Summary

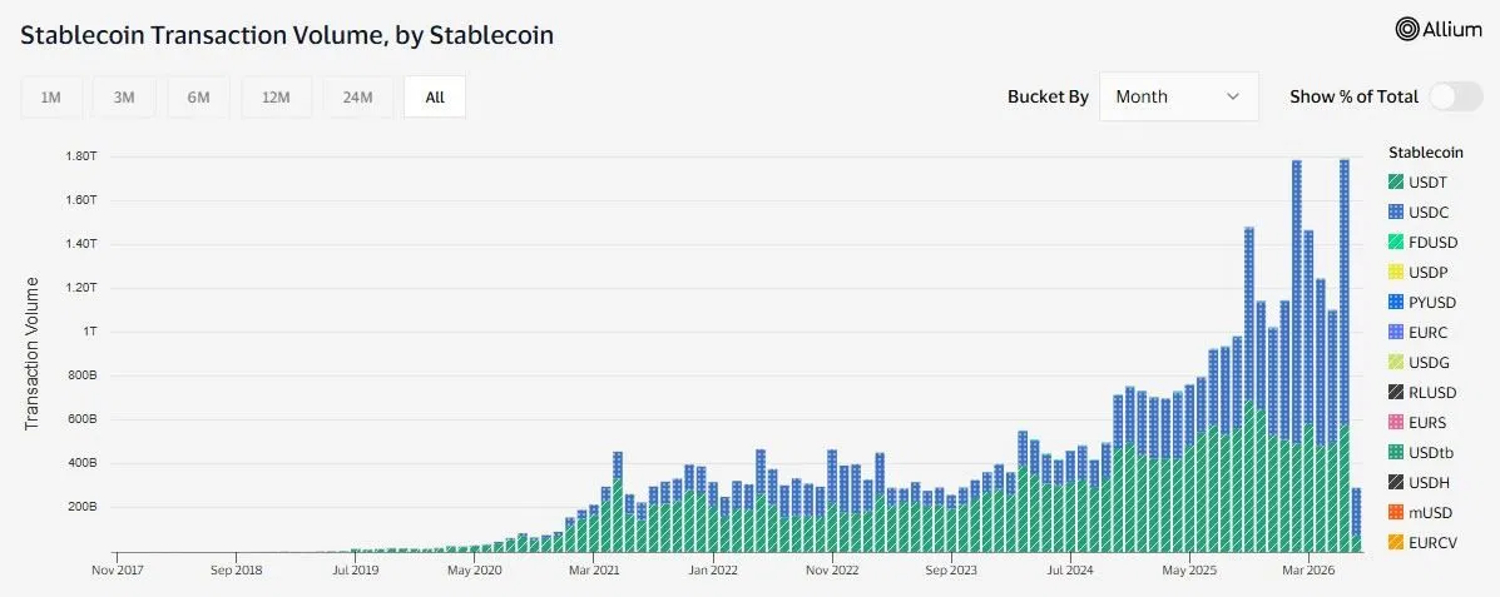

- Tokenized RWAs have jumped roughly 930% in three years to over $33B. Stablecoins settled a record $1.79T in June even as market cap contracted, a near-term squeeze inside a structural uptrend.

