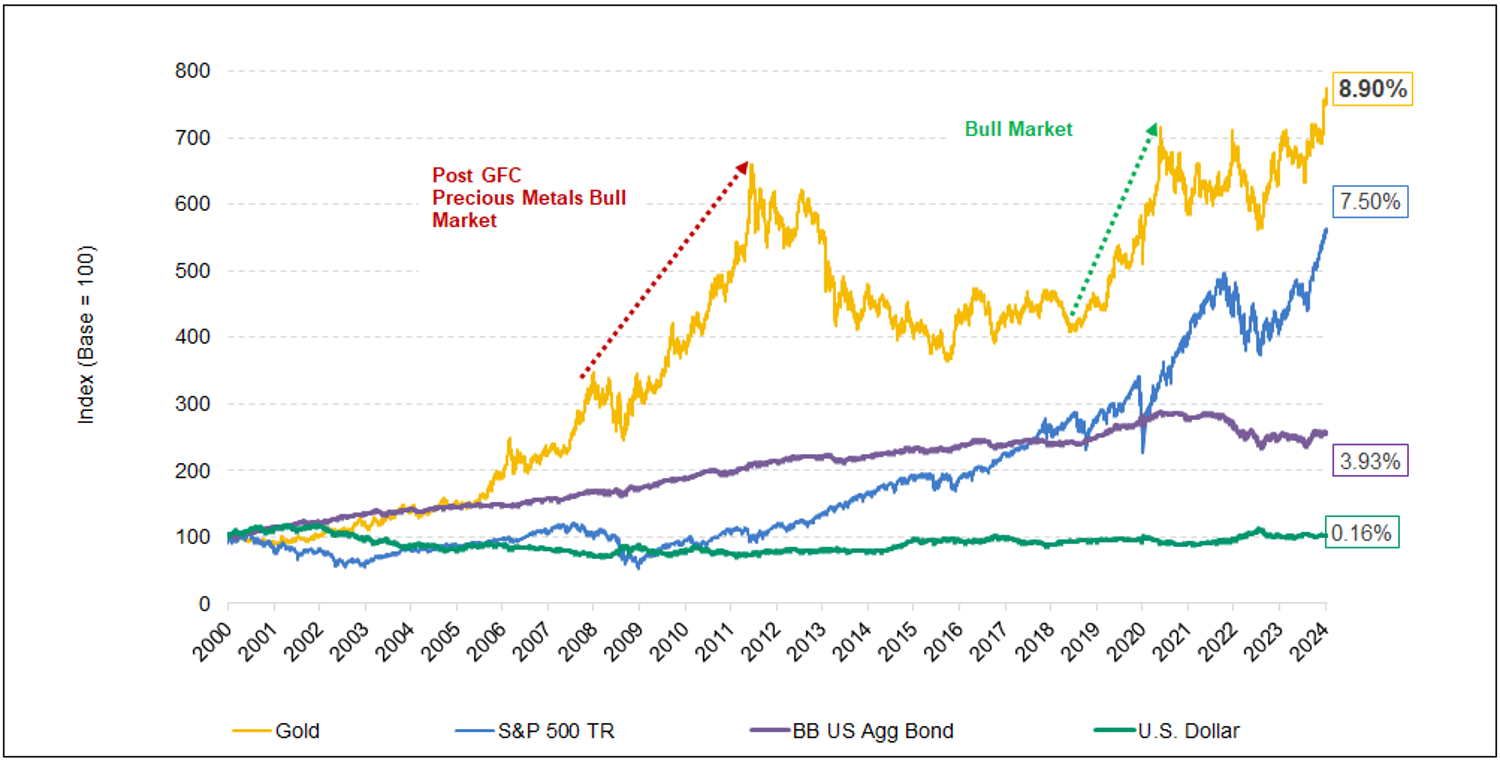

Gold has a track record measured in centuries. It tends to hold its purchasing power over the very long term. For example, despite short-term fluctuations, gold’s value today reflects massive gains since the gold standard era, since 1971 (when the dollar’s link to gold was cut), gold’s price has risen about 8–10% annually on average, well above cumulative inflation in that period. Many turn to gold during times of currency debasement or economic crisis, as it often retains value when paper assets fall. In short, gold can anchor a portfolio with something that doesn’t rely on any government or tech.

Source: https://sprott.com/insights/us-dollar-decline-and-fall/

Gold often moves differently from stocks or crypto. It adds diversification. When stock markets are crashing or when crypto is in a bear market, gold has sometimes risen or remained stable. For a crypto investor now seeking stability, gold can be a way to diversify wealth out of the digital realm. It isn’t perfectly stable (gold has its own cycles), but it’s generally less volatile than crypto and has distinct drivers (e.g. real interest rates, central bank buying).

If you hold physical gold in your possession, there is no issuer that can default. Gold coins or bars in a safe are under your control. This self-sovereignty may appeal to Bitcoin holders who value “hard” assets. Gold cannot be hacked or erased by a computer error. It’s an asset outside of the banking system, which could be comforting if one is wary of keeping all funds in banks or in digital form.

There are several tokenized gold products in the crypto market, allowing investors to gain gold exposure without leaving the crypto ecosystem.

Related Reading: Tokenized Gold and Yield Opportunities

Cons for Gold

No Yield or Cashflow

Gold is often dubbed a “pet rock” in that it does not produce income, dividends, or growth by itself. This means that unlike stocks or real estate which can generate earnings or rent, gold relies purely on price appreciation to match inflation.

