Calm Bitcoin, Hot Gold

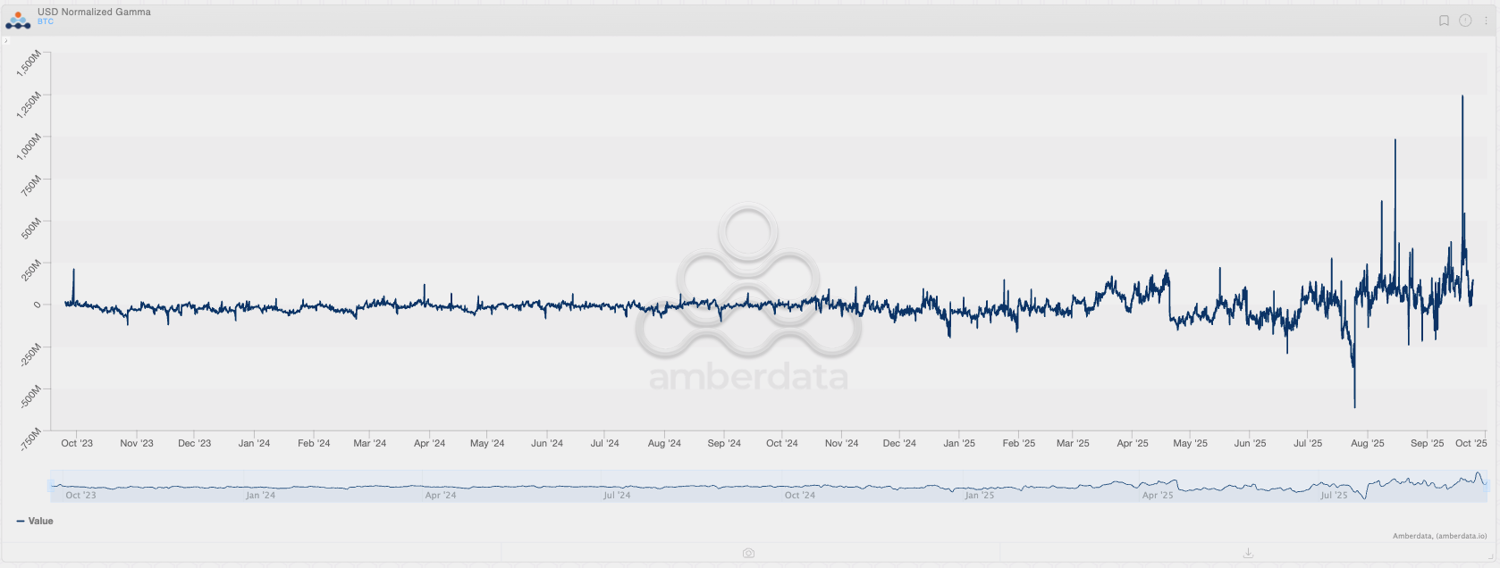

Before quarterly settlements, the crypto market is often characterised by calm. With millions of options contracts expiring, the internal market forces suppressing price movements are reaching their highest levels in months, if not ever. For example, expiring IBIT, CME, and Deribit options are generating astronomical cash gamma: in the most extreme case, even just Deribit options are included, a 1% price movement up or down would result in market makers buying or selling $1.25 billion worth of Bitcoin—undoubtedly, this is a "dominant force".

Record-breaking cash gamma is becoming a dominant factor in BTC trends. Source: Amberdata Derivatives

