Summary

- Warsh's first FOMC broke with how the Fed operates. Forward guidance is gone, and he launched five task forces to remake Fed communications and its inflation gauge. Market-implied odds of at least one hike by year-end have risen to roughly two-thirds, and with the BoJ's hike to 1.00%, global liquidity is tightening.

- Institutions are still absent. Spot BTC ETFs have run net outflows for about a month and a half straight. The brief de-escalation rally drew no confirming inflows, marking it a news-driven blip, not a real rebound.

- The leverage structure is unhealthy and long-heavy. A 5% up day liquidated only ~$324M of shorts versus close to $1B of longs on a comparable down day. With no catalyst in sight, that excess optimism leaves the structure extremely fragile.

The Warsh Doctrine: Less Guidance, Higher for Longer

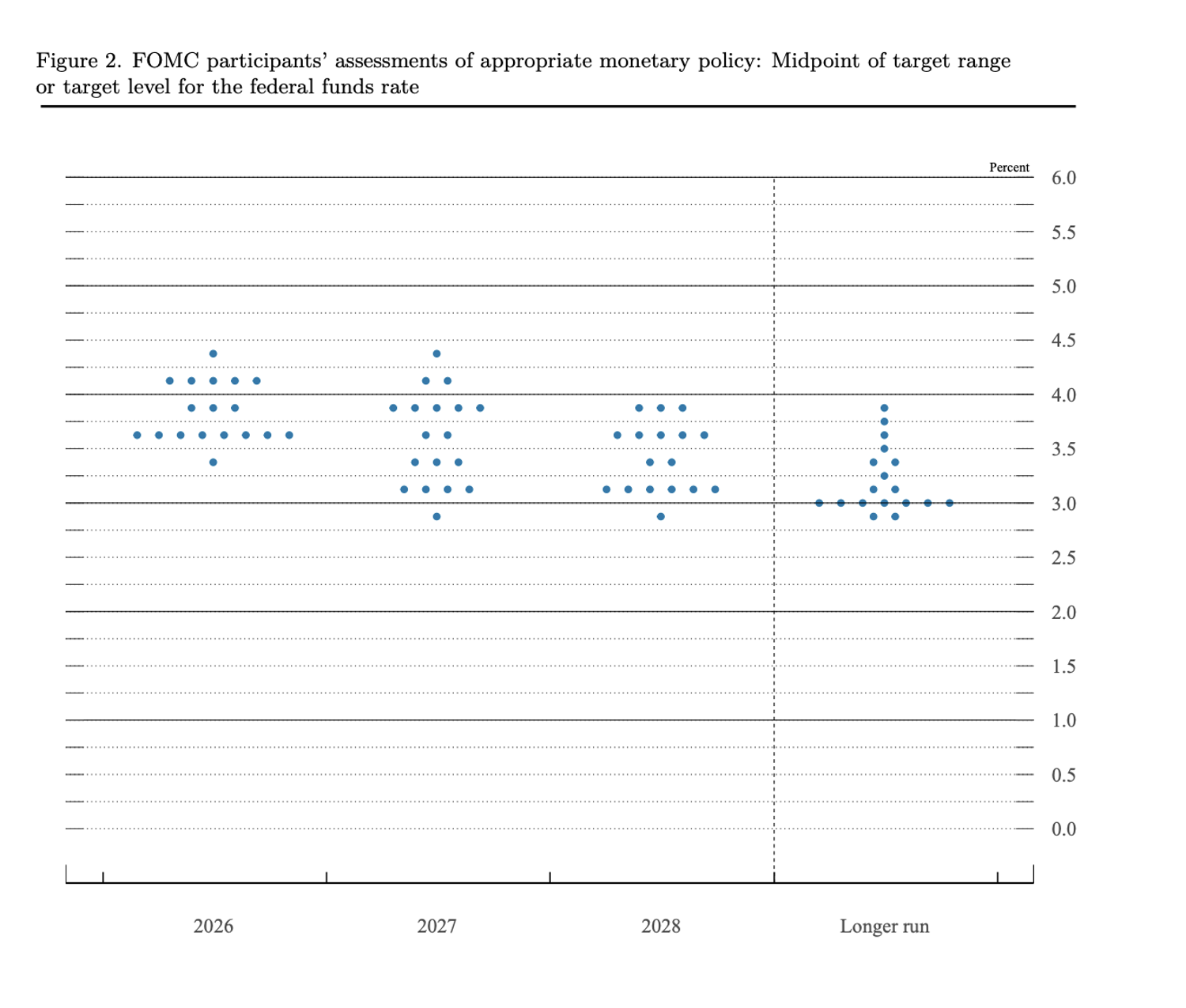

The June FOMC rate decision was fully expected; everything else was not. The Committee held the target range at 3.50 to 3.75 percent by unanimous vote, but the accompanying Summary of Economic Projections (SEP) marked a directional reversal:

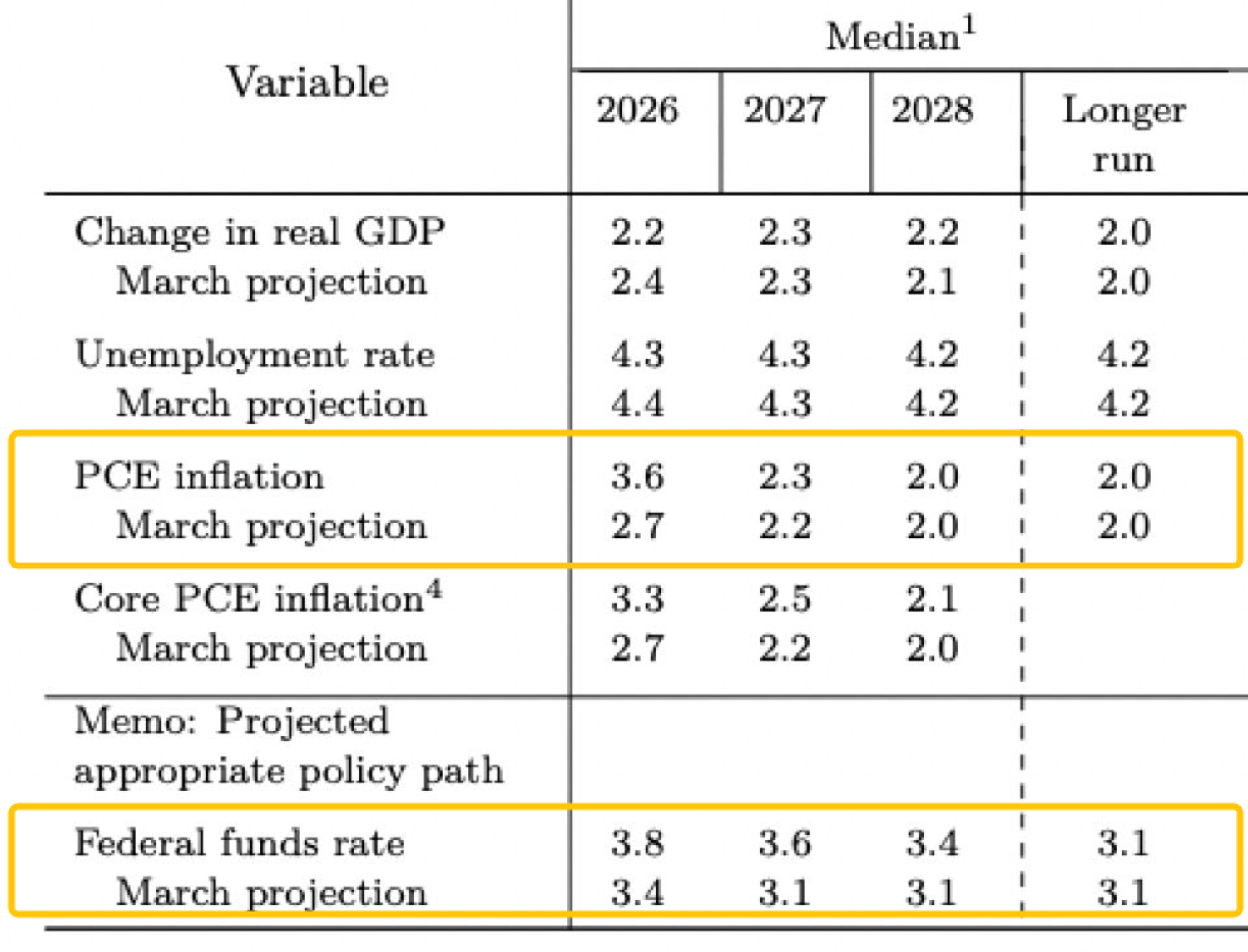

- Rate path: the median end-2026 dot rose to 3.8 percent from 3.4 percent in March, with nine of eighteen participants now projecting at least one hike this year.