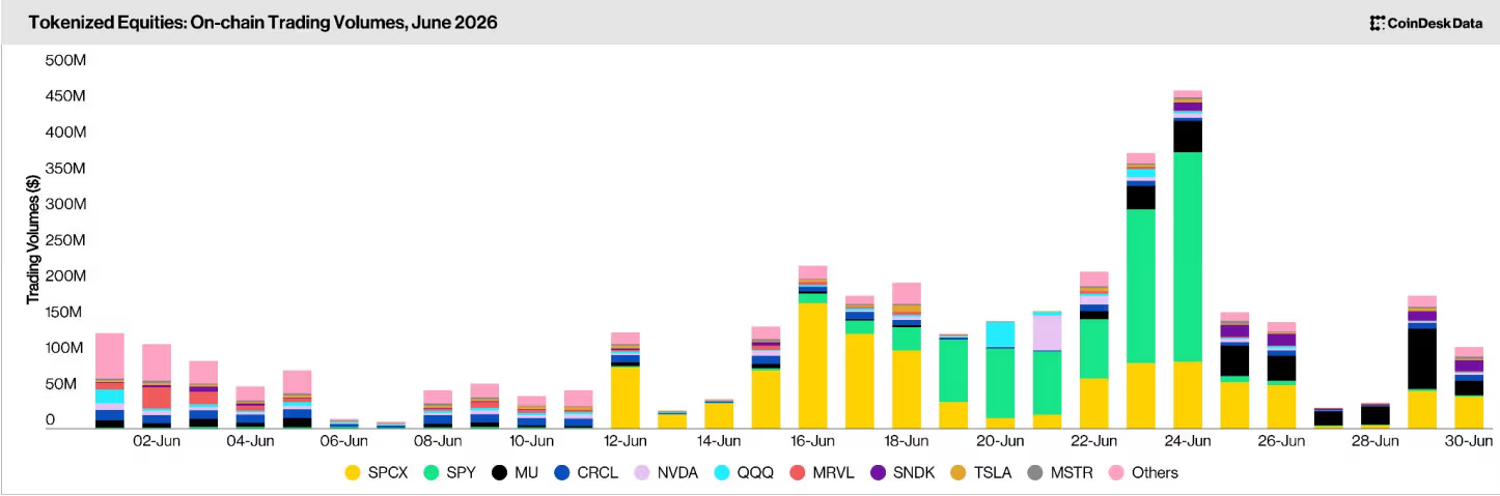

- The asset base is broadening fastest in stocks and commodities. Tokenized equity volume hit a record $3.86B in June (up 145%), led by the SpaceX IPO, while tokenized gold and oil rode 2026's macro shocks, bringing TradFi onchain at speed.

- That demand shows up most clearly in derivatives. RWA perpetuals topped $100B in monthly volume for the first time in June, roughly 5x January, yet sit at just 6.2% of all perp volume, leaving a long runway ahead.

Stablecoins: A Cyclical Squeeze in a Structural Uptrend

Stablecoins are simply tokenized fiat, and they are the largest and most proven real-world asset onchain.