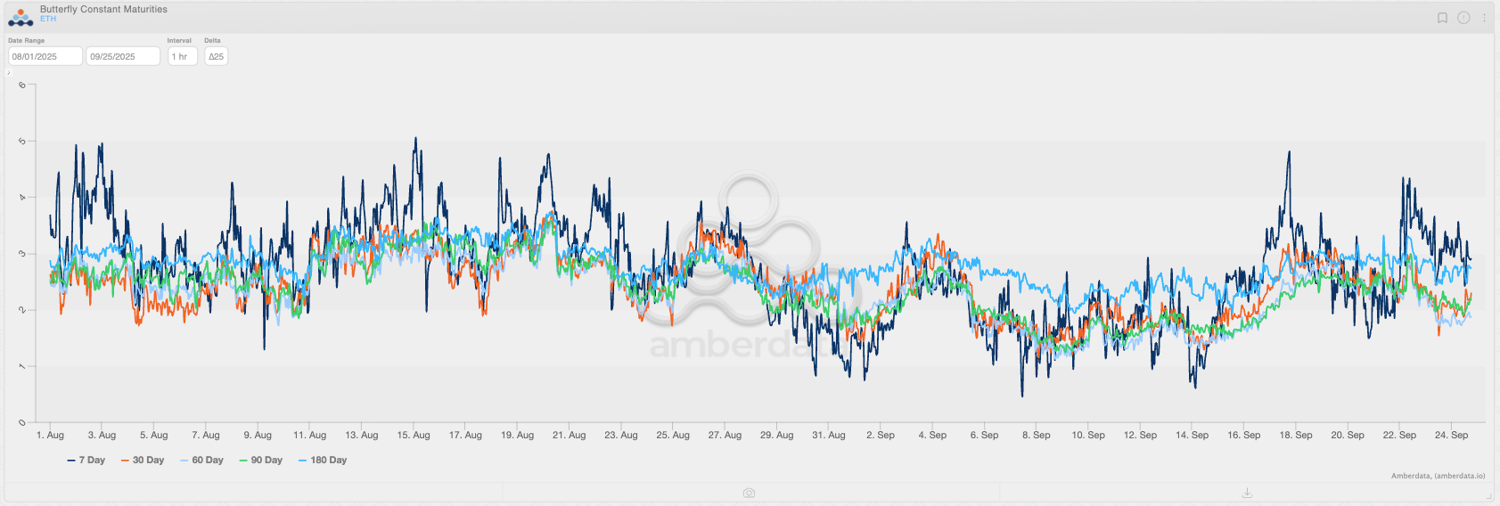

The same is true for ETH. Record-breaking cash gamma is causing its price to enter a "strange calm" state after months of volatility. Only tail risk pricing remains sensitive: despite ETH's price fluctuations of less than 1% daily after Monday's drop, tail risk pricing remains at a high level not seen since late August. This "calm" will persist until Friday, when the market may regain its "heartbeat" after the settlement.

The Butterfly Index is one of the few risk indicators remaining sensitive in the crypto market for now. Source: Amberdata Derivatives

