The Rally Was Genuine; Leverage Did the Damage

Gold and silver delivered an exceptional January by historical standards: within a fortnight, gold rose by more than 25% and silver by more than 60%. Even during the 1970s, when modern spot precious-metals markets were taking shape, moves of this magnitude were rare. Leverage and trend-following capital moved in rapidly. In the final week of January, registered (warranted, deliverable) inventory accounted for only 14.2% of total open interest in COMEX silver futures; even when focusing only on the delivery months, registered inventory was just 21.6% of delivery-month open interest.

This set-up implied that prices were being driven primarily by expectations and leverage, rather than by a gradual change in underlying physical demand. More importantly, in such phases, open interest often expands far faster than deliverable physical inventory can adjust. Once outstanding contracts grow well beyond exchange deliverable stocks, the market’s central tension shifts from “getting the direction right” to structural constraint: delivery exposure becomes a first-order risk factor, not merely a contractual detail.

Source: DataTrack

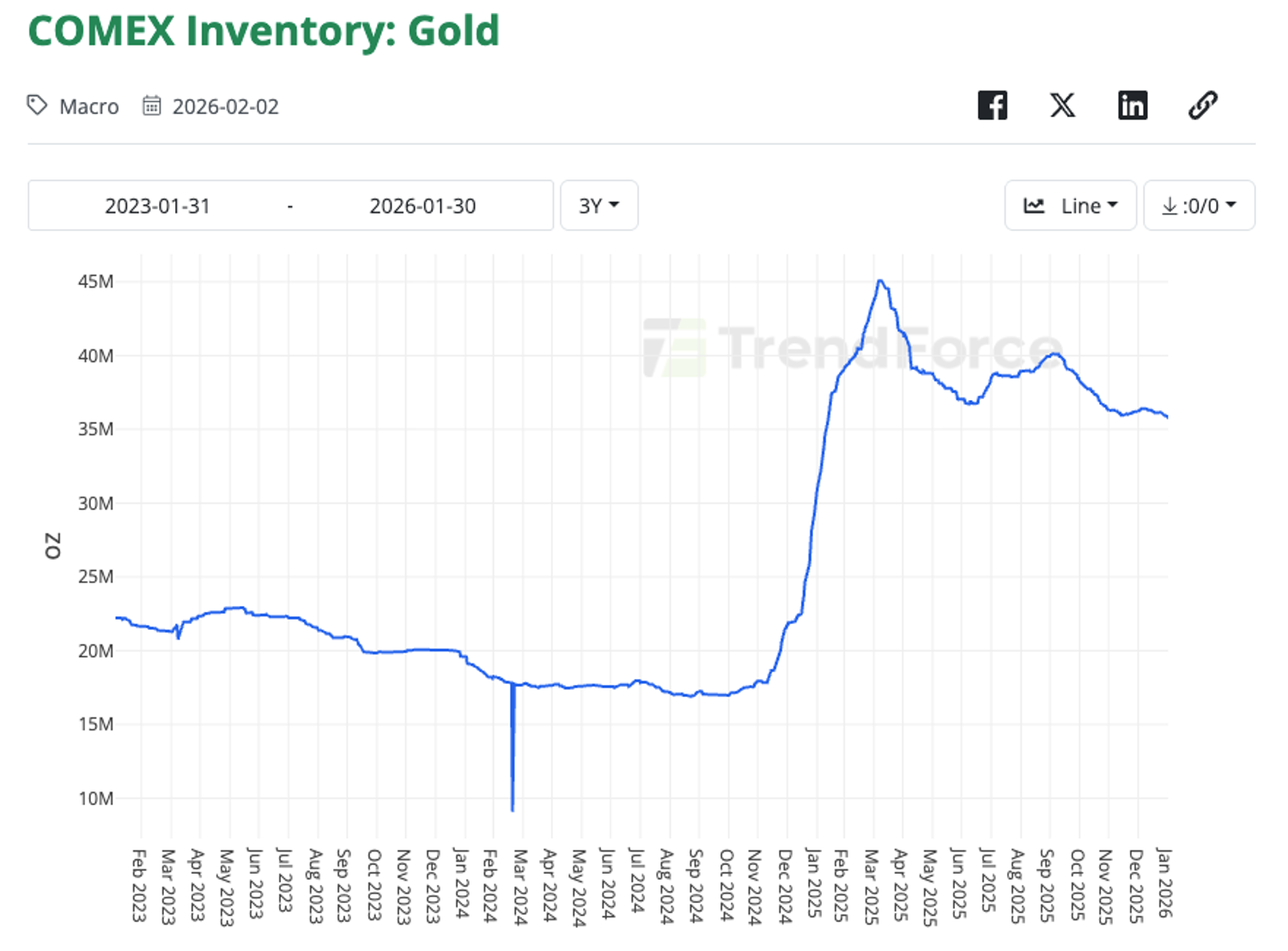

In normal conditions, liquidity and routine rolling activity can make the delivery framework feel distant, leading some participants to treat precious-metals futures as a highly liquid, leveraged proxy for spot. That assumption, however, is conditional: the ratio of deliverable inventory to front-end open interest must remain within a relatively safe band (typically 40%–50%). For gold, that ratio was still within a safer range (59.73%). For silver, it had already moved well beyond the red line. Gold inventories have also been comparatively stable, which tends to provide better shock absorption when speculative activity surges.

Source: DataTrack

Because precious-metals futures ultimately sit on a physical delivery regime, the framework becomes materially more binding as the delivery month approaches, shaping position management in a more rigid way. As COMEX silver registered inventory continued to decline, the market confronted a dangerously unbalanced relationship between open interest and deliverable metal. Once a contract enters its delivery month, most speculators lack the logistics, warehouse access and operational readiness to take delivery of multiple tonnes of silver; in practice, many are pushed towards forced closing of their positions.

Ahead of the delivery window, speculative positions have only two practical paths: take profit or roll. Rolling introduces frictions — carry costs, margin usage and liquidity discounts. When volatility rises and margin pressure increases, taking profit is often the more risk-budget-efficient choice. As the market transitioned from one-way upside to a high-volatility regime, many participants were pushed by similar constraints in the same direction over a short period, laying the groundwork for systemic selling.

Delivery Mechanics Trump Narratives

