"No Data"

October isn't typically a significant macroeconomic month, as key central bank meetings usually occur at the end of the quarter. For example, the Federal Reserve generally releases summary economic projections at its FOMC meetings in March, June, September, and December, while other months are merely "routine meetings."

However, for traders, the level of uncertainty leading up to this FOMC meeting may exceed that of the September meeting. Investors and interest rate policymakers are facing an unprecedented situation: a lack of sufficient data sets to support their next course of action.

It all stems from the government shutdown in early October 2025. This shutdown, triggered by a congressional budget impasse, paralysed the BLS (U.S. Bureau of Labour Statistics) reporting process, including the September non-farm payroll data and subsequent CPI/PPI indicators, which were initially scheduled for release on October 3rd. The shutdown has already lasted a month, and BLS employees are effectively unemployed, leaving them unable to collect, clean, analyse, and publish data.

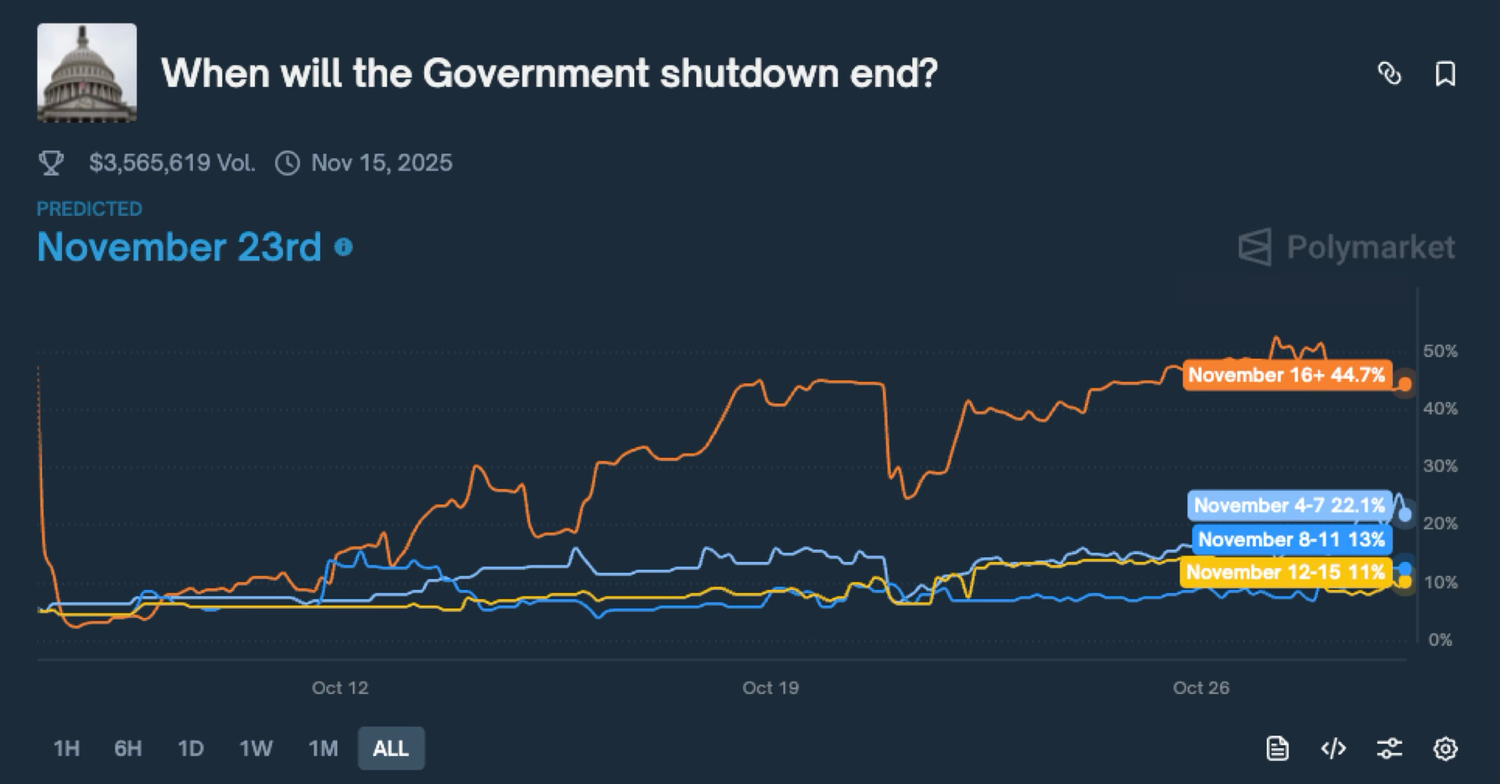

Admittedly, this may just be the beginning of a worse situation. No one knows when the government will reopen; according to Polymarket, investors expect it to close before November 23rd, while more aggressive forecasts have pushed it back to January—of course, either scenario significantly exceeds market expectations. Without wages, there can be no work, and the release of October and November CPI and employment data has been delayed indefinitely, or even cancelled entirely.

Source: Polymarket

The Federal Reserve is not without a plan to address this situation, which was previously considered "extremely risky." As a cross-verification and backup, the Fed had previously been working with ADP (Automatic Data Processing, Inc.) to obtain additional employment data. But now, that backup is completely gone: ADP unilaterally terminated its real-time data access to the Fed in late August. Despite the Fed's repeated formal requests to restore access, the only response received was "HTTP 403 (Access Denied)." Powell is now in a "black box": only fragmented information can inform his next economic decisions, which could impact the world.

While data delays aren't disastrous (at least for now), they magnify the erosion of political uncertainty on monetary policy, extending further into the economy. Institutional investors find prolonged data absence unbearable, while business operators hesitate to increase hiring or expand production amidst high uncertainty and unpredictability.

The Fed is also facing a difficult situation: September's inflation data, while lower than expected, remained at 3%—clearly above its 2% target. If data gaps continue, blindly cutting interest rates will only lead to reflation or even stagflation. However, if interest rates are held steady, labour market weakness could potentially escalate into a recession. Either direction requires data support, but it's likely that there will no longer be authoritative official data to reveal what happened in November and December.

