Introduction

The stablecoin market experienced severe turbulence recently, with several prominent synthetic stablecoins, such as USDX and xUSD, suffering catastrophic depegging events.

The incidents have brought scrutiny to three critical pillars of DeFi’s evolving architecture:

- Synthetic stablecoin mechanisms: the design and sustainability of delta-neutral, hedged “stable” assets.

- Curator-model lending protocols: delegated risk management, designed to segregate risk, ultimately leads to risk concentration.

- Systemic risk through interdependence and recursive lending: the hidden leverage loops that link seemingly isolated protocols.

Recent Stablecoin Depegging Events

The first week of November 2025 marked one of the most chaotic periods for decentralized stablecoins since the Terra/Luna collapse. Within days, three major synthetic dollar tokens, USDX, xUSD, and deUSD, lost their pegs.

USDX Depeg: USDX, a $683 million synthetic stablecoin from Stable Labs, collapsed from $1 to as low as $0.09. Marketed as a delta-neutral, yield-bearing dollar proxy, USDX relied on hedged futures positions rather than cash reserves. The unwind began when wallets linked to its founder allegedly used large amounts of USDX as collateral to borrow USDC and USDT across multiple lending protocols, draining liquidity and leaving USDX under-collateralized.

Stream Finance and xUSD: Only days before USDX’s crash, Stream Finance shocked investors by revealing that an external fund manager had lost $93 million in off-chain positions. Withdrawals were frozen, and its flagship stablecoin, xUSD, plunged 77% within 24 hours. xUSD is also a delta-neutral strategy stablecoin.

Elixir and deUSD Contagion: The collapse didn’t end with Stream. Elixir Network, issuer of another stablecoin, deUSD, had quietly lent $68 million to Stream through the Morpho protocol. When Stream froze withdrawals, Elixir’s assets became effectively trapped. With redemptions halted, deUSD plunged to around $0.04.

Analysts later revealed that both Stream and Elixir had been engaged in recursive cross-lending, using each other’s tokens to inflate TVL. Together, USDX, xUSD, and deUSD triggered a chain reaction across lending markets. Hundreds of million in loans backed by these assets became distressed, spreading losses through lending protocols such as Euler, Silo, and Morpho.

Delta-Neutral Strategies and Structural Weakness

Stablecoins in these incidents (USDX, xUSD, deUSD) share a similar architecture: the delta-neutral trading model. Delta-neutral stablecoins aim to maintain their peg without traditional fiat reserves by using hedging strategies.

How Delta-Neutral Stablecoins Work

A delta-neutral stablecoin is typically backed by crypto assets and uses derivatives to hedge price risk. The goal is to create a crypto-collateralized dollar that doesn’t fluctuate with the crypto market. The mechanism works roughly as follows:

- Collateral and Hedging: The issuer collects crypto deposits (e.g., ETH or staked ETH (stETH)) as collateral. Against this, the protocol mints an equivalent amount of stablecoins. To neutralize the collateral’s volatility, the protocol simultaneously takes a short position in the collateral via futures or perpetual swaps. For example, if the collateral is 1 ETH (long exposure), the system would short 1 ETH on a futures exchange. This pair of positions, long spot ETH and short ETH futures, creates a hedged position that should hold a stable net value. If ETH’s price moves, the gain/loss on the collateral is offset by the loss/gain on the short.

- Yield Generation: Delta-neutral setups are not just about stability; they’re also about yield. The stablecoin protocols typically earn funding rate payments from the futures market (when traders are bullish, longs pay shorts a periodic fee) and may also earn staking yield on staked collateral like stETH.

This model, employed by projects like Stable Labs (USDX), Elixir (deUSD), Stream (xUSD), and also Ethena (USDe), was seen as a way to achieve a decentralized stablecoin without relying on fiat reserves. When market conditions are normal, these systems can work remarkably well, and indeed many saw rapid growth.

Structural Weaknesses Exposed

Recent depeg incidents reveal several vulnerabilities for delta-neutral synthetic stablecoins.