To reduce the risk of a disorderly wave of forced liquidations into delivery, major exchanges implemented preventative measures. CME and SHFE raised margin requirements repeatedly and introduced more dynamic margin models. The essence of these actions is to raise the cost of carrying positions, deliberately tightening liquidity and forcing speculators to choose between taking profit and rolling.

These interventions are often interpreted as an attempt to “cap” prices. From a risk-governance perspective, a more accurate reading is that they aim to prevent concentrated pre-delivery liquidations. Such episodes can create a liquidity vacuum: thinner order books, more frequent gapping, wider spreads, impaired price discovery, and, in the worst case, tail risk to the clearing system.

Accordingly, when excessive leverage meets a sharp rise in realised volatility, exchanges tend to prefer incremental measures — higher margins, dynamic risk-parameter adjustments, and tighter limits on excessively concentrated positions — to raise holding costs and encourage speculative liquidity to retreat in a relatively orderly manner before delivery. This process is not a directional call; it is intended to reduce systemic tail risk, allowing crowded positioning to cool gradually rather than clearing abruptly at a single point in time.

What typically amplifies the drawdown is not one participant taking profit, but the feedback loop created when homogeneous behaviour occurs simultaneously. The transmission chain often unfolds in three stages:

- First, concentrated long unwinds weaken prices.

- As net speculative length contracts quickly, market-makers and hedging flows from options and structured products adjust exposures at the same time. To remain risk-neutral (for example, Delta-neutral), they hedge volatility and directional risk by selling spot or the near-month contract.

- Leveraged accounts then face margin calls and forced liquidation. The sell-off triggers further forced selling, which in turn depresses prices — a recursive “down-move → liquidation → further down-move” loop.

The consecutive large down candles, the sudden loss of market depth and the deterioration in trade structure were, in essence, a rapid reset of positioning — precisely what played out last Friday.

Crypto: Cross-Asset Deleveraging Spillover

Crypto came under pressure alongside this episode, largely due to the overlap of two factors: heightened geopolitical risk (including a higher probability of renewed Gulf tensions) and increased uncertainty around the policy stance of the Fed Chair-designate. Under such macro uncertainty, institutional risk frameworks typically become more sensitive and less tolerant. In particular, when realised volatility in gold — the “ultimate safe haven” — rises sharply, and silver’s realised volatility prints at record levels, many portfolio risk models reduce allocations across all risk assets, not only the first asset to break. High-beta exposures are therefore cut in parallel, with emerging-market equities, credit risk and crypto often taking the first hit.

