From Market Swings to Governance Risk

A more widely shared view is emerging: what many describe as “loss of control” is not an emotional reaction to a single headline, but a rational repricing of institutional boundaries being repeatedly tested—and possibly crossed. The criminal investigation involving Powell goes to the heart of modern finance: central-bank independence. If monetary policymakers can face legal pressure for their decisions, markets must include “governance risk” directly in discount rates. In that context, periods of strength in some traditional haven currencies are not just about better fundamentals; they increasingly look like defensive positioning as uncertainty around the US system rises.

At the same time, tariff actions linked to the Greenland dispute underline that trade policy is shifting from an economic tool to a geopolitical one. When tariffs can quickly move from rivals to allies, and when the trigger is less about industrial goals or the trade balance and more about political issues, then corporate profits, supply-chain costs, and cross-border capital flows become harder to forecast. For institutions, the implication is straightforward: almost anything can be turned into a policy tool. Tariffs can reshape cost structures; the dollar can be used as a tool of financial pressure; and equity markets can be treated as a scoreboard for political success. Macro data still matters, but in this environment, it has less influence on risk appetite and policy expectations.

For years, global allocation rested on an assumption of US institutional stability and policy continuity. Even when tensions rose, markets tended to assume things would return to a familiar track. But when governance conflict shifts from rhetoric to action—investigations, sanctions, and tariffs—this assumption becomes harder to hold. Risk premia then rise across a wider set of assets.

From an asset-pricing perspective, investors are adding a larger “governance uncertainty” component to standard models. That leads to a market that can look contradictory, but, from an institutional point of view, is rational: indices may not fall immediately because earnings momentum and buybacks still support prices, but new money becomes less willing to buy at old valuations. Allocation behaviour shifts towards lower leverage, lower exposure, and lower correlation.

Importantly, this adjustment does not require a crash. For most institutional portfolios, risk management is gradual rather than all-or-nothing. A slow reduction in USD exposure is often expressed through less reinvestment rather than outright selling: new allocations are reduced, maturing positions are not rolled in full, hedge ratios rise, and part of the risk budget moves towards non-USD settlement channels or markets less tied to US policy. The result is that the dollar system’s marginal funding conditions can become more fragile in sentiment terms and more prone to sudden “liquidity discounts” during event shocks.

More Rallies, Less Follow-Through

In this macro regime, crypto markets look less like independent safe havens and more like a function of liquidity and risk appetite. This week’s price recovery is not unusual; in fact, when uncertainty rises, short-lived rebounds often become more common. Short covering, a quick normalisation in futures basis, and short-term changes in stablecoin supply can all create upside. Yet institutional traders’ expectations have not meaningfully improved after this week’s rise. The basic reason is clear: when uncertainty around US fiscal and monetary policy increases, crypto struggles to attract steady, reliable liquidity.

