Introduction

Hyperliquid is a decentralized exchange specializing in perpetual futures trading and built on its own high-performance Layer-1 blockchain (known as HyperEVM). The platform offers ultra-fast transactions, low fees, and advanced trading tools, all while maintaining on-chain transparency and user control.

Launched in 2023, Hyperliquid quickly gained traction in the crypto trading community. It forwent venture capital funding and instead embraced a community-driven approach, allocating the majority of its tokens and revenue back to users. This strategy, coupled with its technical prowess, led to rapid growth.

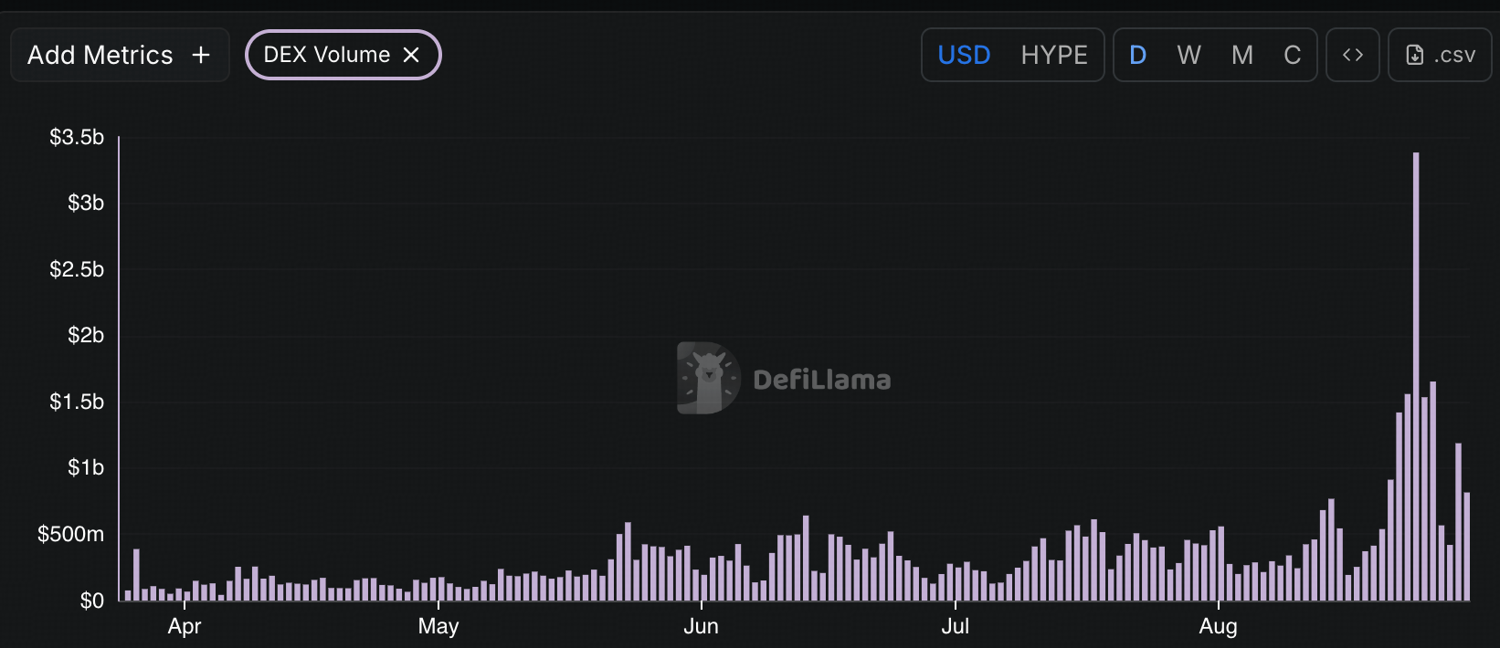

HyperLiquid DEX Volume

Source: https://defillama.com/protocol/hyperliquid?tvl=false&events=false&dexVolume=true

Core Features

Hyperliquid’s core product is its on-chain order book exchange, complemented by a suite of advanced trading features designed for professional-grade performance.

