Will Interest Rate Cuts Be Led by Administrative Orders?

The battle between Trump and the Federal Reserve came to a temporary halt before the September FOMC meeting. The two sides reached a compromise of sorts: the September rate cut was a sure thing, with the Bureau of Labour Statistics providing "sufficient data justification" for the move. Trump took no further concrete action after the cut was finalised.

However, this was merely the "calm before the storm." It must be acknowledged that Trump had already gained some advantages in this battle. Trump's dismissal of Fed Governor Tim Cook has profound implications for the Fed's independence, and the bond market has already partly reacted to this risk. A US court will soon rule on whether Trump's dismissal of Cook is valid. If so, it would mean Trump has complete control of the seven-member Federal Reserve Board. However, it's important to note that this doesn't equate to complete control of the 12-member voting committee of the FOMC, which also includes the five regional Fed presidents, who also vote on monetary policy.

The crucial date is February 2026. During this period, the Federal Reserve Board will vote on whether to confirm (or reject) the reappointment of five regional Fed presidents (who serve five-year terms). If the court upholds Cook's dismissal, the "four-member panel" consisting of Bowman, Waller, Miran, and Trump's newly appointed governors will only confirm those regional Fed presidents aligned with Trump's agenda (i.e., those inclined to support rate cuts). Trump will not only control this panel of 12 FOMC voting members, but will also ensure that at least two or three (or even all) of the reappointed regional Fed presidents align with him.

Even without considering the new Fed chair Trump will appoint in May 2026, by February 2026, he will already control the FOMC's voting committee, thereby steering the Fed toward a rate-cutting cycle. Therefore, Cook's dismissal has implications far beyond personnel changes; it also touches upon the independence of the Federal Reserve, and the court's ultimate ruling will be crucial. If the dismissal is upheld, Trump could potentially control the FOMC's dot plots as early as the March 2026 meeting.