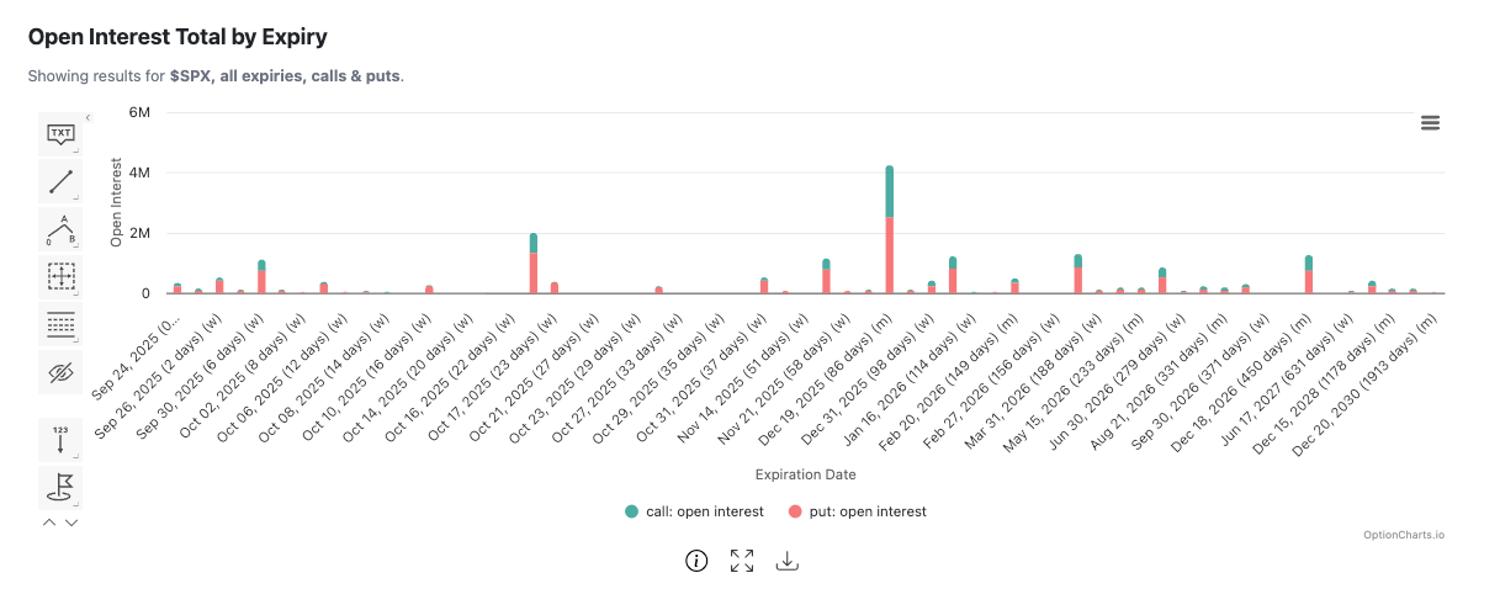

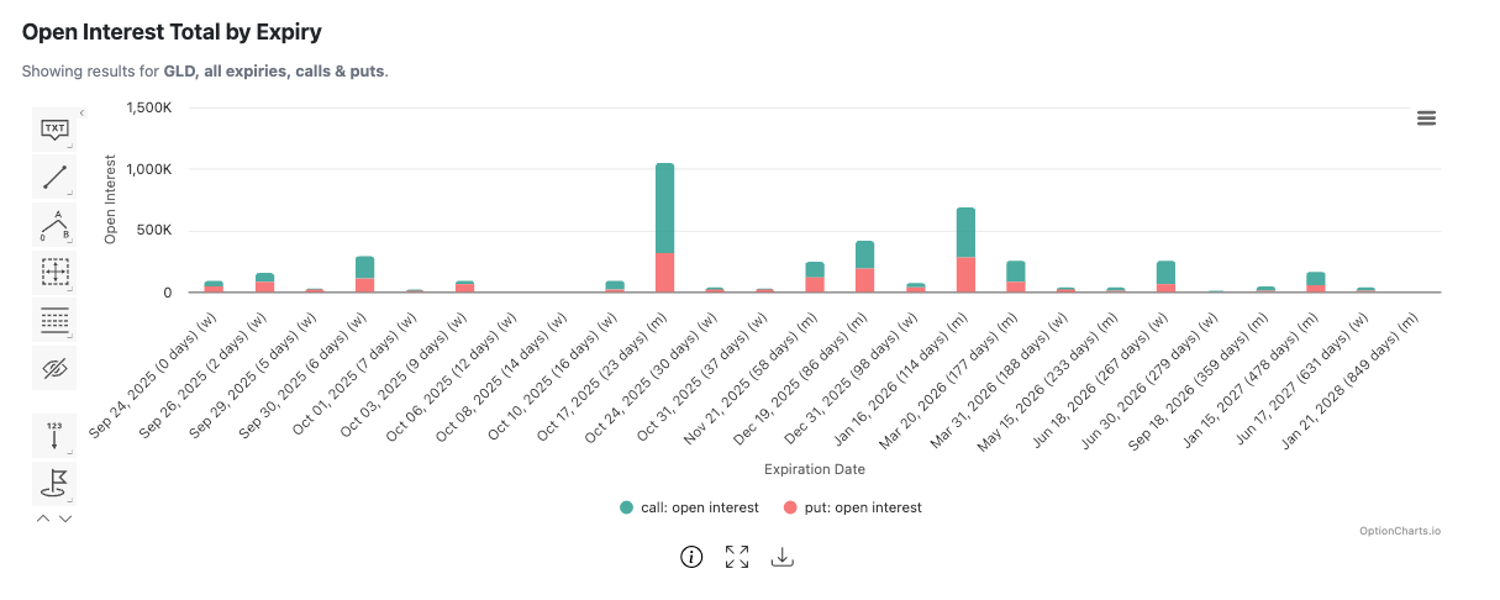

SPX and GLD are still far from the settlement season. Source: optioncharts.io

However, while the crypto market remained calm, the buoyant US stock and precious metals markets remained largely unaffected by derivatives settlements. SPX and QQQ settlements were concentrated around Christmas, while GLD settlements were in October and January. Investors' bullish outlook remained largely unaffected by hedging. As a result, both the US stocks and precious metals markets significantly outperformed the crypto market this month, with the precious metals market's performance in September being "unprecedented":