Short-to-Medium Term Volatility

While gold is less volatile than cryptocurrencies, it is by no means a stable price. It can swing significantly with market sentiment. For example, from 2011 to 2015, gold’s price fell roughly 40% from its then-high. If you buy gold right after selling Bitcoin, there is a risk that gold’s price could decline in the short run, trimming your wealth.

Storage and Security Costs

Holding physical gold securely requires arrangements. Large amounts of gold are bulky and heavy. You’ll likely need a safe or bank vault. There are costs for storage and insurance. If storing at home, you must consider theft risk. If using a bank or vault service, you incur fees and trust that custodian. These factors eat into the convenience and net returns.

Real Estate

Real estate is typically considered a stable, slow-growing asset that provides income (rent) and is often resilient to inflation. It’s also an emotionally satisfying asset, owning your home or land can provide a sense of security that abstract financial assets might not.

Real estate tends to perform well in inflationary environments. As the price of goods and wages rise, rents also usually rise, which increases the income from property. Property values themselves often climb with inflation, partly because replacing a house (construction materials, labor) gets more expensive. Historically, housing prices have roughly kept pace with or slightly exceeded inflation in many markets.

Real estate can generate regular income if rented. The rental yields on property might range from, say, 3% to 8% of the property value per year depending on location and type. This can provide a steady cash flow, effectively turning your crypto gains into a passive income stream. Moreover, real estate uniquely allows for leverage: you can use a mortgage to buy a more valuable property than the cash you put in. For instance, a 20% down payment lets you control a 100% asset. If the property value rises, your equity grows disproportionately (though leverage also magnifies losses, it has historically been a tailwind in stable/growing markets).

Cons for Real Estate

Illiquidity

Real estate is notoriously illiquid. Selling a property can take months, involving listing the property, finding buyers, negotiating, inspections, and paying fees. If you needed to quickly liquidate to access cash, you cannot count on a quick sale without possibly discounting the price significantly. This lack of liquidity is a serious consideration for wealth preservation, you shouldn’t put funds in real estate that you might need on short notice.

High Transaction and Holding Costs

The costs associated with buying and selling property are high. Closing costs, legal fees, real estate agent commissions (often 5–6% of the property price when selling), transfer taxes, etc., can take a significant bite. If you purchase property and then need to sell in a few years, these costs can eat up any appreciation unless the market rose substantially. Additionally, holding real estate isn’t free: there are property taxes, maintenance and repairs, insurance. These ongoing expenses mean real estate wealth can slowly leak if not managed.

Management and Hassle

Owning real estate, particularly rental property, can be management-intensive. If you rent out a home or apartment, you may have to deal with tenants (vetting them, handling late payments, or even legal evictions), maintenance calls at odd hours, and vacancies. You can hire property managers, but that incurs further cost (typically 8-10% of rent). Even owning your own home requires effort, repairs, renovations, etc. This is very different from holding a passive asset like an index fund.

S&P 500 Index Fund

Crypto investors who have cashed out may consider the S&P 500 index fund as a cornerstone for wealth preservation. The S&P 500 is a stock market index of 500 of the largest U.S. companies, spanning diverse industries and serving as a broad gauge of the U.S. economy. Investors can invest in low-cost index funds or ETFs that track the S&P 500’s performance. This provides an easy, passive way to get exposure to the overall stock market’s growth with a single investment, backed by decades of historical data and market performance.

An S&P 500 index fund instantly spreads your investment across hundreds of leading companies, reducing the impact of any single stock’s decline. The index has a long track record of growth. Historically it has delivered around 10% average annual returns (about 6–7% after inflation) over many decades.

S&P 500 index funds (whether mutual funds or ETFs) are highly liquid, you can buy or sell on any trading day and convert your holdings to cash easily.

Cons for S&P 500

Short-Term Volatility

While safer than crypto, S&P 500 funds still experience market swings. In the short to mid term, stock values can drop significantly during market corrections or recessions, for instance, the index plunged nearly 57% during the 2007–2009 financial crisis. Although every major S&P 500 downturn in history has eventually been followed by a recovery, it can take years to bounce back. This means a S&P 500 investment is best suited for a longer time horizon; if you might need the cash in the very near term, market downturns could temporarily erode your wealth.

Moderate Returns

The flip side of lower risk is moderate upside. An S&P 500 index fund is designed for slow-and-steady growth, not explosive gains. Earning 7–10% per year (on average) may feel slow to those used to crypto’s potential for rapid doubling, but it reflects a deliberate trade-off. The index fund prioritizes capital preservation and gradual growth.

Market Dependence

The S&P 500’s performance hinges on the U.S. economy and corporate earnings. A broad index fund won’t protect you from systemic market downturns, if the overall market struggles, your fund will likely dip as well. Additionally, the index today is somewhat top-heavy (a large portion of its value is in a few big tech companies), which can introduce concentration risk.

Conclusion: Choosing the Right Mix for Preservation

Selling Bitcoin at the top is a big win, and the priority becomes not losing those gains. Each of the assets discussed (stablecoins, gold, index fund, real estate) can play a role in a wealth preservation strategy, but none is a perfect one-size-fits-all solution. The best choice depends on your personal needs, time horizon, risk tolerance, and plans.

A prudent approach to wealth preservation after a crypto windfall is often diversification. Each asset class has distinct strengths and weaknesses, and by combining them, you can capture a more balanced profile. For example, you might hold a core of stable assets (some stablecoins or cash for liquidity, some gold for disaster insurance), a healthy allocation to index fund for growth and income, and perhaps some real estate for inflation-protected income and personal use or diversification.

The exact mix can be tailored: an investor worried about the banking system might favor more gold and real estate; someone who wants dry powder for future crypto investments might keep more in stablecoins.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.