What most warrants reappraisal in 2026 is not the linear question of whether growth will be stronger, but the fact that markets are increasingly working with a different pricing grammar. For roughly two decades, asset returns have tended to rest on two tacit assumptions. First, supply chains were organised to maximise efficiency, keeping costs down and inflation contained. Secondly, central banks provided decisive backstops during stress, systematically compressing risk premia. Both assumptions are now weakening. Supply chains increasingly prioritise control and redundancy; fiscal and industrial policy more frequently feeds directly into earnings expectations; and geopolitics has shifted from a tail risk to a persistent source of noise. In that sense, “regionalisation” is less a slogan than a change in the constraints under which the economic system operates.

Within this framework, the central task is not to bet on a single macro outcome, but to realign exposures towards three more observable “hard variables”: supply constraints, capital expenditure, and policy-backed order flow. Together, these variables point towards a familiar cluster of assets—commodity-linked equities, the AI infrastructure stack, defence and security themes, and selected non-US markets that can improve a portfolio’s correlation structure. Meanwhile, the core question in rates and sovereign bonds is no longer how much of a tailwind a “rate-cut narrative” can deliver, but how a reshaped term structure redistributes returns.

Regionalisation: Not “Decoupling”, but a New Cost Function

Treating regionalisation as synonymous with full-scale decoupling tends to understate its practical significance. A more accurate description is that the objective function of globalisation has shifted from “efficiency at all costs” to “efficiency subject to security constraints”. Once security becomes binding, variables that previously sat outside most valuation models, such as supply-chain redundancy, energy security, access to critical minerals, export controls on strategic technologies, and the rigidity of defence budgets, begin to show up in discount rates and earnings assumptions in tangible ways.

Two immediate consequences follow for asset pricing. First, risk premia become less likely to revert to structurally low levels: political and policy uncertainty turns into a day-to-day input, and markets demand compensation for bearing it. Few investors willingly carry “Cuban equity risk”; in the current regime, even US equities can no longer assume that risk is priced at zero.

Secondly, global beta explains less, while regional alpha matters more. Under different geopolitical blocs and policy functions, the same growth and inflation prints can translate into materially different valuations and capital flows. For allocators, diversification in a regionalised world increasingly means diversifying by supply-chain position and policy sensitivity—not simply spreading exposure across countries.

Equities: From “Buying Growth” to “Buying Position”

If equity allocation between 2010 and 2021 essentially amounted to “buying growth alongside falling discount rates”, 2026 looks closer to “buying position”. Position, in this context, is a market’s location on three maps: the resource map, the compute map, and the security map. As supply-chain autonomy and critical infrastructure resilience move up the agenda, markets at key nodes can command structural premia—even when domestic macro conditions are less than ideal.

In a world where security becomes a first-order priority, increasing inventories of gold, silver, copper, and other industrial metals can be rational even without immediate end-use demand. Supply chains can be disrupted abruptly—trade tensions have already shown how quickly frictions can turn into cost shocks. That reality pushes major economies towards larger strategic mineral buffers. Structural uplift in critical minerals demand, combined with long-cycle supply constraints, makes commodities behave more like supply-side assets than mere mirrors of the business cycle.

