Doves Debating, Hawks Gathering

The Federal Reserve yesterday released the outcome of its final FOMC meeting of the year. Although it delivered a third consecutive rate cut, officials now appear more concerned about inflation and the labour market than about supporting growth. Vast divisions have opened up within the Fed, and officials are signalling limited appetite for further cuts.

Public remarks from Fed officials in recent weeks suggest the committee is deeply split, to the point where the final decision may largely depend on how Chair Jerome Powell chooses to steer policy. Powell’s term is due to expire in May next year, which means he will chair only three more FOMC meetings. Stubborn price pressures, combined with a cooling labour market, have presented the Fed with a trade‑off it has not faced for decades. In the “stagflation” era of the 1970s, when policymakers confronted similar dilemmas, the Fed’s stop–go approach allowed high inflation to become entrenched.

Against this backdrop, several recent Fed actions are worth watching. One is the removal of the aggregate cap on the Standing Repo Facility (SRF). Another is the purchase of short‑term Treasury bills (T‑bills) and, where necessary, other US Treasuries with a remaining maturity of up to three years, to maintain ample reserves in the banking system. The intention is clear: not to provide high‑quality liquidity to equity or crypto markets, but to stabilise short‑term liquidity in the banking system and ease the shortage of short‑dated dollar funding.

The planned purchase of around $40bn of T‑bills this month, together with the loosening of the SRF, will help underpin equity markets, but is unlikely to fuel another leg higher in stocks as in 2021. Powell has also stressed that current T‑bill purchases are purely for “reserve management”, meaning the primary aim of balance‑sheet expansion is to keep liquidity stable rather than to inject additional liquidity to stimulate the economy and markets.

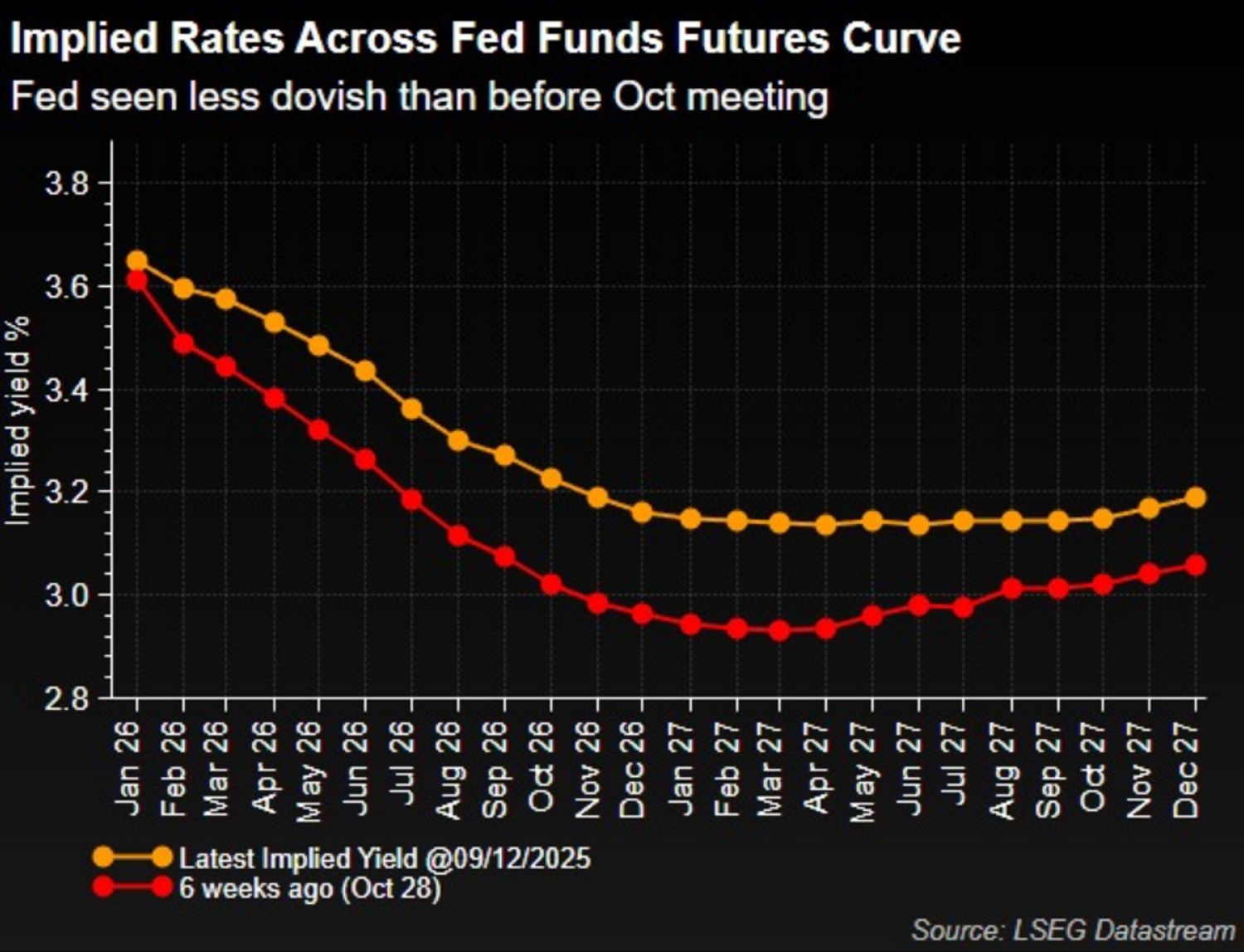

Judging from implied rates in interest rate derivatives, the Fed is clearly less dovish now than it was at the end of October.