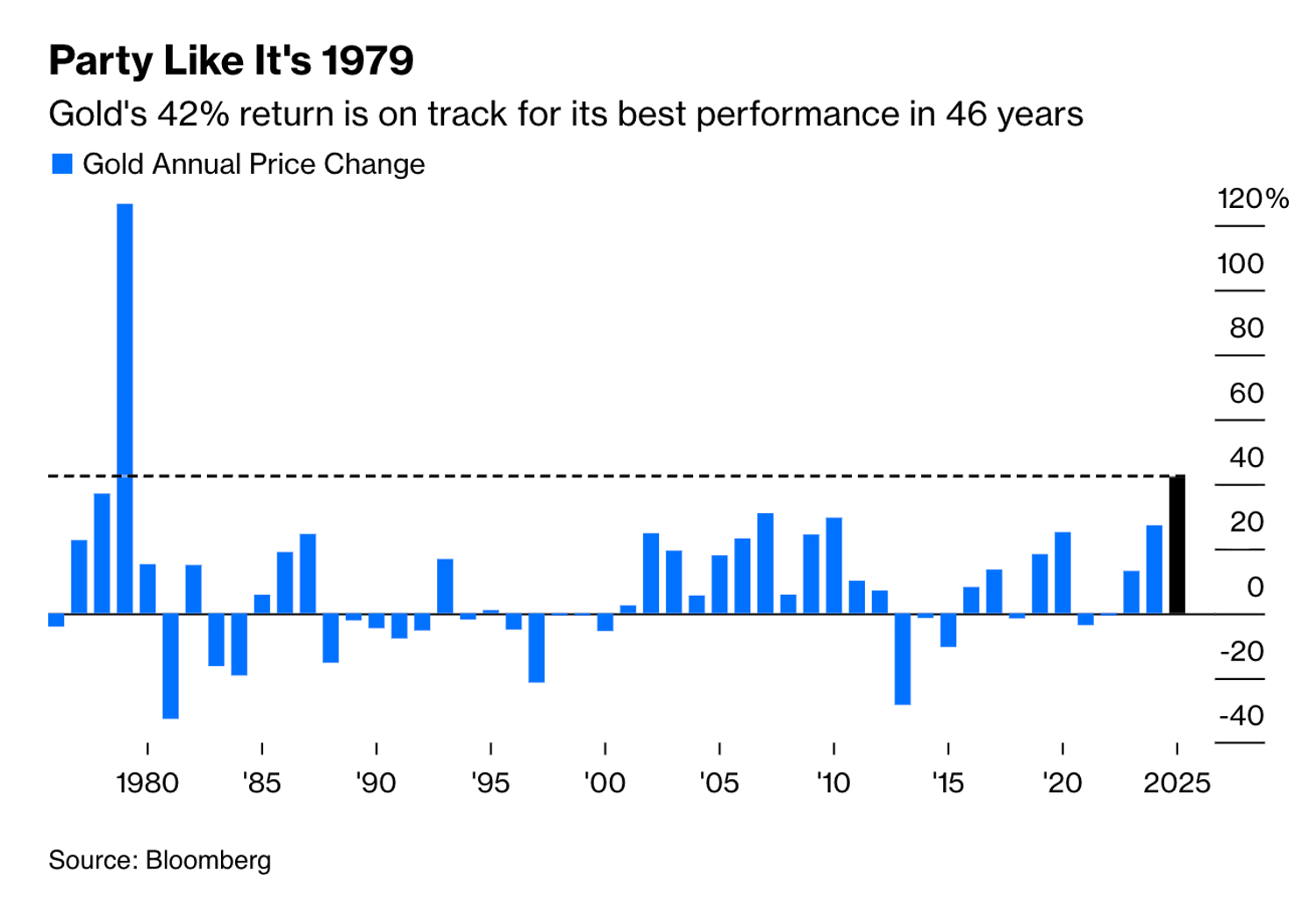

While BTC's monthly price saw a mere 0.2%, gold rose 10.7% in September, while silver climbed 12.65%. Gold has achieved its best annual performance since 1981.