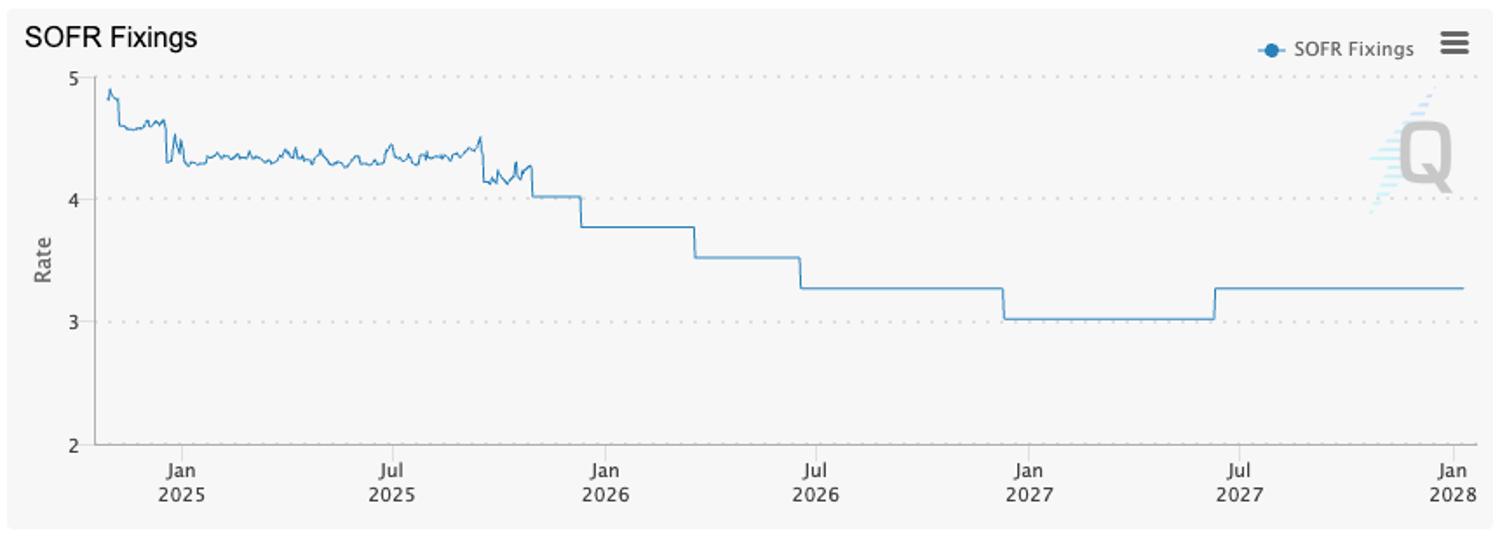

At present, perhaps one of the few reliable anchors is the interbank market. SOFR futures are among the core tools banks and financial institutions use to hedge interest rate risk, and a large mismatch could lead to significant losses for banks and even a new banking and liquidity crisis. Therefore, the Fed typically tries to keep its interest rate decisions consistent with expectations to minimise market volatility.

Source: CME Group

Clearly, rate cuts remain the dominant theme. SOFR futures traders expect the Fed to cut rates five times over the next 14 months, with the year-long 3% endpoint rate forecast unchanged. This year, despite a lack of data, the Fed is expected to cut rates again in December. However, third-party data suggests the Fed may need to slow down its pace again.

Sticky Inflation

While not as authoritative as the BLS, Truflation's inflation data is still worth paying attention to. Starting in April, the inflation index began a steady rise, consistent with our predictions in previous months: the tariff war would trigger a "supply chain pulse," increasing costs across warehousing, transportation, and distribution, ultimately passing on to consumers. Although the government has asked supermarket giants like Walmart to bear the additional costs, it's clear they cannot.

Source: Truflation

Even based on official CPI data for September 2025, the rising risk of inflation is evident. Overall CPI rose 0.3% month-on-month and jumped to 3.0% year-on-year, the highest level since January of this year. This is 0.3 percentage points higher than the 2.7% year-on-year increase in August, marking the fifth consecutive month of acceleration. Core CPI (excluding food and energy) is also not optimistic, rising slightly by 0.2% month-on-month but remaining stable at 3.0% year-on-year, indicating that price pressures after volatility adjustment remain strong.

More detailed data also indicates a rebound in inflation. Alternative indicators, such as PriceStats, based on online retail prices, show that September inflation reached 2.6% year-on-year, a two-year high, primarily driven by furniture and household equipment prices. The CPI for durable goods and personal consumption products surged 0.6% month-on-month, the highest since June, influenced by rising costs of personal care products and communication equipment. Housing rents rose 3.4% year-on-year, used car prices soared 5.1%, and tobacco products saw an even higher increase of 6.9%. These data clearly indicate that inflation is rebounding from its post-pandemic lows and entering a new normal of "higher equilibrium," also known as "sticky inflation."

Furthermore, due to the suspension of inflation data releases, the public typically "considers the worst-case scenario" and prepares accordingly when data is scarce. This is understandable (risk aversion is human nature), but objectively, it pushes up inflation expectations. When every link in the economic chain is preparing for another rise in inflation, inflation, to some extent, becomes a "self-fulfilling prophecy".