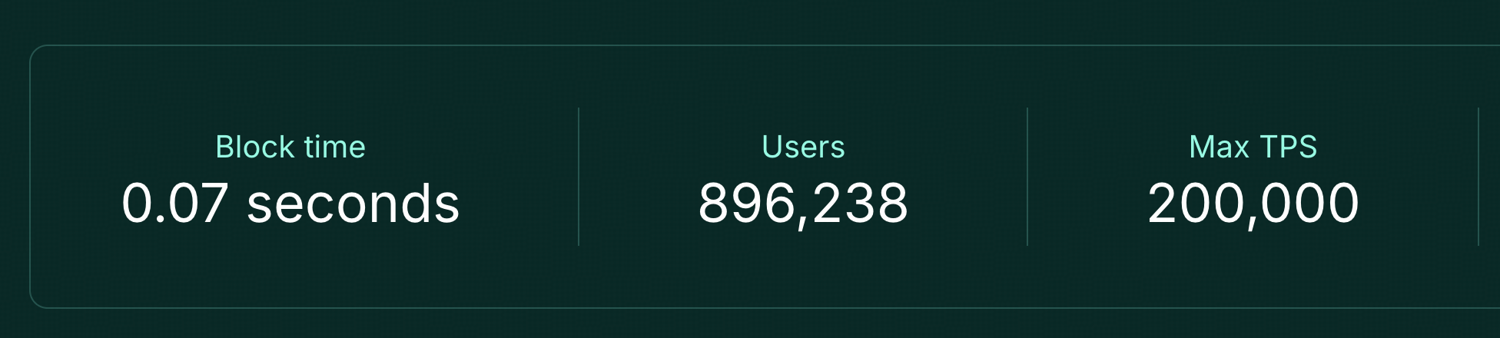

On-Chain Order Book & High Throughput: All orders and trades are processed on-chain via a central limit order book (CLOB), enabling real-time, transparent trading. The custom Hyperliquid blockchain achieves extremely high throughput, handling up to 100,000 orders per second with sub-second finality. A proprietary consensus (HyperBFT) underpins this performance, allowing 0.07 second block times and up to 200,000 transactions per second capacity. This ensures minimal latency for trading.

Source: https://hyperfoundation.org/

Trading Features: The exchange supports up to 40× leverage on perpetual futures and offers a variety of order types and risk controls. Traders can choose from market, limit, stop-market, stop-limit orders, as well as more sophisticated options like scaled orders and TWAP (time-weighted average price) execution. A decentralized clearinghouse manages positions with both cross-margin and isolated-margin modes, giving users flexibility in collateral usage while mitigating liquidation risk. Price oracles update every 3 seconds to ensure accurate pricing for margin and liquidation calculation.