In September, ETH's price fell 12.6%, while SPX rose 2.73%, QQQ rose 4.4%, and even IWM rose 3.34%.

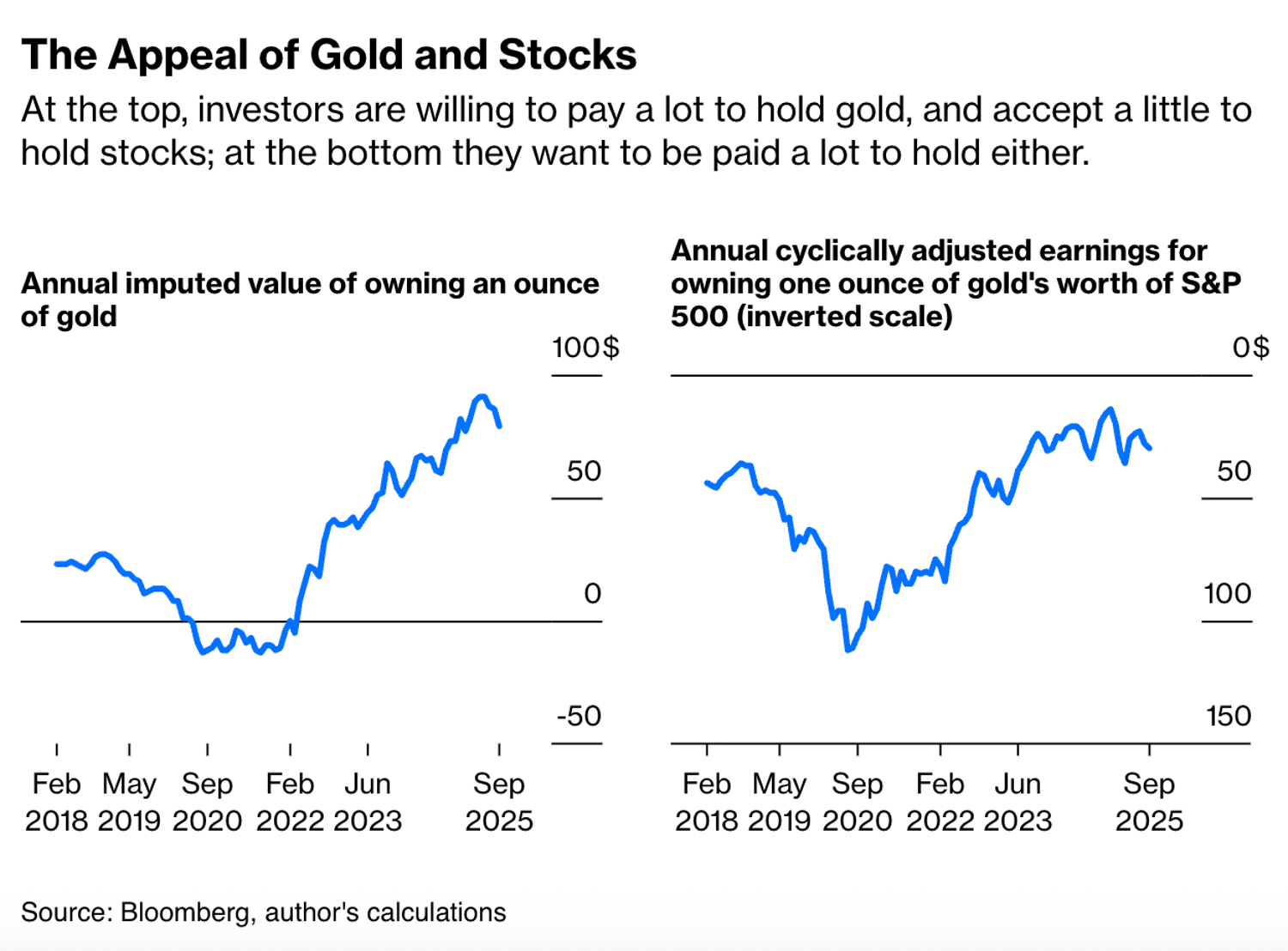

If we ignore the crypto market and simply compare gold to the US stock market, the popularity of gold since 2024 is also obvious. The liquidity support provided by Bessant through short-term bonds has not reversed this trend; currently, investors are willing to pay a certain cost to hold gold for the long term, and demand additional compensation for