- Centralized Exchange Dependence: Despite branding themselves as decentralized, many synthetic stablecoins rely on centralized exchanges for liquidity and hedging. For instance, maintaining the delta-neutral hedge often means shorting on major exchanges like Binance or OKX, since that’s where the liquidity is. This introduces several risks incompatible with a “stable” asset. Firstly, one has to trust the exchange’s solvency and proper functioning, if an exchange were to freeze funds or get hacked, the stablecoin’s hedges could be in jeopardy. Secondly, during market stress, CEX liquidity can evaporate or prices can dislocate, which can undermine the peg even if on-chain assets are fine.

- Off-Chain Counterparty Risk: Delta-neutral stablecoins still depend on centralized or off-chain entities in executing the trading strategies. For example, Stream Finance entrusted an external fund manager with a large portion of its capital, and that trust was betrayed with a $93M loss.

In October’s market crash, a wave of automatic deleveraging (ADL) across centralized exchanges broke many delta-neutral strategies. One leg of their hedge (often the short) could be closed or auto-liquidated first because of “automatic deleveraging” (ADL) mechanisms on perpetual futures platforms. ADL is when a profitable trader’s position is forced closed because the counterparty pool is exhausted, leaving the counterparties with the losing side. When one leg disappears or dramatically changes, the intended hedge breaks: the portfolio is no longer neutral, and the remaining leg either gains large losses or loses large gains.

Ethena, the largest delta-neutral strategy stablecoin, avoided losses thanks to bespoke agreements with exchanges to immune from ADL mechanism so that insulated its exposure, others weren’t so fortunate.

Contagion Through Curator Model Lending Protocol and Recursive Leverage

The rise of curator-based lending protocols such as Morpho and Euler in the 2024-2025 cycle has played a pivotal role in the recent DeFi turmoil.

The Curator Model Lending Protocol

At their core, these protocols use a curator model to decentralize risk management and optimize capital efficiency. Instead of a monolithic pool like Aave or Compound, curators, typically sophisticated entities, design isolated lending markets with tailored parameters for specific collateral and borrowing assets.