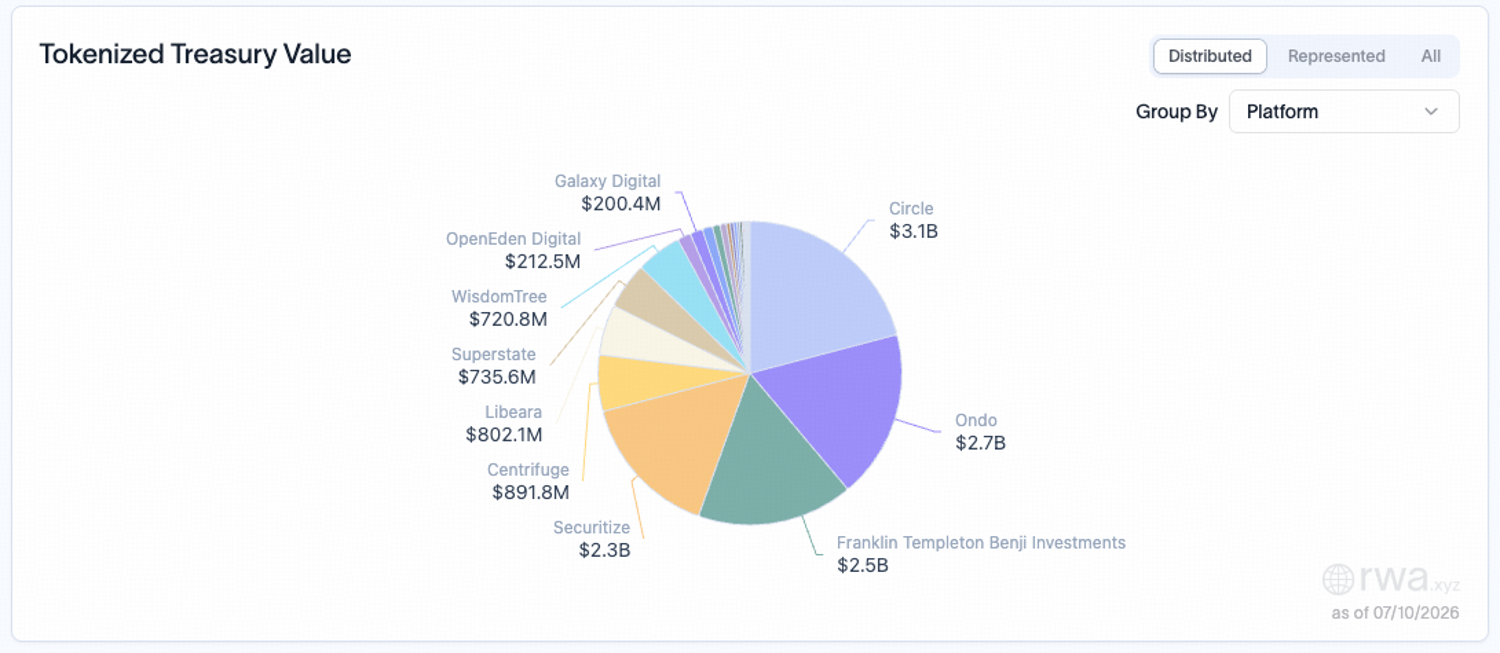

Tokenized RWAs now sit above $33B in distributed value, up from under $3B three years ago, a roughly 930% jump. What began as a Treasury-only trade now spans more than ten asset classes.