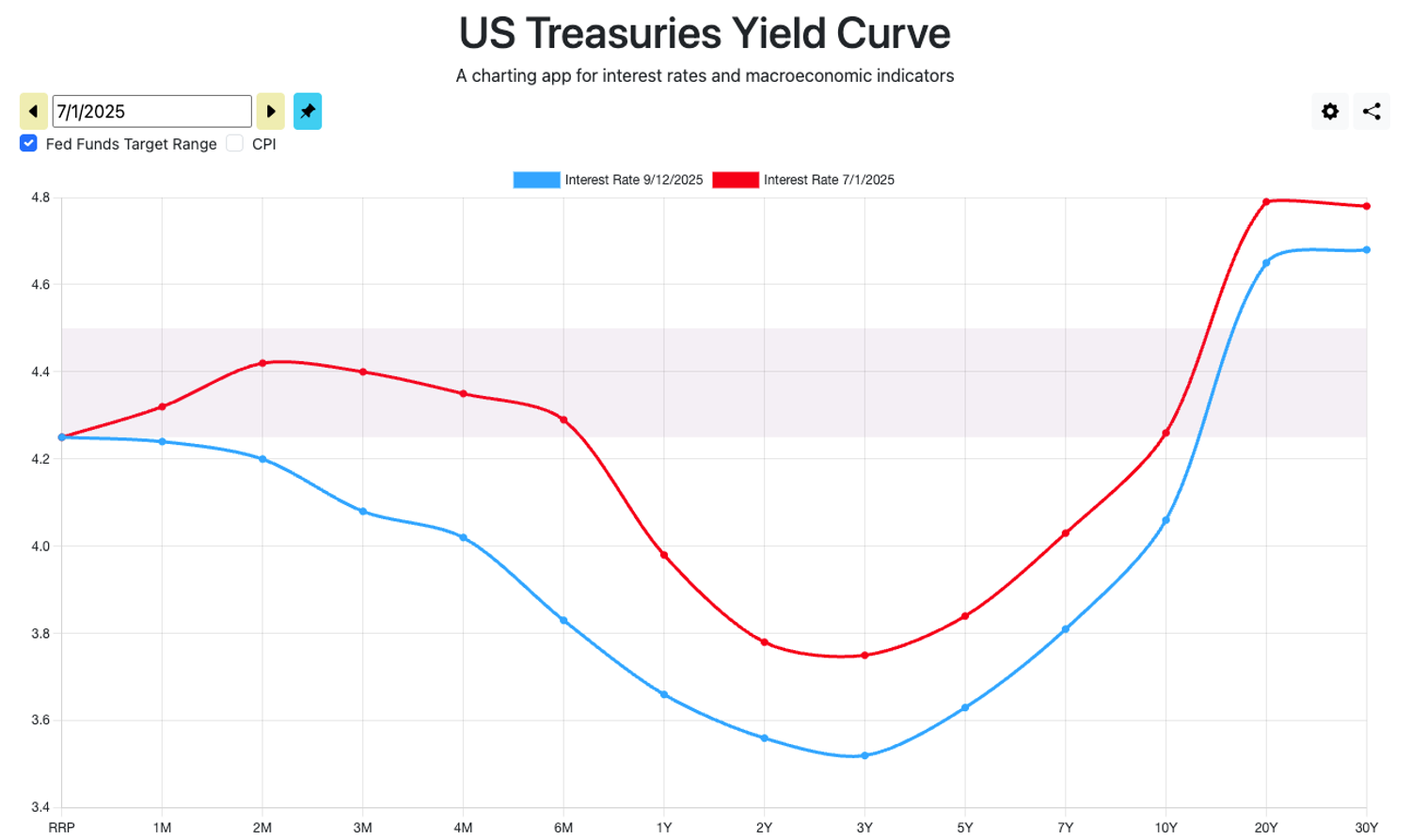

Source: ustreasuryyieldcurve.com

While traders don't view a "Trump Fed" as a positive development, it's clear that the probability of such an event is increasing. The bond market has already priced in a "Trump Fed" to some extent: T-bills' yields have continued to decline, while 2- and 3-year T-notes' yields have fallen further, pushing the bond yield curve further toward a "U-shaped" shape.