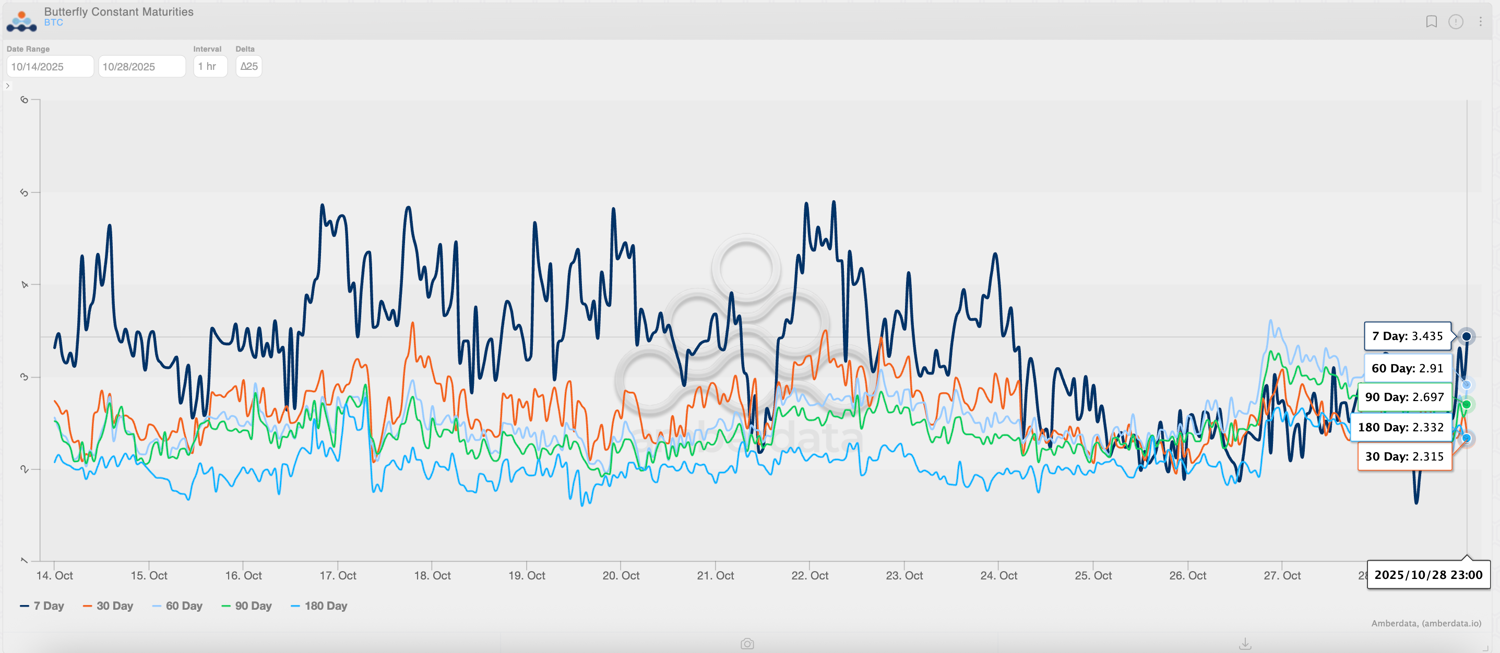

Source: Amberdata Derivatives

In the 1970s, the United States experienced the "Volcker moment" to curb rising inflation and persistent inflation expectations. Now, amid a rebound in inflation, derivatives traders have begun betting on a potential policy shift by the Federal Reserve. In the crypto market, BTC's tail risk pricing structure remains backwardation, while even ETH's tail risk pricing has reverted to a contango pattern, which is rare in trading records. Given BTC's high sensitivity to macroeconomic factors, it seems smart traders are already preparing for possible Fed actions in the event of persistent sticky inflation, something we need to monitor closely. Let's see what Powell is thinking at this week's FOMC meeting.

Economic Calendar of This Week

Monday 12:30

- US Durable Goods Orders MoM

Wednesday 18:00

- US Fed Interest Rate Decision

Wednesday 18:30

- US Fed Press Conference

Thursday 10:00

- EU GDP Growth Rate QoQ Flash

- EU GDP Growth Rate YoY Flash

Thursday 12:30

- US GDP Growth Rate QoQ Adv

Thursday 13:15

- EU Deposit Facility Rate

- EU ECB Interest Rate Decision

Thursday 13:45

- EU ECB Press Conference

Friday 10:00

- EU Inflation Rate YoY Flash

Friday 12:30

- US Personal Income MoM

- US Personal Spending MoM

- US Core PCE Price Index MoM

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.