holding SPX for the long term, resulting in gold achieving an annualised carry of nearly 5% or even higher. In comparison, the SPX's annualised carry is less than 3.5% (roughly comparable to the yield of 2-year T-bills).

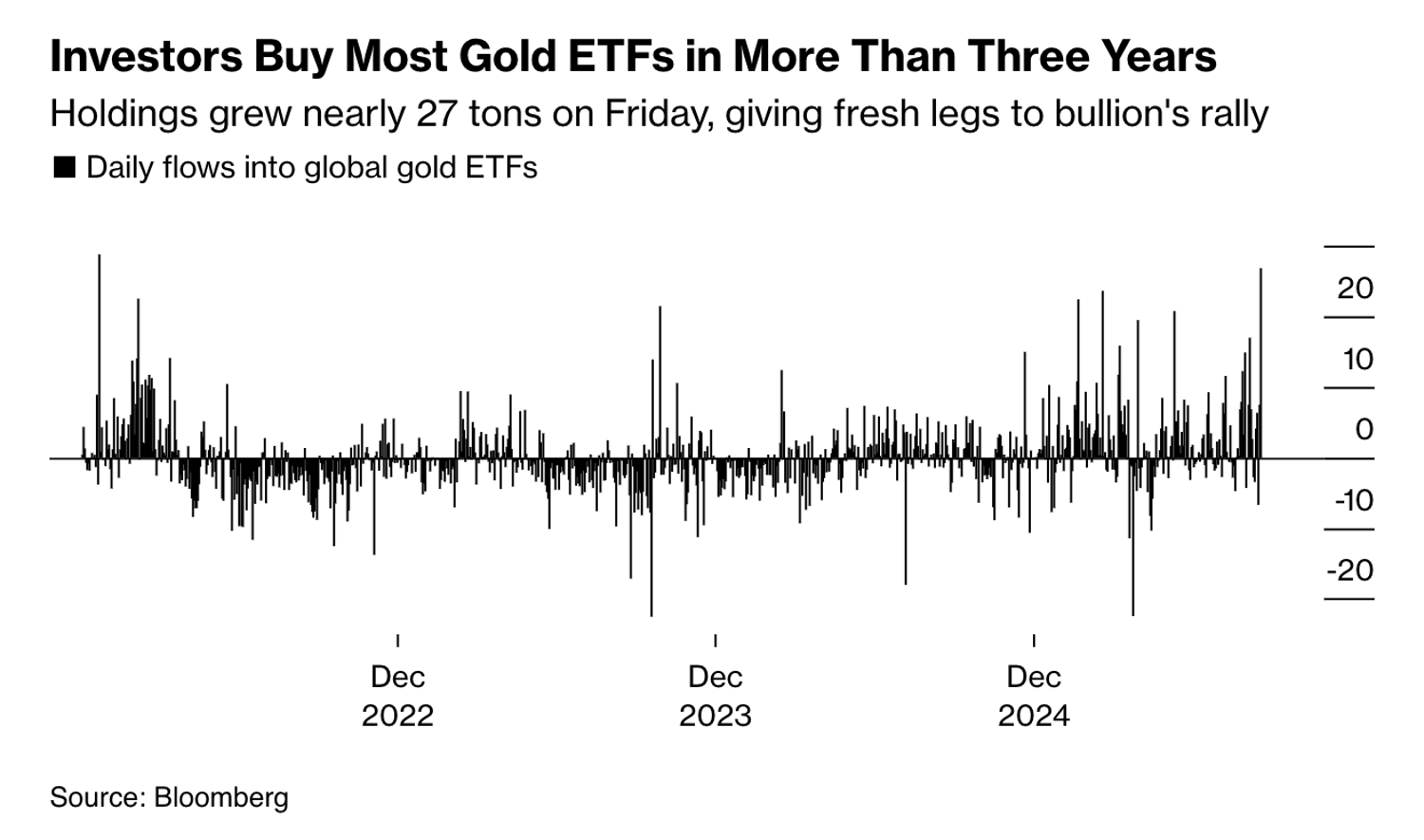

Therefore, it is not surprising that investors have flocked to gold. Gold ETFs have recorded their largest weekly inflows since 2022, and silver has been even more popular: open interest on SLV options is over 1.5 times that of GLD.