- Inflation: the 2026 headline PCE forecast was lifted to 3.6 percent (from 2.7 percent) and core to 3.3 percent.

- Growth and jobs: 2026 GDP growth was trimmed to 2.2 percent (from 2.4 percent), while unemployment was nudged down to 4.3 percent.

The trigger was an energy-led inflation shock, with May CPI at 4.2 percent year-over-year, the hottest in three years, layered on a still-firm labor market.

A tension in the projections. The Fed sees 2027 PCE inflation falling back to 2.3 percent, yet keeps the 2027 funds rate elevated at 3.6 percent (revised up from 3.1 percent in March).

It projects inflation nearly back to target next year but not the rate relief that would normally accompany it. That implies a Fed intending to keep policy restrictive well past the point where its own inflation forecast would justify easing, reinforcing the higher for longer signal independent of the dot count.

Key change: the mechanism

- Forward guidance was removed.

Warsh's rationale, laid out before he took office, is that he does not want markets reading off where individual FOMC members expect rates to go next; keeping that view private, in his thinking, leaves the Fed more flexible to change course without being held to a path it has signaled.

- The inflation gauge may shift to trimmed mean.

Warsh has argued that headline PCE and CPI are dated and less representative of true inflation, and signaled a preference for a trimmed-mean measure, which strips out the largest upside and downside outliers.

A trimmed-mean gauge would tend to print lower than headline PCE; if the Fed eventually anchors policy to it, that could open an earlier and more credible path to easing than the current dots imply.

- Five task forces will review Fed operations.

Warsh announced five working groups covering communications, the balance sheet, data sources, productivity and jobs, and the inflation framework. Personnel are reportedly chosen but not yet confirmed, so this is a signpost to track rather than a change in effect today.

- AI is expected to keep inflation in check.

Warsh pointed to AI-driven productivity as a force likely to contain inflation over the medium term, a structurally disinflationary view that, if it holds, leans dovish over the horizon.