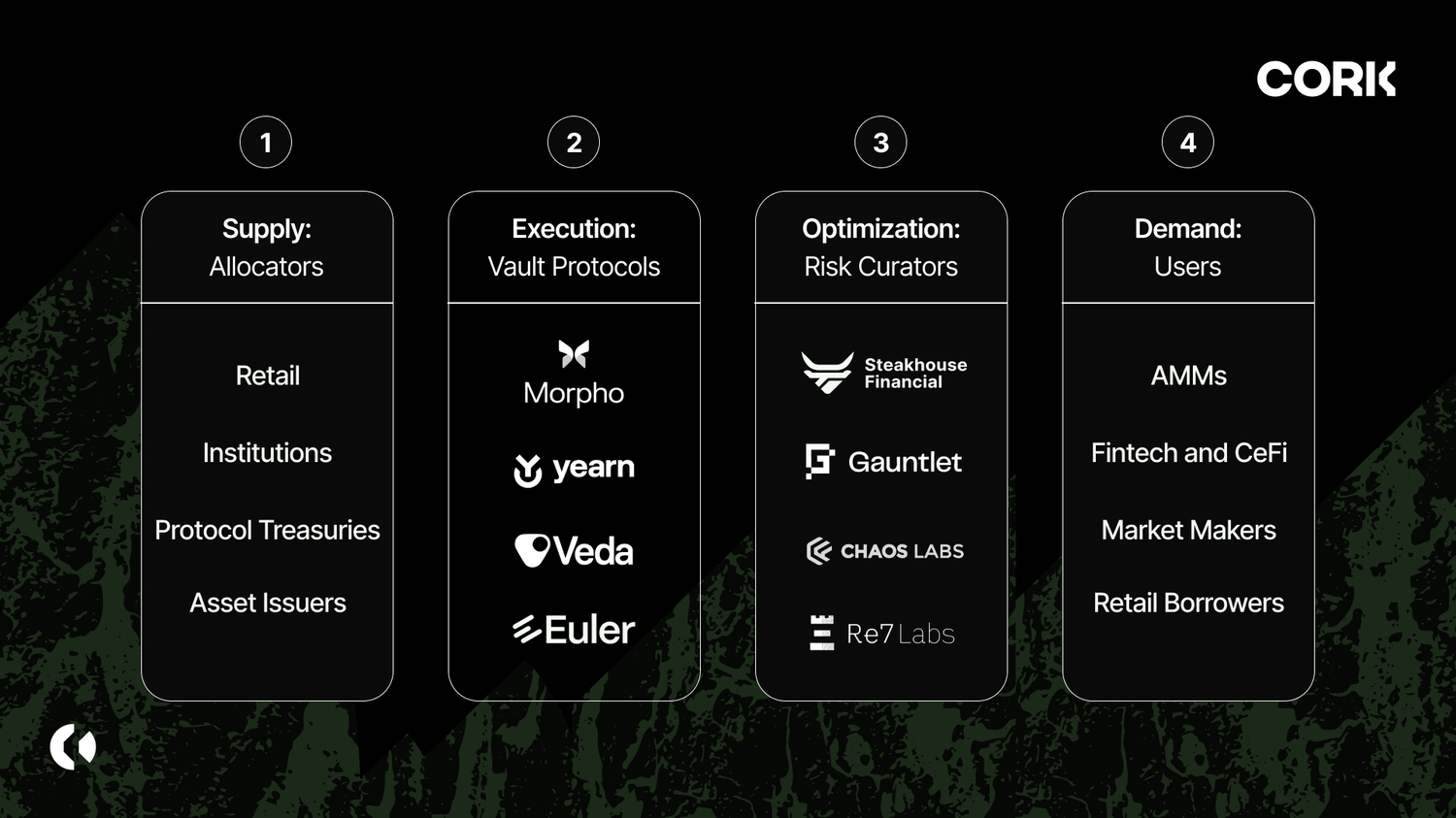

Risk Curator Lending Stack

Source: https://www.cork.tech/blog/onchain-vault-ecosystem

The curator model was designed to segregate risk across isolated lending markets, but in practice it has done somewhat the opposite, concentrating exposure through homogeneous strategies and correlated collateral choices.

Curators are like on-chain fund managers: they decide how to deploy the pool’s liquidity for yield. However, as competition for returns intensified, many curators converged on similar high-yield approaches, typically involving leveraged stablecoin loops built on assets such as Stream’s xUSD and other yield-bearing tokens.

Instead of diversification, this led to concentration: dozens of nominally separate pools chasing yield in the same direction, with the same collateral base. When one of these underlying assets suffered a failure, the damage propagated rapidly.