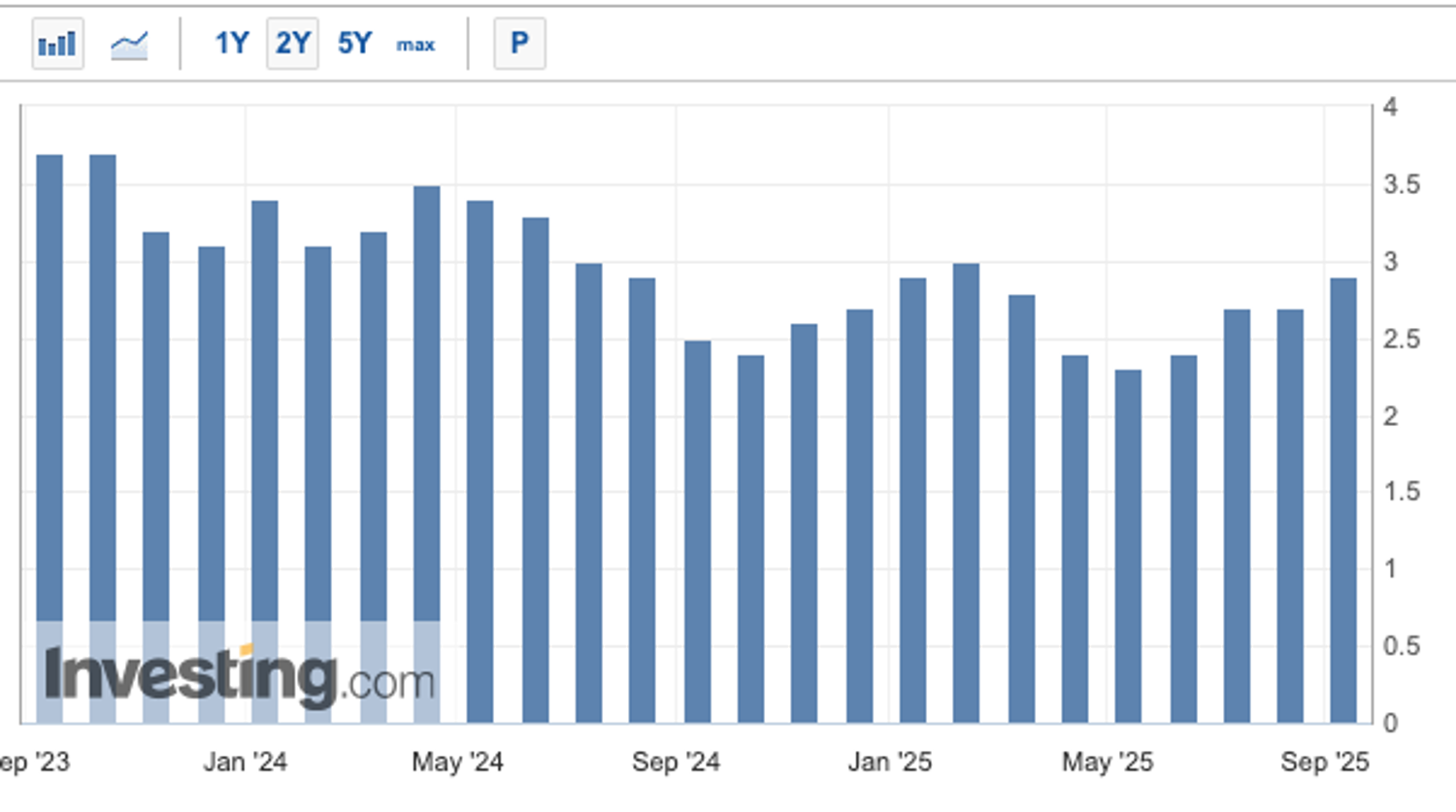

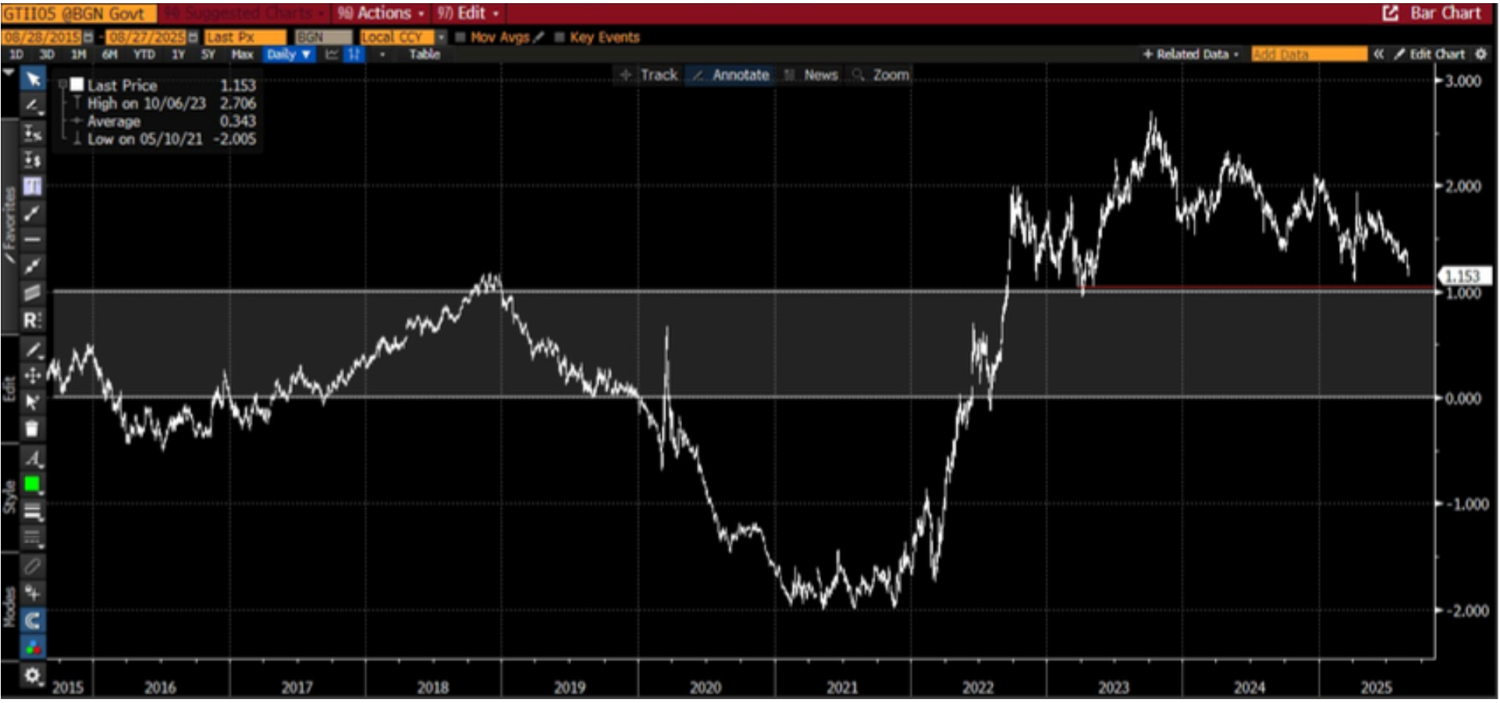

Meanwhile, US 5-year inflation swaps have just broken through a 12-month high, and the September preliminary estimate of the one-year inflation rate exceeded expectations. However, 5-year nominal yields continue to decline slowly, directly leading to a sharp drop in US 5-year real interest rates. Notably, the current real interest rate has fallen below 1%, suggesting that the market is positioning for a new round of QE from "Trump's Fed". US real interest rates have remained above this level (indicating a somewhat tightening policy environment) since 2022, and are now trending back toward pre-pandemic levels.

5-year US inflation swap VS 5-year US nominal yields. Source: Bloomberg

As for inflation? It seems "no one cares." Under the "Trump Fed" scenario, the decision to cut interest rates hinges on the White House's preferences and whims. Meanwhile, inflation, which has risen for four consecutive months since May, is viewed by the White House as "not a problem." Even if "Trump's Federal Reserve" is not ultimately realised, Bessent can actually control the real interest rate through fiscal operations, which is one of Trump's "trump cards."

Source: Investing.com

But it is clear that institutional traders have not ignored the impact of inflation and deficits. The US primary fiscal deficit currently exceeds 3%, compared to a pre-pandemic deficit of only 1%–1.5%. The market indicator of "fiscal dominance," the spread between 30-year T-bond yields and 5-year T-note yields, is also breaking higher. Traders' positioning suggests that while Trump may have a significant impact on interest rates in the short term, the current disregard for inflation and aggressive borrowing will lead to a heavier debt burden in the long term. Furthermore, given the questionable sustainability of these policies and the lack of expectations, traders are demanding higher risk premiums for holding T-bonds, both for risk management and self-management of macro risks, pushing up long-term bond yields and financing costs.

Changes of US primary fiscal deficit. Source: Bloomberg

Source: Bloomberg

How to Trade?