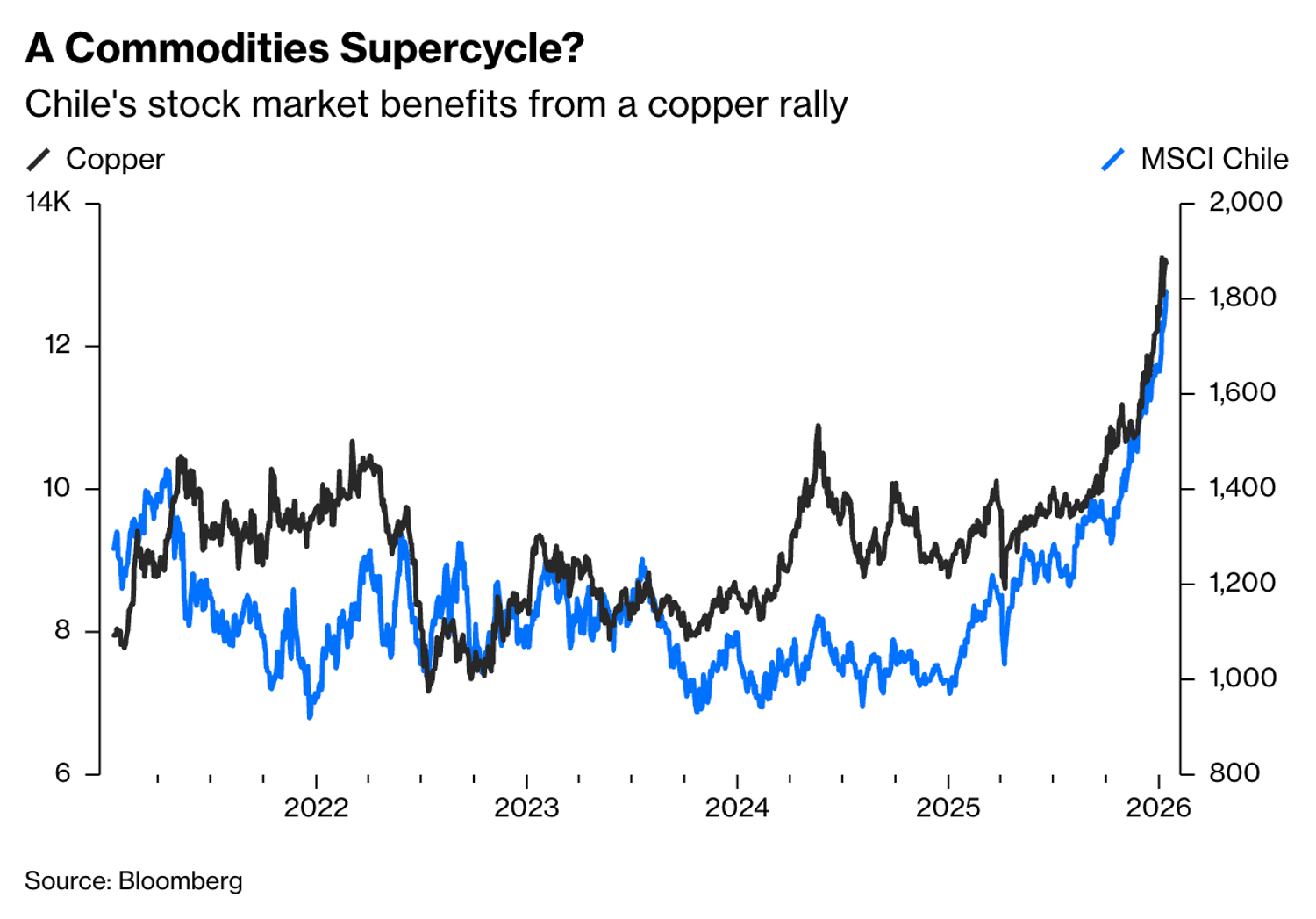

This logic strengthens the case for allocating to resource-endowed equity markets. Copper-linked equities in countries such as Chile partly reflect the foundational demand created by electrification and the build-out of industrial infrastructure. Precious metals and broader resource equities in markets such as South Africa, meanwhile, carry a double-edged profile: on the way up, earnings and FX can reinforce one another; in risk-off phases, politics and external financing conditions can magnify volatility. Resource-country equities, therefore, fit better as “supply-constraint factors” within a portfolio than as generic emerging-market beta.

A second central theme is AI. Application-layer narratives easily capture discussion, but capital allocation is often better anchored in what sits plainly on balance sheets: compute, power, data centres, networking and cooling. The common feature across these segments is greater capex visibility, frequently reinforced by both policy and industrial strategy. Rather than treating AI as a software valuation cycle, it can be framed as an infrastructure build-out: rising compute density ultimately translates into demand for electricity and engineering, shifting a larger share of returns towards upstream and midstream physical capacity.