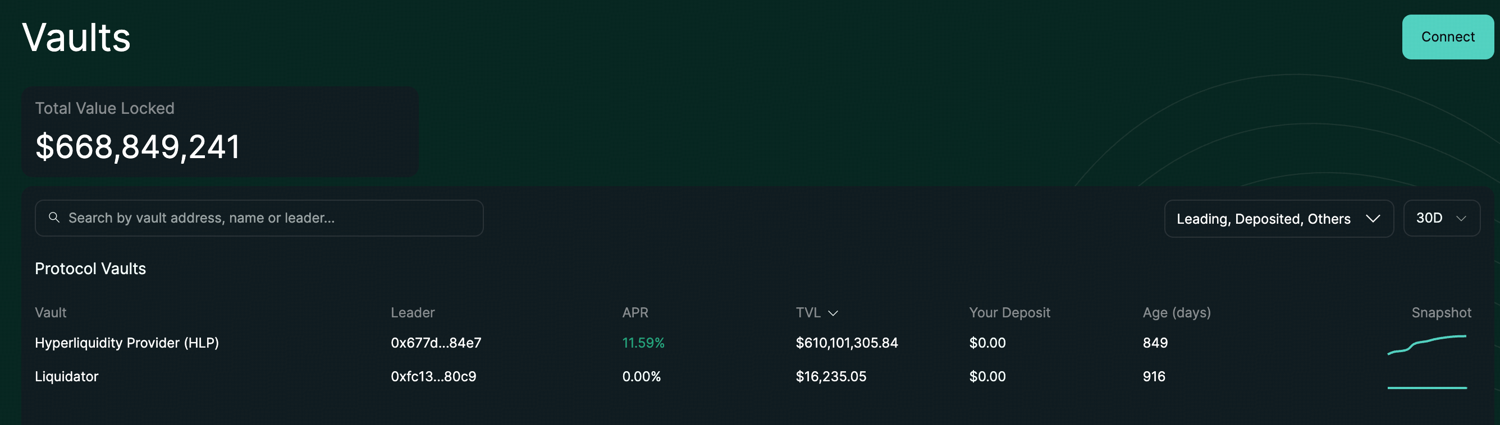

Vaults and Liquidity Provision: Hyperliquid introduces an vault system to market making and yield generation. The Hyperliquidity Provider (HLP) vault is a protocol-run pool that engages in market-making and liquidation backstopping on the exchange. Users can deposit USDC into HLP to earn a portion of trading fees and liquidation profits, effectively tapping into strategies typically reserved for professional market makers. HLP is community-owned (no special fees for the protocol) and allows the community to collectively provide liquidity. This vault system provides opportunities for passive yield (up to 15–24% APR ) while strengthening the overall liquidity on the exchange.

Source: https://app.hyperliquid.xyz/vaults

Security and Decentralization: Hyperliquid’s blockchain currently operates with a limited set of validators which helps maintain high performance. While this design trade-off has drawn some critiques about centralization, it is a deliberate choice to ensure speed, and the network is steadily moving toward further decentralization.

Spot Markets: The platform has also expanded beyond derivatives into spot trading, users can trade major spot crypto pairs on Hyperliquid’s order book DEX alongside perpetual futures.

In summary, users benefit from fast order execution, deep liquidity, and advanced trading tools, all while retaining custody of their assets and avoiding the need for intermediaries.