Admittedly, this situation is not common. Generally speaking, precious metals like gold and silver tend to underperform when the stock market hits new highs. This is because precious metals are traditionally considered safe-haven assets, and when risky assets perform well, investors tend to allocate more liquidity to stocks rather than gold. So, what causes gold and risky assets to move in the same direction?

"Onshore" vs. "Offshore"

For decades, the precious metals market revolved around the United States. Many countries held their gold and silver reserves in custody there, and New York City became a major trading centre for precious metals, even surpassing London at times. No one doubted the dollar's dominance at the time. The Eurodollar system was more convenient than gold, and using the dollar rather than gold in international trade and financial transactions was clearly more cost-effective.

This perception reached its peak in the 1990s: stock investors, bond traders, and precious metals trading firms alike were undeniably convinced that there was no "onshore" or "offshore" distinction for the US market. Investor preferences for gold and silver were entirely determined by liquidity allocation in the onshore market, with the offshore market playing a negligible role. Looking back at historical records before 2020, global markets largely followed this logic, with little change.

However, in the 2020s, several events have made institutional investors and traders realise that the views of the past few decades may be outdated. The US debt continues to reach record levels, with no end to the rising debt ceiling; the Eurodollar system faces threats from stablecoins; inflation is steadily eroding the dollar's value; and even the Federal Reserve itself faces challenges from the White House. In this context, "offshore" is no longer a minor corner of the global market, but has become a crucial market that cannot be ignored. The LME has established a massive gold vault in Hong Kong, and the CME is following suit; offshore demand and the offshore market are expanding at a rate far exceeding expectations.

As a result, the narrative of precious metals trading has gradually shifted offshore. The Fed is no longer the "almost sole variable" determining precious metals prices. A series of new narratives, such as "central bank gold purchases" and "alternative payment systems," have become the key drivers of gold's continued rise around 2024. For Bitcoin, the situation is similar to that of gold; a "parallel financial world" has emerged.

The stock market continues to follow the classic "onshore" operating logic compared to precious metals. Crypto assets heavily reliant on the US dollar, such as ETH and altcoins, also operate similarly to the US stock market. However, with the expansion of offshore markets, a considerable risk has emerged: investors are prioritising the onshore-offshore allocation ratio rather than the asset allocation ratio when allocating liquidity. Investors determine how much funding to allocate to onshore and offshore markets and then decide which underlying assets to invest in.

One direct consequence of these changes is a significant decrease in the long-term liquidity available to US stocks and some altcoin markets (the so-called "onshore market") compared to before. Liquidity held offshore will not easily return to the onshore market, meaning that stock market performance will depend more on domestic funds than global capital. Therefore, whether it's the Fed's statements or the impact of fiscal and monetary policies, the lack of additional lubrication provided by global capital will lead to more volatile onshore market fluctuations and even reverse transmission to the offshore market.

Of course, the White House, seeking greater government power, is not concerned about this situation. However, for the crypto market, the sharp fluctuations in the onshore market are already a potential threat (consider the performance of crypto assets listed via "DAT structure" in the past few months). Given the increasing risks of the Fed's monetary policy and the White House's deeper involvement in market operations in the coming months, the September settlement may only be the end of the "calm" period; it is more likely the beginning of a period of turbulence.

Economic Calendar of This Week

Thursday 12:30

- US GDP Growth Rate QoQ Final

- US Durable Goods Orders MoM

Thursday 14:00

- US Existing Home Sales

Friday 12:30

- US Personal Income MoM

- US Personal Spending MoM

- US Core PCE Price Index MoM

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.