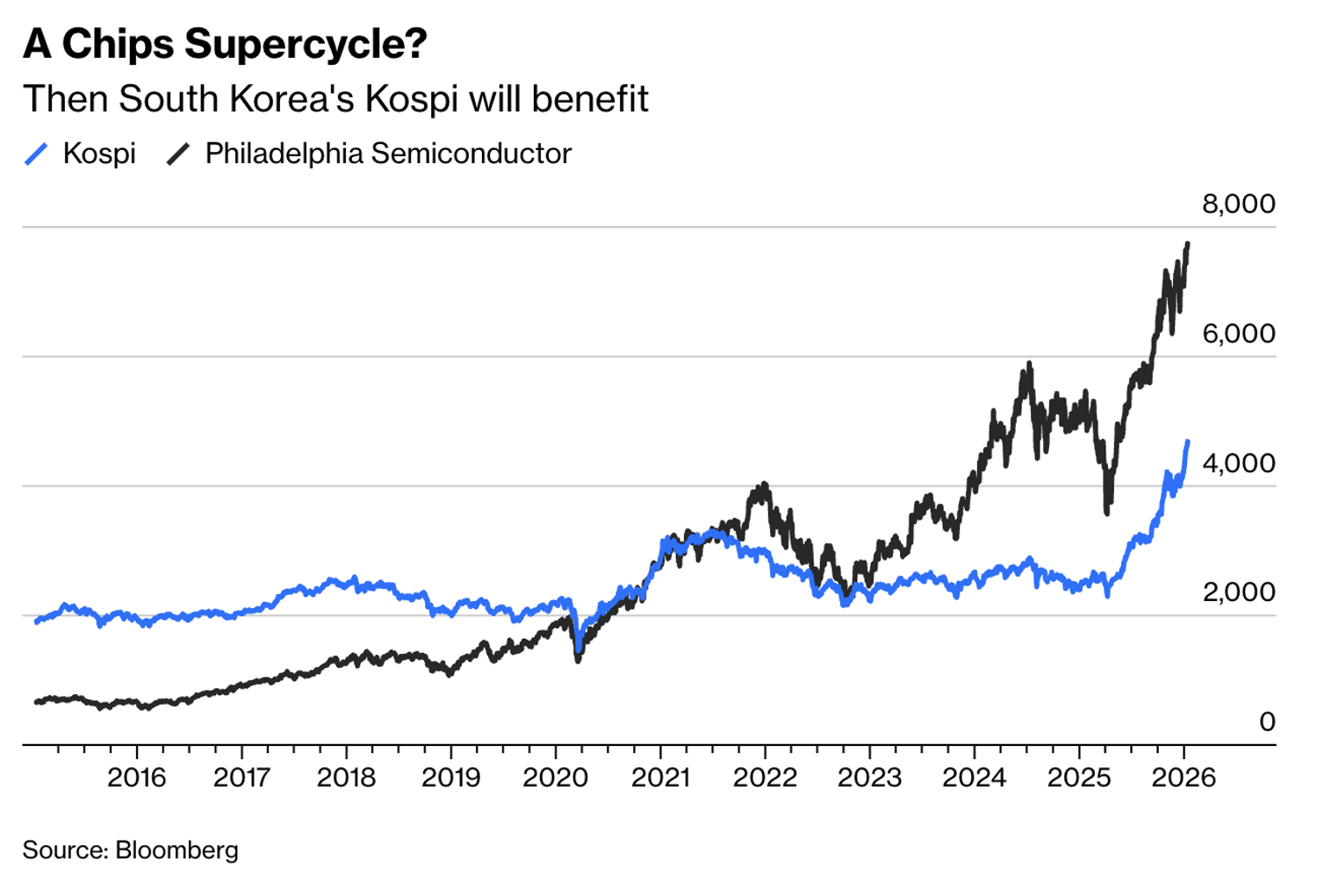

Under regionalisation, higher requirements for redundancy and localisation raise the strategic value of critical hardware and intermediate inputs. Markets such as South Korea—home to key semiconductors and electronics linkages—often provide a more direct equity expression of the AI capex cycle, precisely because they sit at the industrial interface of global compute infrastructure. From a portfolio perspective, the appeal lies not only in higher growth potential but in more visible capex and more durable policy support.