A hawkish repricing, reinforced globally

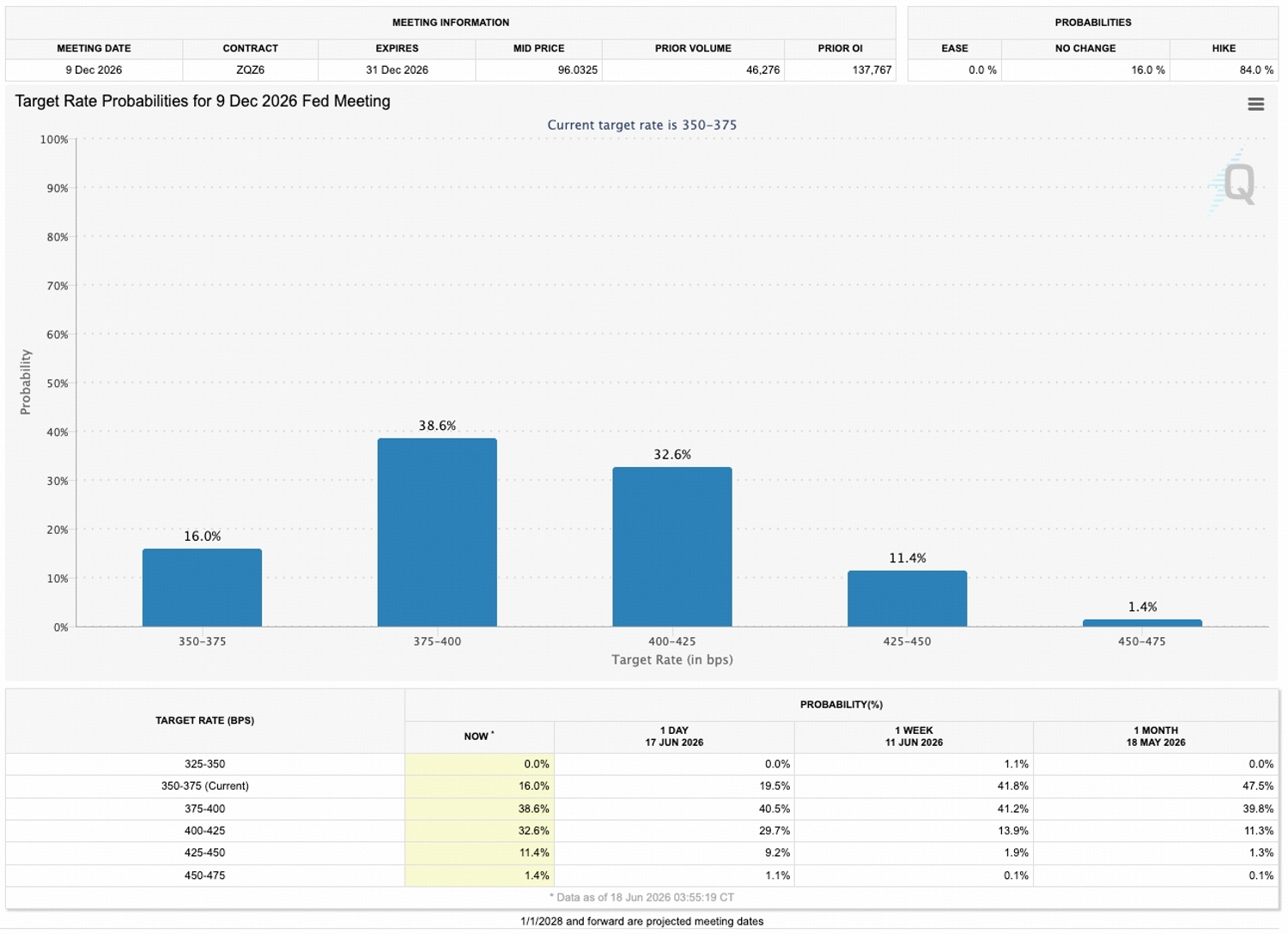

The easing cycle the market priced at the start of 2026 is now substantially impaired. Following the meeting, market-implied odds shifted to roughly a two-thirds probability of at least one hike by year-end, a near-complete reversal from the cut priced only months ago.

The single most important swing factor is energy, since the inflation upgrade is largely an oil-price story.

A credible de-escalation that pulls energy lower is the fastest route to a softer PCE print and an eventual dovish revision; combined with a possible trimmed-mean reframing and AI-driven disinflation, that is the path on which the current hawkish dots prove to be a peak rather than a trajectory.

Source: FedWatch

At the same time, under pressure from a weak yen and energy-driven inflation, the Bank of Japan raised its policy rate by 25 basis points to 1.00 percent on June 16, its highest level since 1995.

A BoJ that keeps tightening compresses the yen-funded carry that has quietly financed global risk-taking, removing a source of marginal liquidity.

Set against the Fed's upgraded rate path, it reinforces the same direction. Until softer data shows up, macro is a headwind, not a tailwind.

Flow Data: Institutions Are Still Absent

US spot BTC ETFs now hold roughly 6% to 7% of circulating supply, which makes them the marginal buyer on the way up and the marginal seller on the way down.

As of June 17, the complex has run a near-continuous stretch of net outflows lasting about a month and a half. The chart shows the shift plainly: the green inflow bars that dominated April and early May give way to an almost unbroken run of red from mid-May onward.

Bitcoin saw a brief macro-driven move on the back of de-escalation headlines and the prospect of the Strait of Hormuz reopening, but the ETF flows never confirmed it. There was no meaningful inflow alongside the price reaction.

It marks the move as a short-lived response to the news flow, not the start of a genuine rebound. A real recovery would need the largest structural buyer to step back in, and so far it has not.