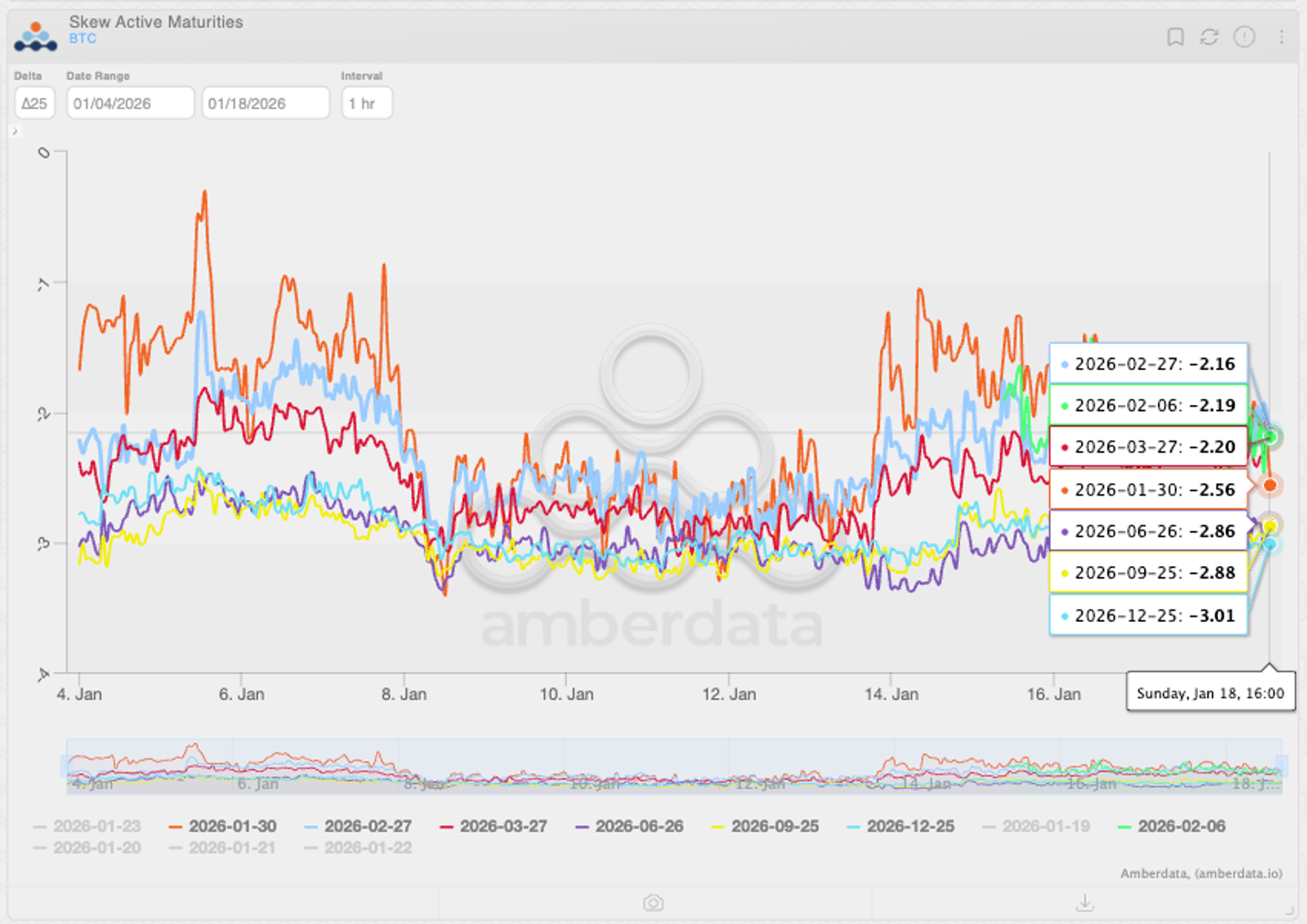

Source: Amberdata Derivatives

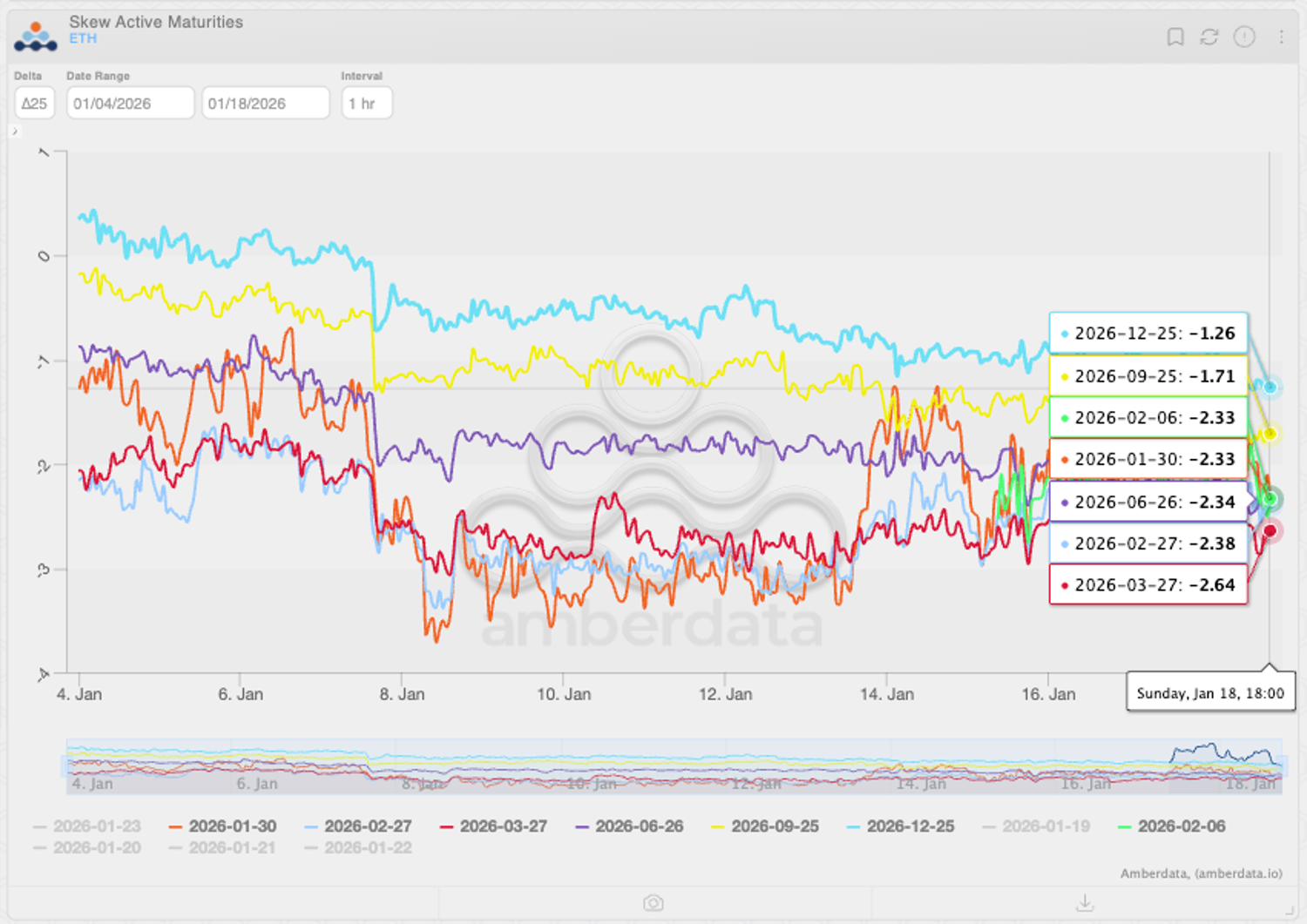

Source: Amberdata Derivatives

This is easy to misunderstand. Intuitively, greater uncertainty about institutions should support “non-sovereign” assets. But market structure keeps crypto closely tied to the dollar system. Leverage, settlement, and key risk tools—especially derivatives and stablecoins—remain heavily USD-linked. When dollar funding becomes harder to read, and when shocks are driven more by politics than by data, market-makers and institutions become more cautious with risk. Leverage shrinks faster, and liquidity becomes shorter-term, thinner, and more expensive. Crypto prices can still rise, but it becomes harder for rallies to turn into trends, because trends need stable, sustained, and affordable new buying.

There is another practical constraint. When macro noise rises, correlations across risk assets often increase in the short run. Crypto, as a higher-volatility instrument, is more likely to be used to adjust overall risk—meaning it may be reduced or hedged earlier than other exposures. The pattern is familiar: rallies are driven by technical factors and short-term flows, while drawdowns are driven by tighter risk budgets and hedging-related rebalancing. For systematic and institutional capital, this is not necessarily a long-term rejection of crypto; it is a recognition that, when USD uncertainty rises, it is difficult to justify a higher “liquidity premium” for crypto.