Defence and security have likewise returned to the forefront of investor attention for the first time since the end of the Cold War. Influenced by a more transactional US foreign policy posture and the Russia–Ukraine war, both the United States and Europe have elevated defence and security as strategic priorities. The defining feature of defence-linked assets is that demand is not driven by marginal household consumption, but by a fiscal function constrained by national security. Once budgets step up, political resistance to reversal tends to be strong, improving order visibility. That gives defence and security equities a more defensive role in a regionalised regime: as conflict and sanctions risk rise, they can add resilience at the portfolio level.

Still, defence and security often reprice ahead of fundamentals. Rapid, event-driven reratings followed by mean reversion are common. A more robust positioning is to treat the theme as tail-risk insurance or a risk-hedging factor, rather than as a straightforward growth compounder. Its value is in limiting drawdowns, not in delivering consistent outperformance every quarter.

Hong Kong SAR and China assets also merit consideration. Describing them simply as “cheap” is incomplete; their allocation value typically comes from two sources. First, risk pricing often embeds pessimism early, creating rebalancing optionality. Secondly, their policy functions and sector composition differ from those of the those of US and European markets, which can improve the correlation structure. In a regionalised world, correlations do not automatically fall; they can rise during stress, making structurally differentiated exposures more useful as hedges.

Rates & Treasuries: Staying Steep in a Term-Premium Regime

The core tension in 2026 rates can be summarised simply: the front end largely responds to the policy path, while the long end behaves more like a term premium vessel. Rate-cut expectations can pull short yields lower, but whether the long end follows depends on whether inflation tail risks, fiscal supply pressure and political uncertainty allow term premia to compress further. Put differently, long-end “stubbornness” does not necessarily mean markets have miscounted the number of cuts; it may simply reflect markets charging again for long-horizon risk.