In addition to commodities, emerging markets such as South Korea have also experienced a sell-off. Source: Tradingview

Crypto’s additional fragility is structural leverage. Perpetual swaps, funding rates and collateralised lending can build vulnerabilities during rallies, then magnify forced selling when conditions turn. Because crypto trades 24/7, can be liquidated quickly, and often carries a higher risk weight in institutional frameworks, it frequently becomes the “first unit to sell” when risk budgets tighten — and thus absorbs a disproportionate share of the pressure during cross-asset deleveraging.

ETH suffered a heavy loss in the latest sell-off. Source: Tradingview

Outlook: Metals Reset vs Crypto Repricing

Going forward, the divergence between gold/silver and crypto is worth emphasising. For precious metals, this drawdown looks more like a reset of leverage and positioning than a rejection of the long-term thesis. Medium- to long-term drivers — the path of real rates, reserve-asset allocation, and the geopolitical tail-risk premium — are unlikely to reverse in a way that matches the price slope observed over a fortnight. In other words, the decline primarily addressed “who owned the move and with how much leverage”, not “why hold an allocation”.

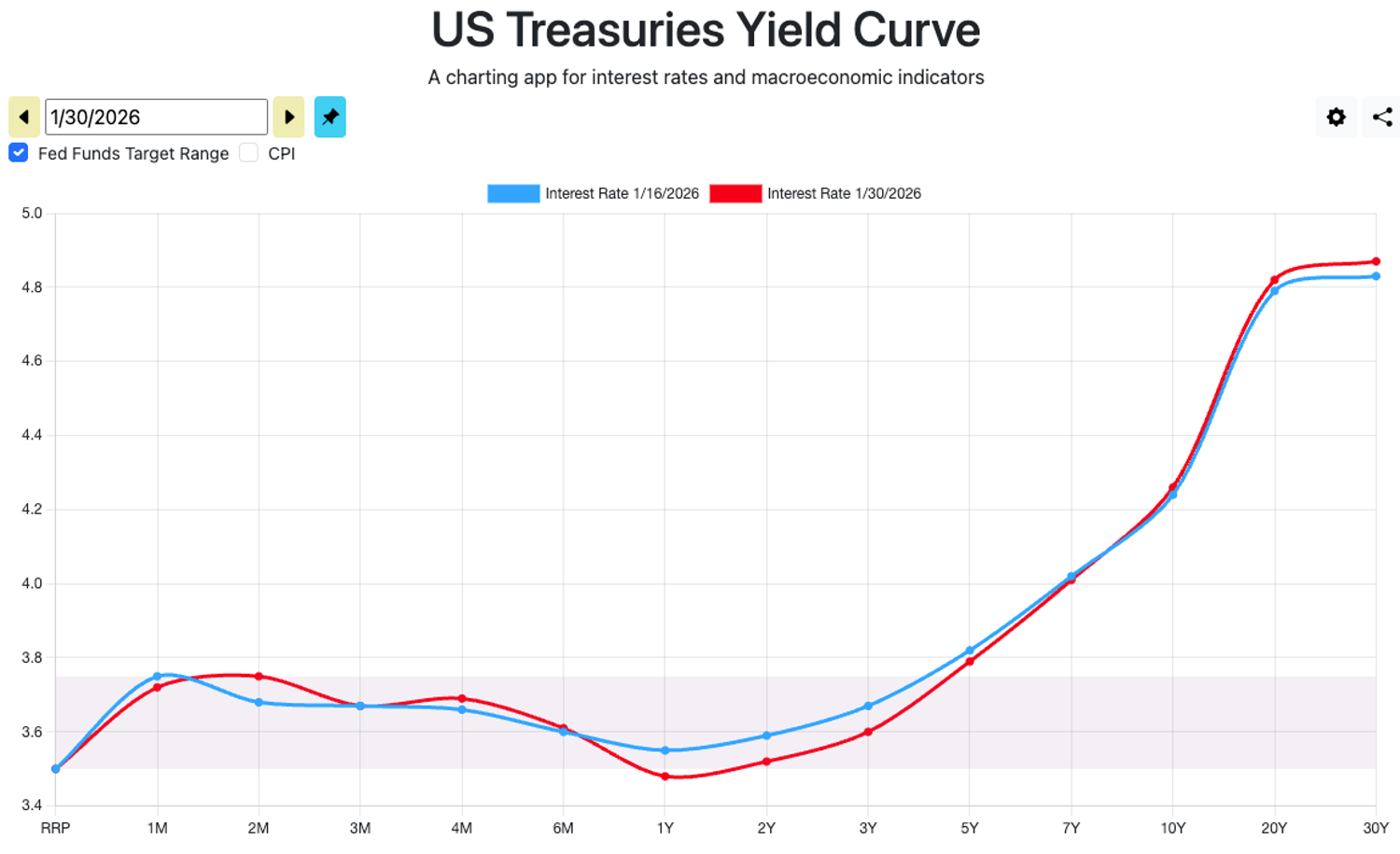

Once forced liquidations and margin constraints have cleared excess positioning, and provided there is no meaningful macro or funding inflection in the opposite direction, precious metals can still re-enter a longer-cycle uptrend. Notably, outside commodities, neither bonds nor rates moved materially, and equities were not significantly affected — reinforcing the view that this “epic commodity deleveraging” was, at most, a brief interruption.

Source: ustreasuryyieldcurve.com

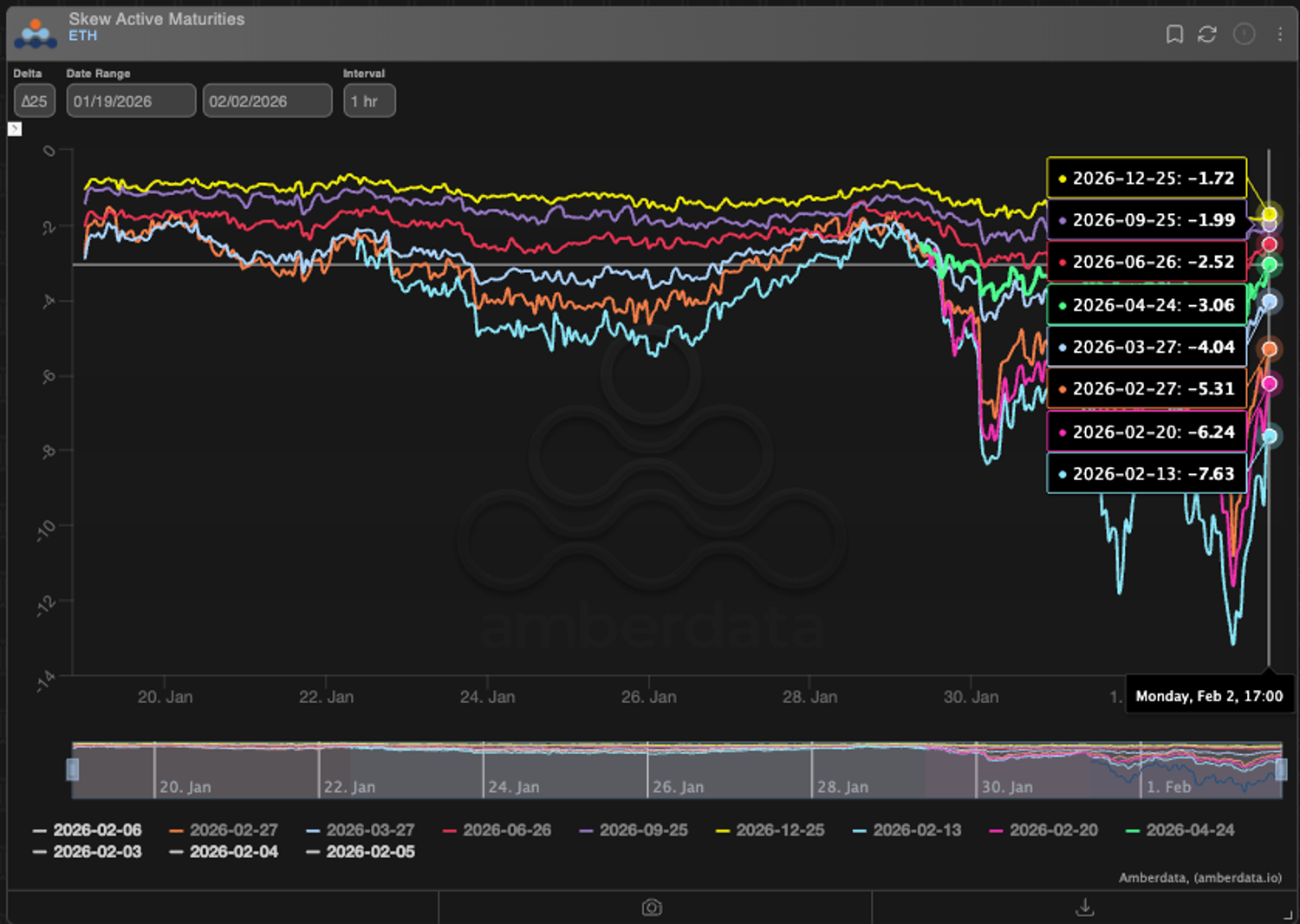

By contrast, crypto’s recovery is more dependent on a renewed expansion in global liquidity and risk appetite. Forward expectations for BTC and ETH had already weakened earlier, and — aside from BTC — most crypto assets sit at the far end of the risk-asset transmission chain. In an environment where global liquidity expansion is stalling, marginal capital is less likely to reach them. The baseline implication is consolidation or a gradual drift lower, rather than a rapid V-shaped rebound.