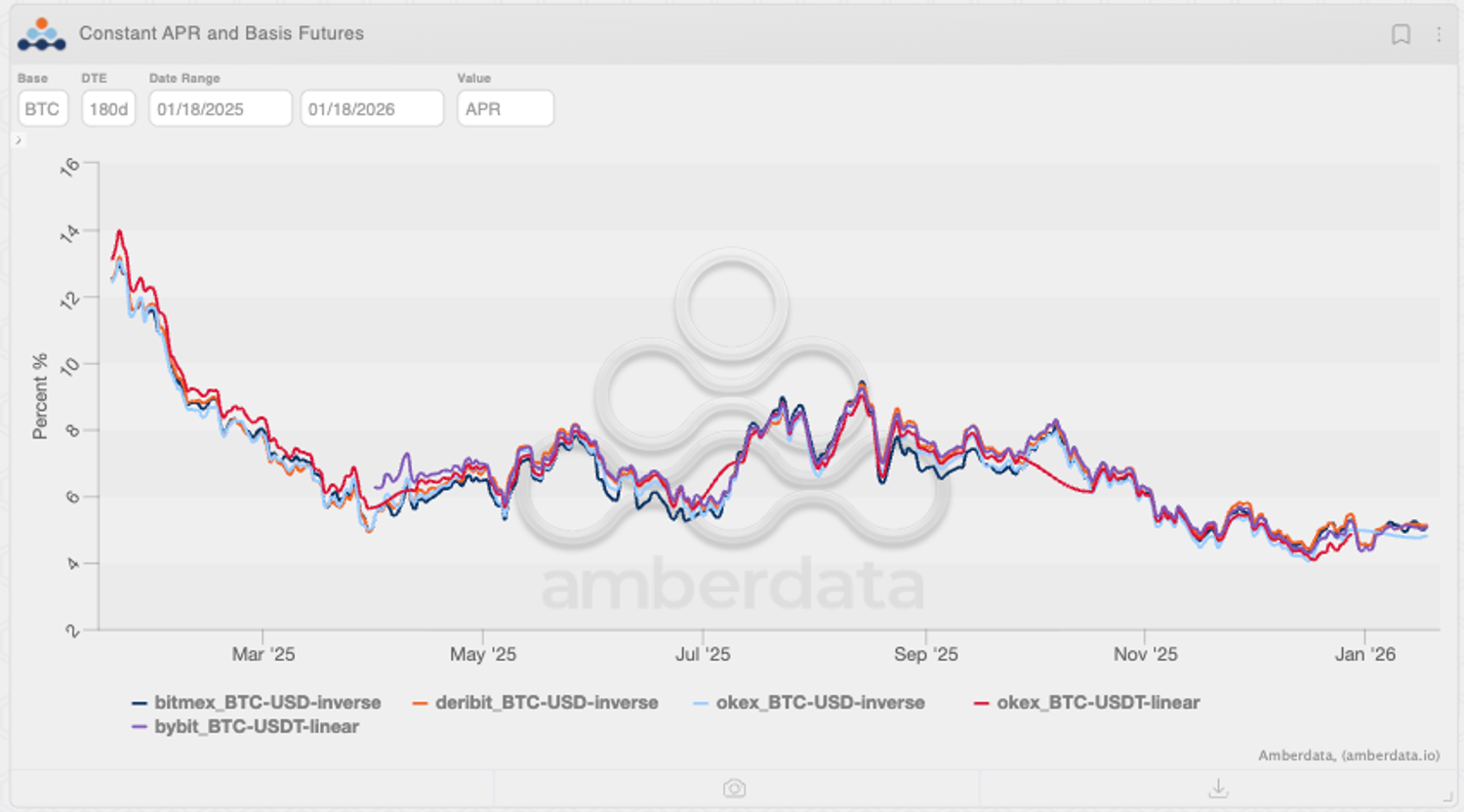

Source: Amberdata Derivatives

A more profound change is that inflation and employment—once central to the market’s policy framework—are being pushed aside by political priorities. Markets used to link expectations closely to data, creating a relatively stable reaction function: higher inflation lifted rate expectations; weaker employment increased the chance of easing; and asset prices moved around that logic. But when political issues can directly drive tariffs, investigations, sanctions, or regulatory direction, the reaction function becomes less consistent. The informational value of data falls, and event risk becomes the main driver. Investors are therefore spending more time assessing whether policy paths are workable and where institutional limits really are, rather than simply trading the next data release.

This also weakens a stabiliser that markets once relied on. The “central-bank put” is the idea that, in severe stress, monetary authorities will step in to prevent financial conditions from tightening too sharply. But when central bank independence is challenged, and central bankers are drawn into political conflict, the credibility of that backstop is reduced. Institutions respond in predictable ways: heavier hedging, shorter duration, lower concentration in one currency system, and stronger diversification across assets, regions, and legal frameworks.

To be clear, institutions have not responded to recent US policy and institutional shocks with panic selling. But they are reducing reliance on USD-linked exposure in a slower, more systematic way—one that is harder to see in headline moves. For USD assets, this means valuations depend more on changes in governance-related risk premia, and risk budgets are more easily triggered by events. For crypto, it means short-term rebounds may happen more often, but sustained trend rallies are harder to maintain without a stable liquidity backdrop. Politics is shifting markets from a data-driven to an event-driven regime. The institutional response is rarely about betting on a single outcome; it is about updating constraints in advance: reducing single-system exposure, keeping liquidity, strengthening hedges, and waiting for a new pricing anchor to emerge.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.