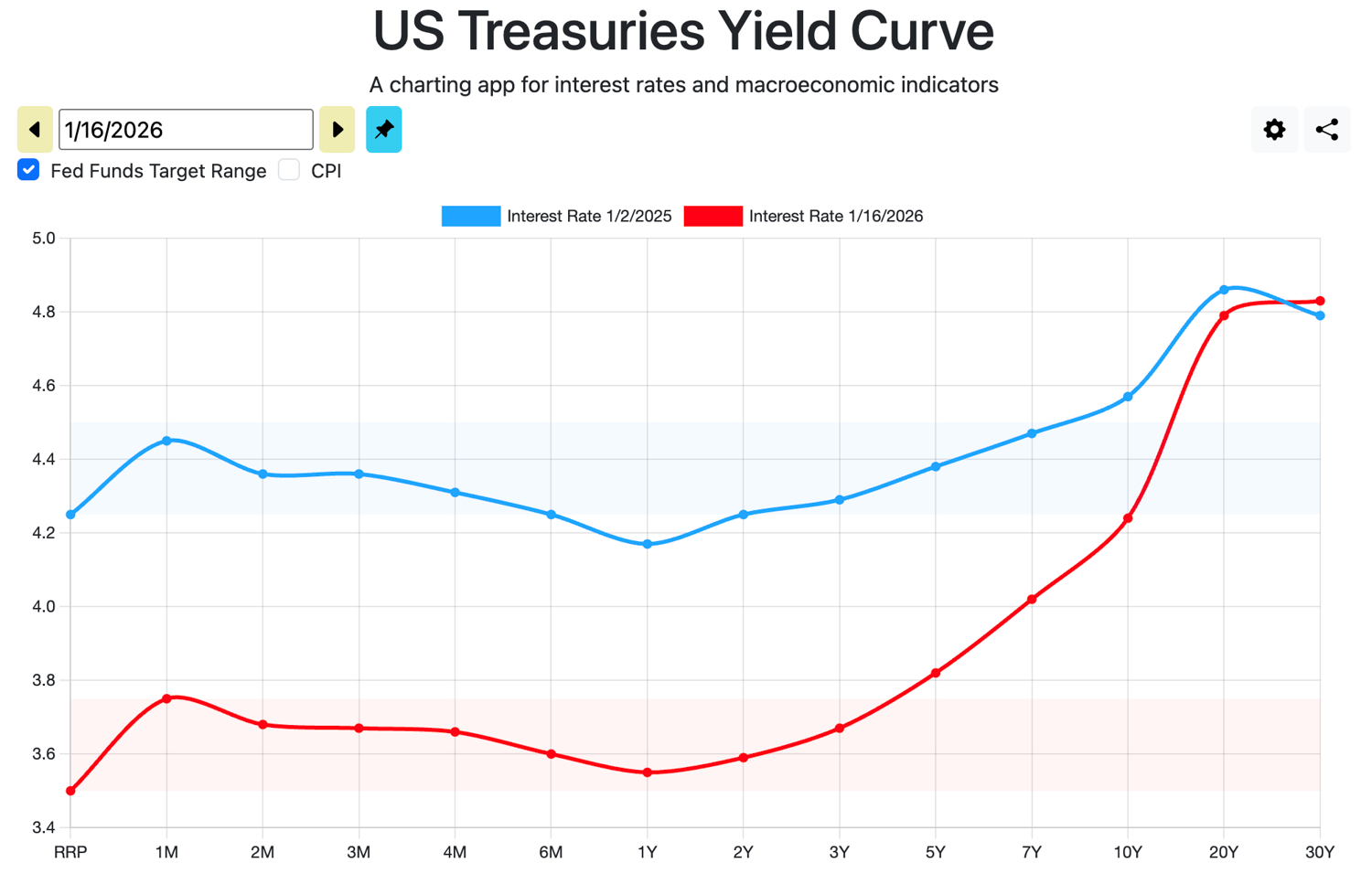

Compared to the same period last year, the yield of T-bills has declined significantly, but the decline has become smaller as the duration increases, while the yield of T-bonds has hardly dropped. Source: ustreasuryyieldcurve.com

Supply dynamics reinforce this structural divergence. Shifts in US Treasury financing strategy directly affect supply–demand balance across maturities: the front end is often absorbed more readily when money-market capacity is strong, whereas the long end is more prone to impulse moves driven by risk budgets and term-premium repricing. The portfolio implication is straightforward: duration is best managed in layers, avoiding a single-path bet that “inflation disappears and term premia return to extreme lows”. Curve-structure trades—steepeners in particular—persist not because they are clever, but because they align with the different pricing mechanisms at the front and back ends of the curve.

Crypto: Ring-fencing “Digital Commodity” Exposure from Second-Tier Risk

The key issue for crypto in 2026 is not whether the complex rises, but how sharply internal differentiation increases. Bitcoin is more readily framed as a non-sovereign asset with rules-based supply and cross-border portability—hence its tendency to attract alternative-asset and hedging demand under a regionalisation narrative. By contrast, a number of tokens sit closer to equity-like risk assets: their pricing depends more heavily on growth stories, ecosystem expansion and risk appetite. When risk-free rates remain attractive, regulatory frameworks become clearer, and traditional capital markets offer more mature routes for funding and exit, equity-like tokens need to offer meaningfully higher risk compensation to remain compelling from an allocation standpoint.