For the onshore market, one direct consequence of rising long-term financing costs is a significant shortening of investors' investment durations. Liquidity releases primarily come from the short term, not the long term, making it difficult for investors to hold high-quality underlying assets for the long term. This makes it more difficult for investors to hold onto specific high-quality underlying assets for the long term, and they are more inclined to hold assets with better short-term performance. Consequently, the pursuit of "trend stocks" and "narratives," as well as a preference for small- and mid-cap stocks and altcoins, may offer better short-term returns than the SPX and defensive stocks.

Unlike 2021, the current proportion of short-term financing in the stock and crypto markets is significantly higher due to the increasing T-bills proportion, approaching levels seen at the end of 1999. This means that the share of "speculative funds" in the market may continue to increase with interest rate cuts; therefore, shortening trading cycles is necessary. Stop-loss/take-profit strategies based on yield rather than absolute returns are particularly useful at this time.

For long-term investors, a shift to offshore becomes necessary. With the Federal Reserve becoming "Trump's Fed," coupled with the potential for a resurgence in CPI, the risk of dollar-pegged assets has significantly increased, which is within expectations. Therefore, the demand for alternative payment systems to the dollar will continue to grow over the next few years.

As a result, investment in the US stock market remains sustainable, but the proportion should be appropriately reduced and concentrated in ETFs and indices rather than individual stocks. Furthermore, one can consider increasing the allocation to gold, Bitcoin, and non-US FX, while allocating some funds to emerging stock markets with relatively long average sovereign debt maturities.

However, the implementation of this strategy requires two conditions: 1) stubbornly high inflation, and 2) the Supreme Court of the United States (SCOTUS) permitting Trump to fire Cook, thereby controlling the FOMC. We haven't reached that point yet, but regardless, "inflation-ignoring rate cuts" is a macroeconomic scenario worth considering.