Recursive Leverage

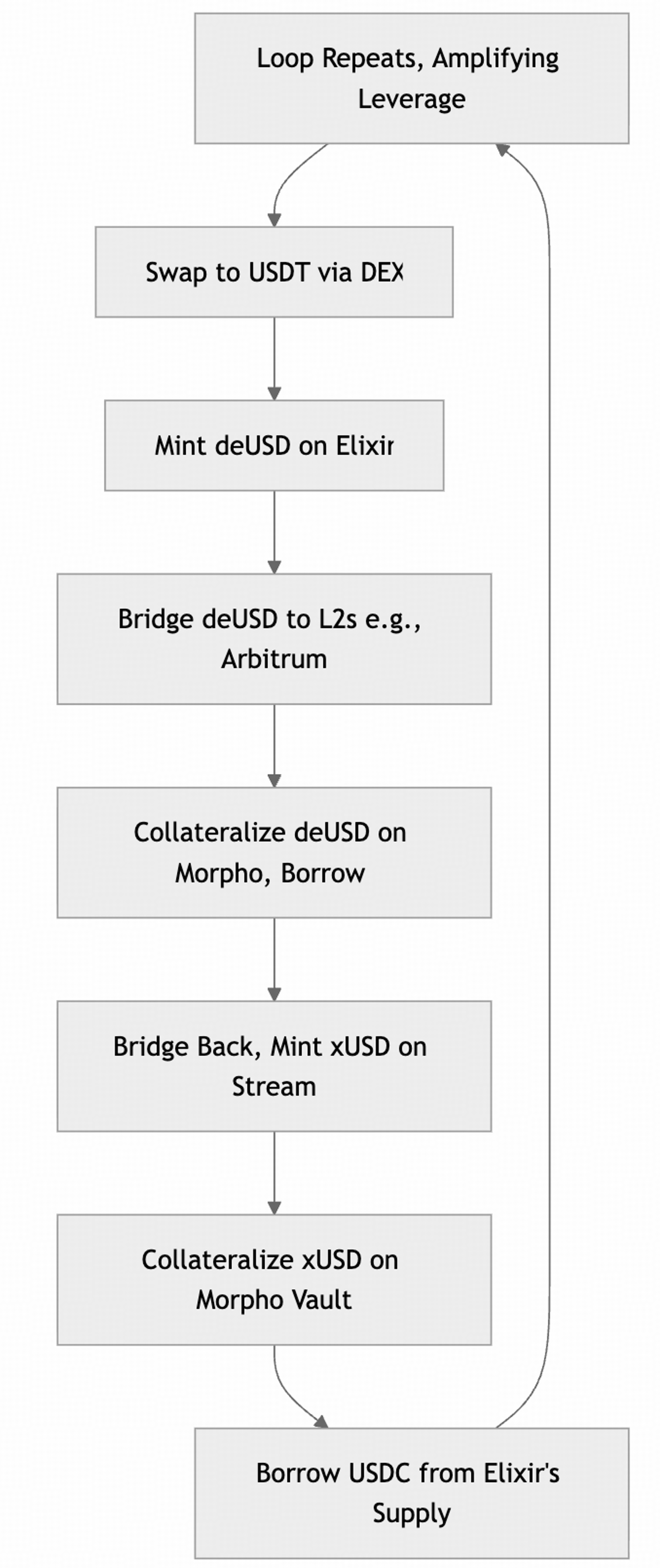

DeFi protocols often allow collateral reuse and looping, which is called Recursive lending. It involves using borrowed funds as new collateral to take out additional loans, creating a self-reinforcing loop, in order to multiply exposure to both lending yields and token incentives, without needing extra external capital.

For example:

- Deposit 100 USDC.

- Borrow 75 USDC against it.

- Re-deposit that 75 USDC as new collateral.

- Borrow again (e.g., 56 USDC), and repeat several times.

After a few loops, you might end up with an effective exposure of 300–400 USDC from your original 100 USDC deposit.

We saw this vividly with Stream and Elixir. Stream utilized “recursive looping,” essentially reusing its own xUSD tokens as collateral to borrow more, re-deposit, and so on. The two systems are interlinked, using each other’s assets as collateral in a closed-loop arrangement. Approximately 40% of the total supply is backed by external capital, with the remainder generated through internal lending loops.

How Investors Navigate the Risks

Understand the Stablecoin You’re Using

Fiat-backed and regulated stablecoins (such as USDC or USDT) are the safest, as they are redeemable 1:1 for fiat and backed by verifiable reserves like cash or U.S. Treasuries. These stablecoins are designed for redemption stability, not yield.

In contrast, algorithmic, synthetic, or mechanism-driven stablecoins derive stability from trading strategies or arbitrage incentives rather than tangible assets. Their “stability” depends on the underlying strategy or mechansiam, making them more akin to structured investment products than true stablecoins.

Investors should therefore differentiate between payment-grade stablecoins used for settlement and yield-bearing or experimental stablecoins, which carry higher risk. The latter should not be treated as safe cash equivalents.

Know the Lending Protocol and Its Risks

Established, time-tested protocols such as Aave are generally safer choices. Their mechanisms have been extensively audited, battle-tested across market cycles, and scrutinized by large communities of developers, auditors, and professional investors. While no protocol is risk-free, their longevity and transparency make catastrophic failures less likely.

In contrast, newer or experimental lending protocols that promise higher yields or feature “innovative” mechanisms often carry unidentified or poorly understood risks. Yield differentials often reflect risk premiums, not free opportunities. In DeFi, if a yield looks high, it likely compensates for unseen structural or smart contract risk.

Recognize Counterparty Risk in CeDeFi

Moreover, the emergence of so-called CeDeFi (Centralized Decentralized Finance) deserves careful scrutiny. DeFi offers full transparency and self-custody, while CeFi inherently introduces counterparty risk. Any system involving intermediaries, be it a fund manager, custodian, or centralized exchange (CEX), cannot be considered DeFi. And when they are considered as CeFi, detailed, timely, and verifiable transparency reports are essential to maintain user confidence and mitigate systemic risk.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.