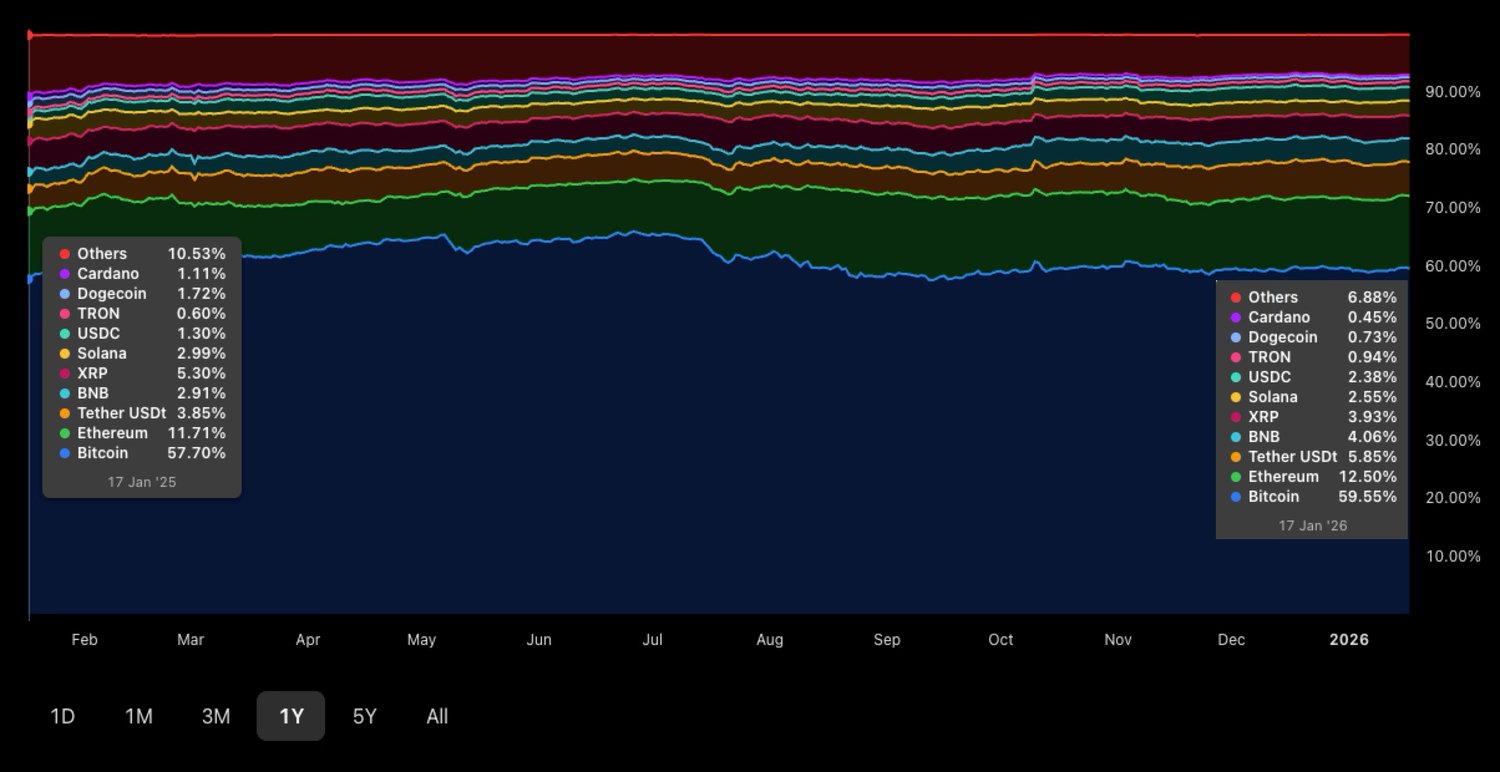

Clearly, altcoins have struggled to attract investor interest over the past year, and their market share has declined further. Source: Tradingview

For that reason, crypto exposure is better managed through ring-fencing than through a single basket. Bitcoin fits more naturally within a commodity/alternatives sleeve, where small weights can buy asymmetry at the portfolio level. Equity-like tokens are better treated as high-volatility risk assets, subject to stricter return hurdles and explicit risk budgets. In a regionalised regime, the aim is not to embrace every new instrument, but to identify which exposures remain intelligible under the new constraints.

Anchor on Hard Constraints, Monetise Structural Divergence

Taken together, the 2026 portfolio increasingly resembles the management of hard constraints. Supply constraints restore the strategic character of commodities and resource equities. Capex visibility supports the AI infrastructure stack. Policy-backed order flow underpins the resilience of defence and security. Term-premium repricing reshapes duration’s return distribution. Selected non-US exposures can provide reflexive hedging through valuation structure and policy-function differences.

None of this requires perfect prediction of each headline. The scarcer skill in a regionalised era is building portfolios that rely less on flawless forecasting: hard assets and infrastructure absorb structural demand, curve structure expresses structural divergence, and hedging factors absorb structural noise. Trading in 2026 is less about guessing the answer and more about recognising the constraints, then reshaping allocation priorities accordingly.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.