Source: Amberdata Derivatives

Source: Amberdata Derivatives

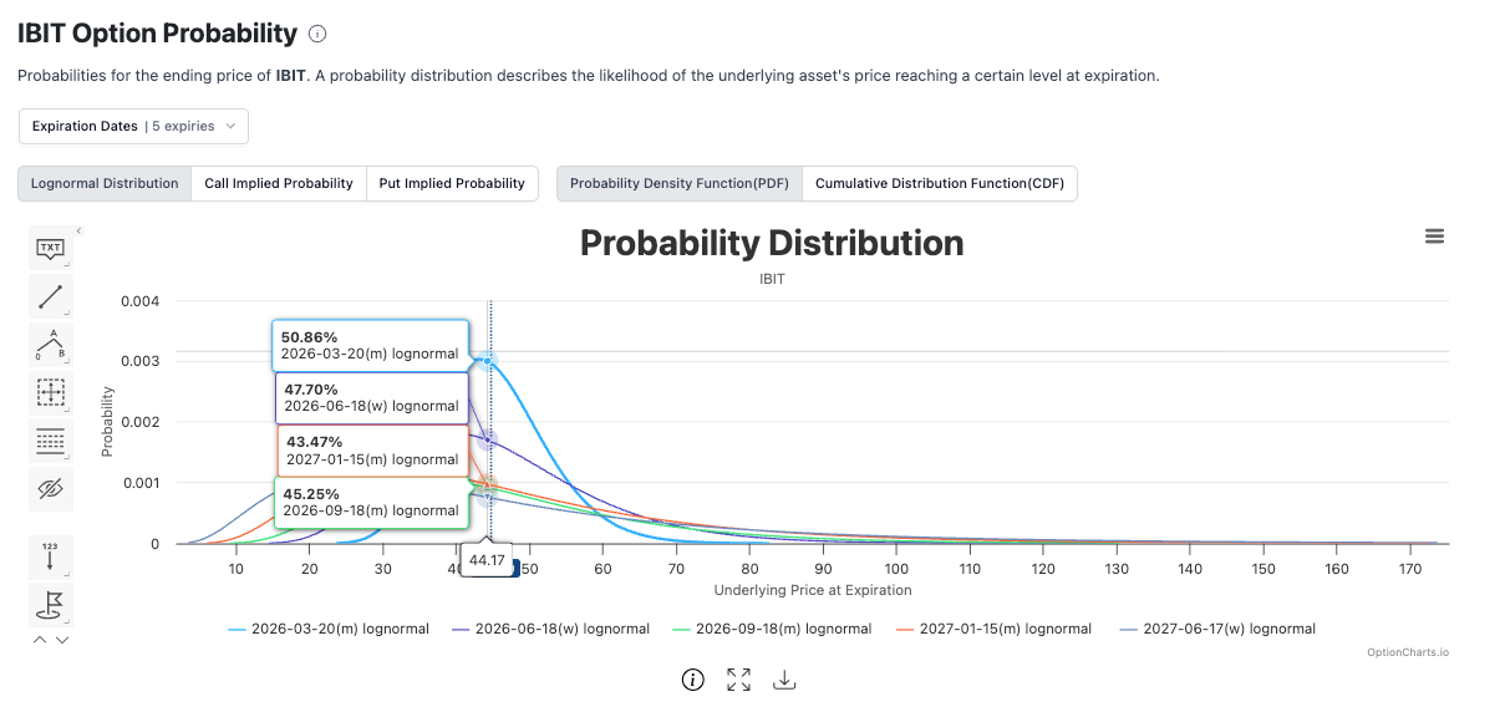

That said, this does not automatically imply a prolonged deep drawdown. With BTC and ETH now closer to the median of their probability density distributions, a more common follow-on pattern is low-level consolidation: volatility falls from elevated levels, funding and leverage reset lower, and the market rebalances over time — waiting for the next macro and liquidity signal to provide direction.

Source: optioncharts.io

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.