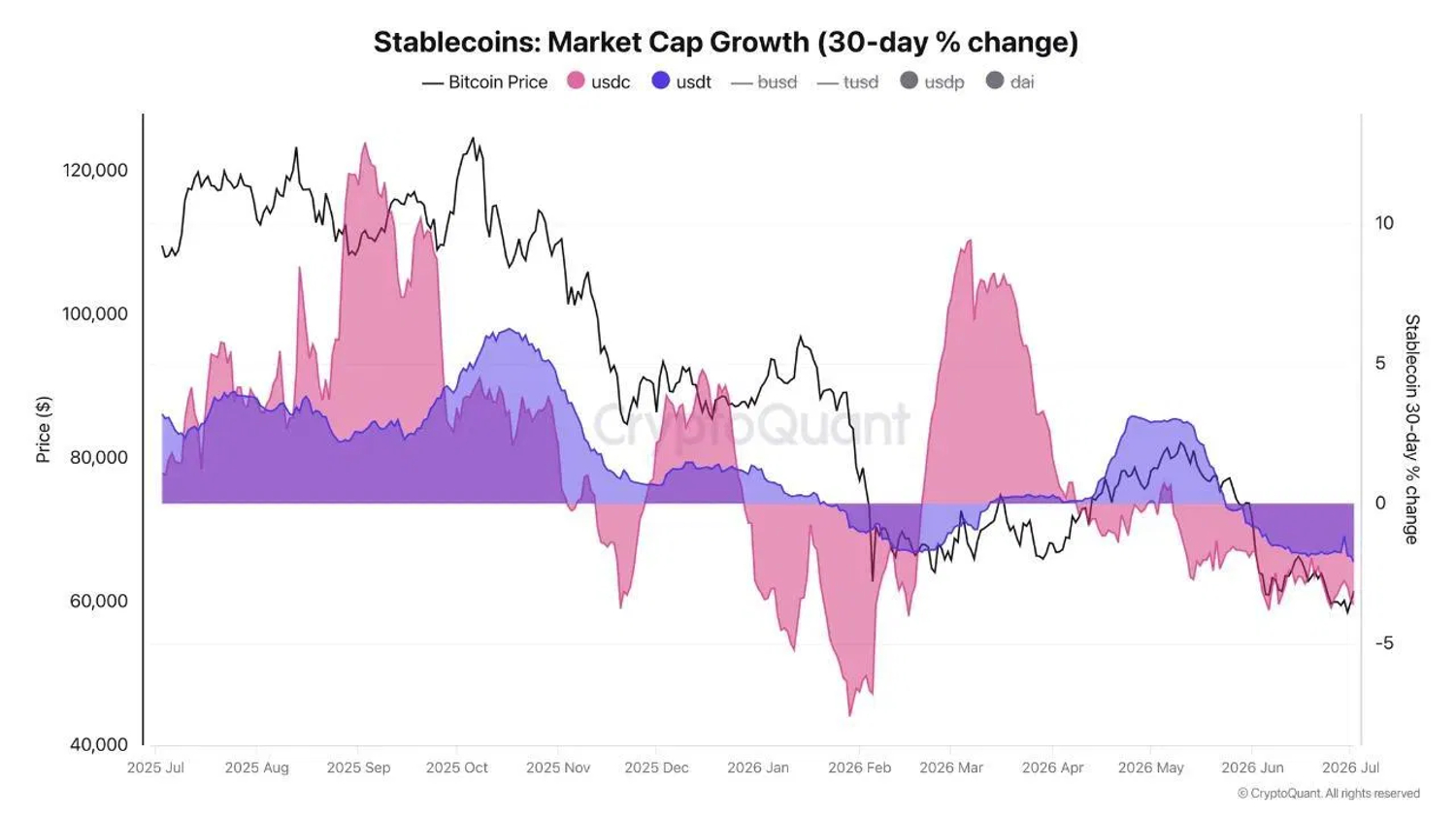

With BTC at a fresh 2026 low, two stablecoin readings look contradictory on the surface.

- On supply, liquidity is draining. USDC and USDT market caps fell 3.6% and 2% over the past 30 days. Shrinking supply means the dry powder available to bid crypto is leaving the on-ramp, consistent with the ETF outflows.

- On flow, activity hit a record. Adjusted stablecoin transaction volume reached $1.79T in June, up 63% from May and 125% year on year, the biggest month ever.

Supply is contracting because speculative capital is exiting risk. Volume is climbing because stablecoins are increasingly used for payments, cross-border transfer, and settlement, utility that grows even in a bear market.

A clear June example is prediction markets. The FIFA World Cup drove combined Kalshi, Polymarket, and Polymarket US volume to $44.8B, up 75% from May, most of it settled in stablecoins.

The supply squeeze is cyclical; the growth story is structural.

Even after this pullback the sector sits above $310B, and forecasters see a far larger base ahead. Standard Chartered projects $2T by 2028; Citi models $1.9T by 2030 base case and $4T in a bull case.

Recent examples of the issuer base broadening:

- OUSD. In June a consortium of 140+ firms (Visa, Mastercard, Stripe, BlackRock, Coinbase) unveiled a yield-sharing stablecoin governed collectively rather than by a single issuer.

- Robinhood. Building its own on-chain rails and distributing USDG through the Paxos-led network.

- Bank of Korea. Pushing for won-stablecoin legislation under a bank-led model.

The near-term supply contraction reflects a weak spot bid, but the longer-term direction points to structural growth in stablecoin adoption.

The Five Assets Tokenizing Fastest Onchain

As stablecoins prove the model, both use cases and asset types are broadening fast. Five real-world assets are moving onchain quickest.

- US Treasuries

At roughly $15 to 17B, tokenized Treasuries are the largest and most mature category.

They offer what stablecoins can't: onchain yield with government-grade safety. This is the category that brought institutions onchain.

- Private credit

It offers higher yields than Treasuries, while tokenization adds liquidity to an asset class historically locked up for years. Positions become transferable, usable as collateral, and redeemable onchain.

- Stocks and ETFs

Tokenized equities exploded from May onward on the back of the AI-fueled equity boom. June onchain equity volume hit a record $3.86B, up 145% from May.

The catalyst was SpaceX IPO driving $1.19B of that volume alone, roughly 31% of the month, as traders rushed tokenized SPCX.

The DTCC's planned tokenized-securities pilot (50+ firms including BlackRock, Goldman, JPMorgan) points to far more ahead.

- Gold and commodities

Around $4.7B, dominated by tokenized gold, this category rode 2026's twin macro shocks:

- Gold ran to a record near $4,768 in May on global risk-off.

- Oil spiked to a four-year high above $120 as Strait of Hormuz disruptions tightened supply.