Tokenomics

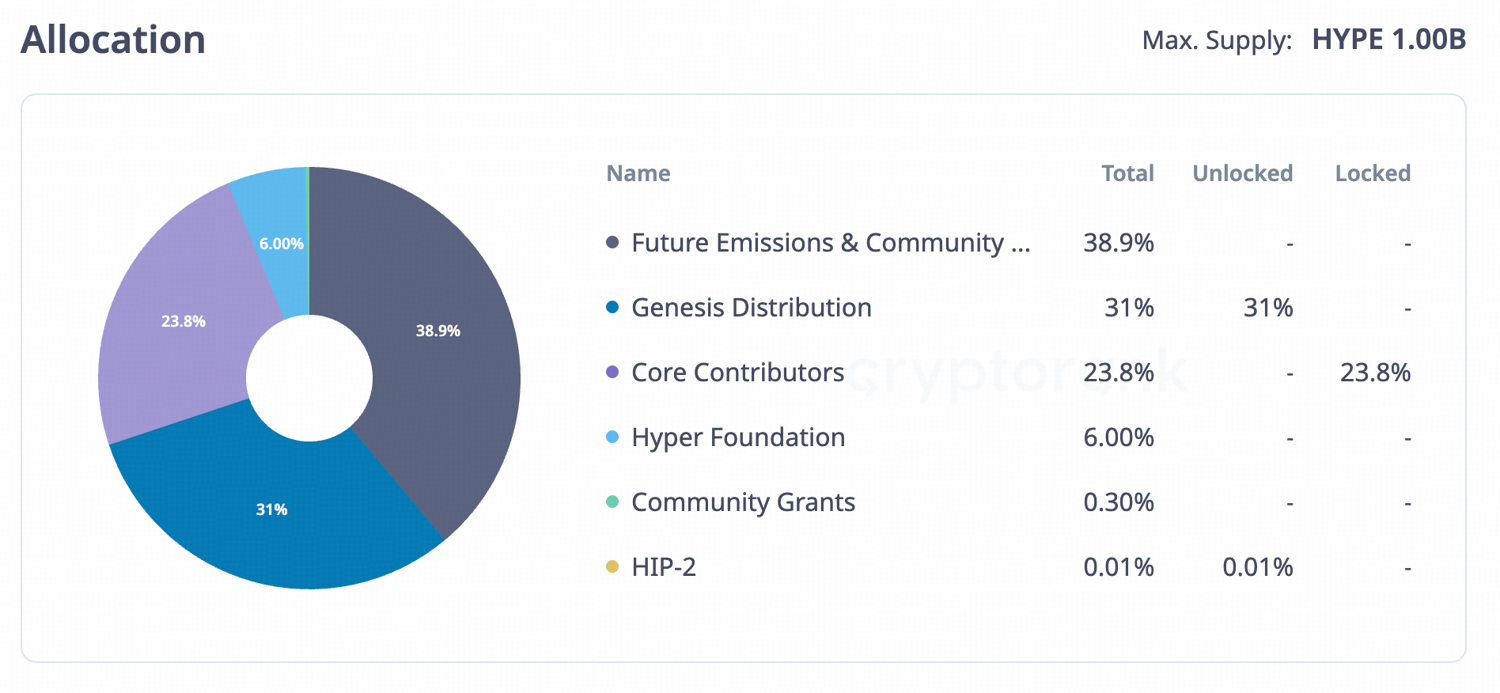

Hyperliquid’s token distribution was deliberately designed to favor the community and long-term development, with no allocations to private investors or venture capital. The total supply is fixed at 1,000,000,000 HYPE. The allocation breakdown is roughly as follows:

Community: 70% – The vast majority of HYPE is allocated to Hyperliquid community. This included a genesis airdrop of 31% of the supply (310 million HYPE), which was distributed to around 90,000 early users of the platform. The remainder of the community allotment (39% of supply) is reserved for future user incentives, liquidity mining, and other community programs to grow the ecosystem. By avoiding any token sale and giving tokens directly to its user base, Hyperliquid ensured its community owns a significant stake in the network’s success.

Core Contributors and Foundation: 30% – Approximately a quarter of the supply is allocated to Hyperliquid’s founders, developers, and core contributors. Importantly, these team tokens are subject to a long-term vesting schedule and did not begin vesting until late 2025, with full lock-up through 2027–2028.

Source: https://cryptorank.io/price/hyperliquid/vesting

Token Buyback Program

Hyperliquid directs 97-99% of its protocol revenue, primarily from trading fees on perpetuals and spot markets, directly to an on-chain entity called the Assistance Fund. The Assistance Fund uses the accumulated revenue to periodically purchase $HYPE tokens from the open market. These buybacks occur automatically and are designed to provide consistent demand pressure on the token.

Risks: Market Manipulation Incidents

Hyperliquid has experienced high-profile market manipulation incidents that expose risks in its model. In two major events in 2025 (the JELLY token incident in March and the XPL token short squeeze in August), opportunistic whales exploited low-liquidity markets on Hyperliquid, causing massive position liquidations and raising questions about the platform’s risk controls and decentralization.

The XPL Short Squeeze: Low Liquidity + High Leverage = Mass Liquidations

In the most recent incident in August 2025, four whales built large long positions in XPL, the token of a new blockchain project. With only about $5 million in capital, they cleared out Hyperliquid’s shallow order book, sending the price from $0.60 to $1.80 within minutes. This 200% price spike forced short sellers into rapid liquidations, wiping out positions worth tens of millions. The episode revealed how easily a thin market can be manipulated when combined with leverage.

- Root Causes: Thin Markets and Whale Dominance

- Low-cap tokens + high leverage created fragile markets where small amounts of capital could drive extreme moves.

No strict position size limits allowed whales to dominate open interest, leaving the order book vulnerable to coordinated manipulation.

A fully decentralized perps exchange in theory would rely only on algorithmic rules and open markets, with “code is law” even in chaotic scenarios. That ideal took a hit in these cases. If Hyperliquid had not intervened on JELLY cases, its HLP vault and many user accounts might have been wiped out, possibly bankrupting the exchange’s liquidity pool. Yet intervening meant undermining the promise of trustless trading.

This dilemma is now at the forefront for all perps DEXs: how to incorporate robust risk controls (position limits, circuit breakers, liquidity requirements, etc.) without relying on ad-hoc centralized actions.