With the Fed's upgraded rate path and the Bank of Japan's hike both pulling in the direction of tighter global liquidity, the conditions that would draw institutional capital back into the ETF complex are not yet in place. Until the flow prints turn green, the signal for a sustained rebound is simply not there.

Derivatives: An Unhealthy Long-Heavy Structure

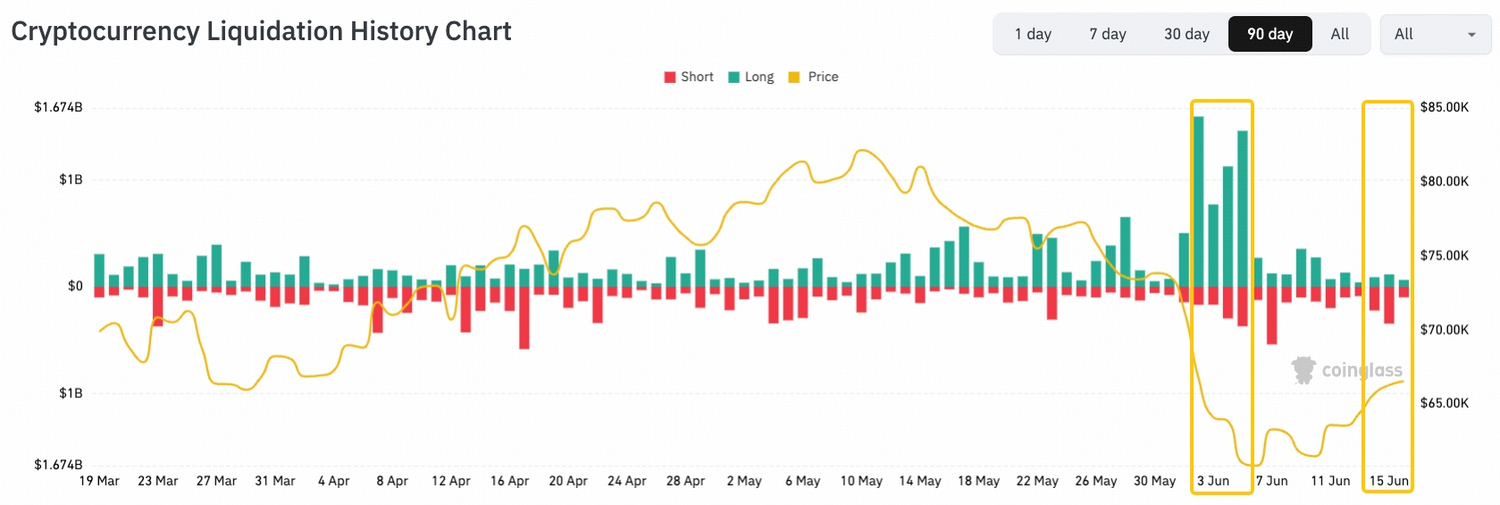

This week's liquidation data shows a clear leverage asymmetry.

When BTC rose around 5% in a single day, short liquidations reached only about 324 million dollars; by contrast, when BTC fell around 5% in a day two weeks earlier, long liquidations ran close to 1 billion. Same size of move, vastly different scale of forced closures.

The read is that leveraged longs still far outweigh leveraged shorts, and the market remains overly optimistic even as the macro backdrop deteriorates.

This is not healthy. Institutional capital has not stepped back in, there is no clear positive catalyst on the table, and none is obviously on the horizon. Against a backdrop of tightening global liquidity and oil-driven inflation pressure that cannot be absorbed quickly, that excess optimism leaves the current structure extremely fragile.

Week Ahead

- Jun 23: U.S. Conference Board Consumer Confidence (Jun)

- Jun 25: U.S. May PCE

- Jun 25: U.S. Q1 GDP (third estimate)

The week's core event is the June 25 PCE release. Having just lifted its 2026 PCE forecast to 3.6% almost entirely on energy, the Fed faces its first test of whether last week's hawkish pivot is justified or already stale.

A soft core print would be the fastest route to an eventual dovish revision, while a hot one would confirm the higher for longer path and keep the dollar and real yields elevated, sustaining the headwind on BTC.

With forward guidance now removed under Warsh, every print carries a wider volatility premium than usual.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out above is for informational purposes only.