Traditional markets close; onchain commodity markets never do, so they increasingly serve as a pricing venue when others are shut. That is their core edge.

- Real estate.

It remains more promise than scale, but it is entering regulated markets: Dubai's Land Department opened tokenized property units for resale, and Hong Kong approved its first real-estate tokenization products.

The appeal is fractional ownership and tradable positions without waiting for a property sale.

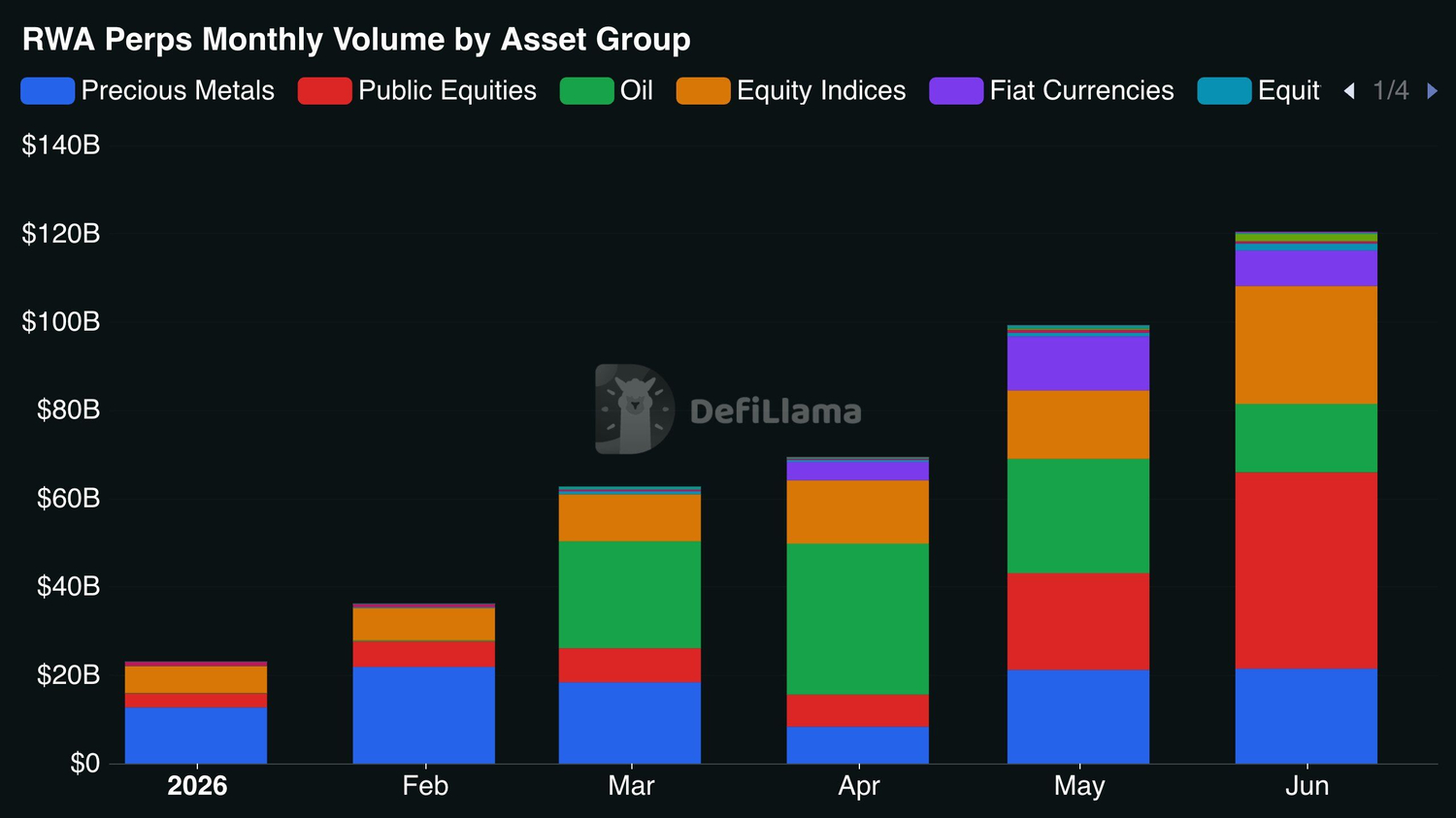

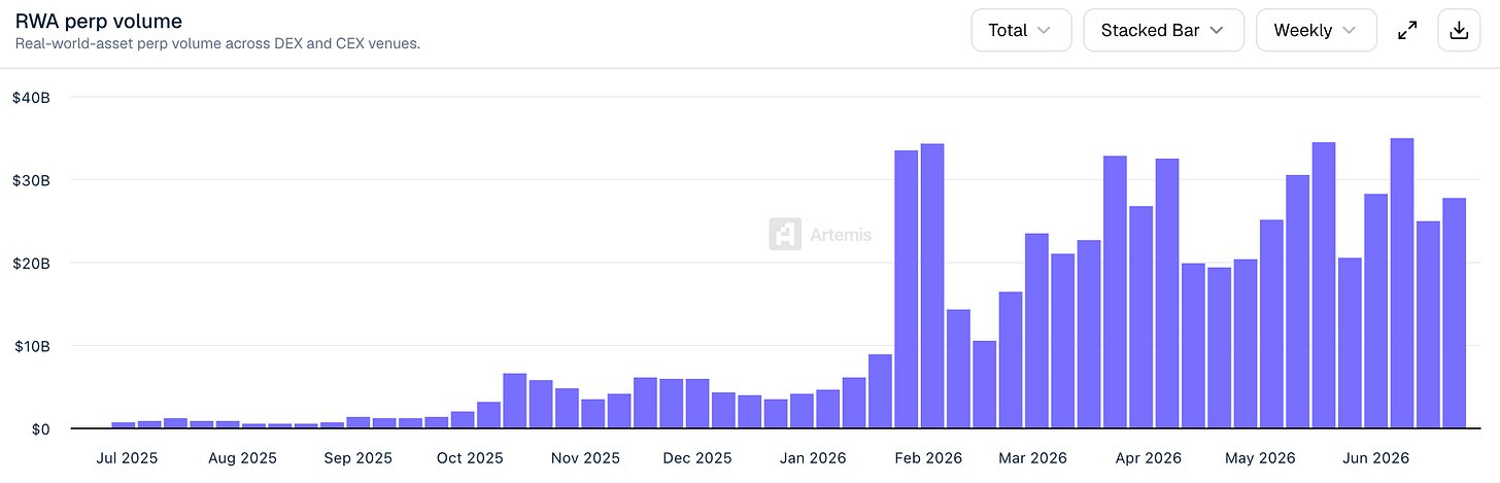

RWA Perps Hit a Record

That expansion is clearest in perps. Oil and equities in particular carried enormous momentum in 2026, and RWA perpetuals posted their biggest month ever in June, with volume first topping $100B (~$6B/day), roughly 5x since January.

The breadth is the tel. Public Equities and Equity Indices now rival Oil and Precious Metals, versus a January chart that was almost all metals.

The move looks structural, not speculative. Tradable markets exploded from 29 in January to 600+ by end-June.

The signal is that crypto rails are absorbing TradFi risk, becoming a settlement layer for leveraged macro exposure, and a rare bright spot while ETF flows and stablecoin supply contract.

Still early in the cycle.

Weekly volume went from under $1B to $30B in 12 months, yet RWA perps are only 6.2% of all perp volume and about 27% of on-chain perp volume, with just $3.6B in open interest.

As they expand into equities, commodities, FX, and beyond, the runway on-chain remains large.

Week Ahead

- Jul 13: U.S. Senate returns from recess

- Jul 14: U.S. June CPI

- Ongoing: Strait of Hormuz conflict

The Senate's July 13 return opens a roughly 25-day floor window before the August 7 recess, widely viewed as the last realistic gate for CLARITY Act passage in 2026. The bill is calendar-eligible but unscheduled, and still sits about seven to nine Democratic votes short of the 60 needed.

The Strait of Hormuz conflict is the live macro tail after the July 8 ceasefire collapse; watch oil as the read on whether June CPI gets interpreted as hawkish.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out above is for informational purposes only.