What may prove more consequential are the signals and actions coming from non‑US central banks. A growing hawkish tilt among major central banks has become a key focus for markets. Recent comments from Reserve Bank of Australia Governor Michele Bullock and ECB Executive Board member Isabel Schnabel both suggest that their next move could be a rate hike. The Bank of Canada, for its part, indicated in this week’s policy decision that “the easing cycle may have ended”, a message that significantly exceeded market expectations. The Bank of Japan is also widely expected to raise rates next week and to hike a further three times next year, taking the terminal rate to around 1.5%.

Many major central banks now find themselves in an unusual position: they have just completed their fastest easing cycle in decades, despite the absence of a formal recession. Analysts at Deutsche Bank note that, in the Fed’s case, this is the first time since the mid‑1980s that such rapid easing has occurred without an accompanying downturn, while the ECB has never before loosened policy this aggressively without an economic contraction.

Historically, rapid easing that is not triggered by recession has often been followed by a marked re‑acceleration in economic activity – particularly when rate cuts are combined with generous fiscal spending. That, in turn, paves the way for a return to rate hikes sooner than markets had anticipated. This is one plausible scenario for next year. Although the Fed may, under pressure from a Trump administration and out of concern for the labour market, maintain a more dovish tone for a while longer, the current level of the federal funds rate suggests the next potential “terminal rate” may not be far away.

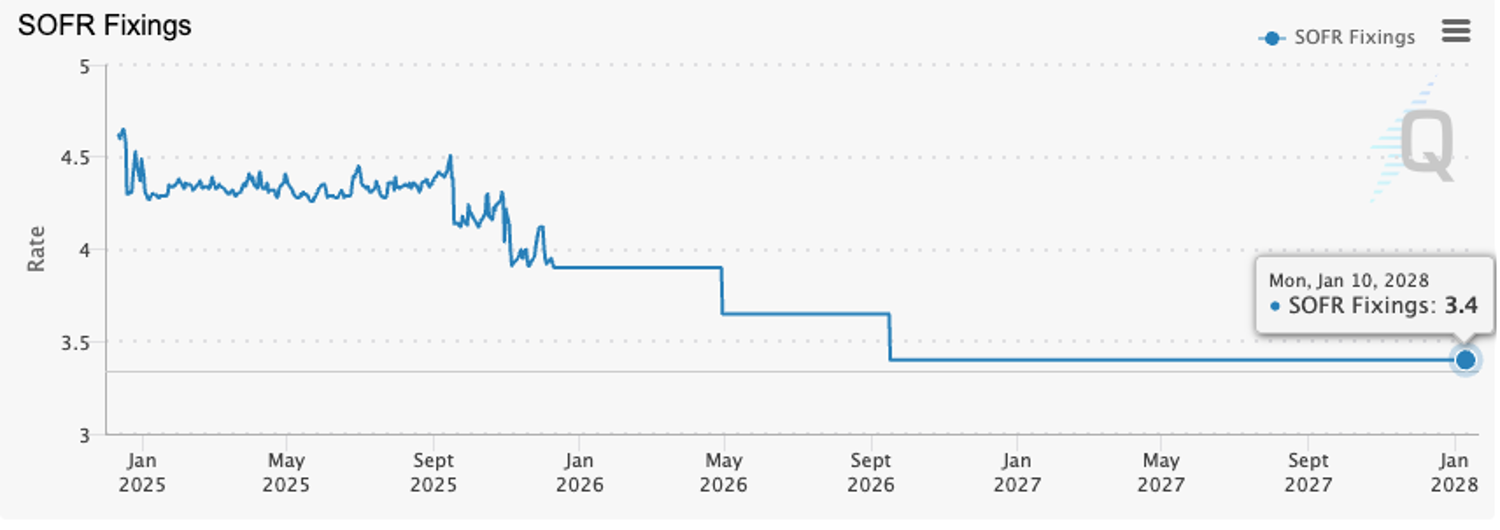

The SOFR futures implied terminal rate has risen to 3.4%, a significant increase from the previously expected terminal rate of 3%. Source: CME Group

The Long Goodbye of Easy Money

Market pricing of G10 central bank policy shows that only three – the Federal Reserve, the Bank of England and Norges Bank – are expected to cut rates next year. The Fed is priced to deliver cuts of 50–75bps, while the other two are expected to cut by around 50bps each.

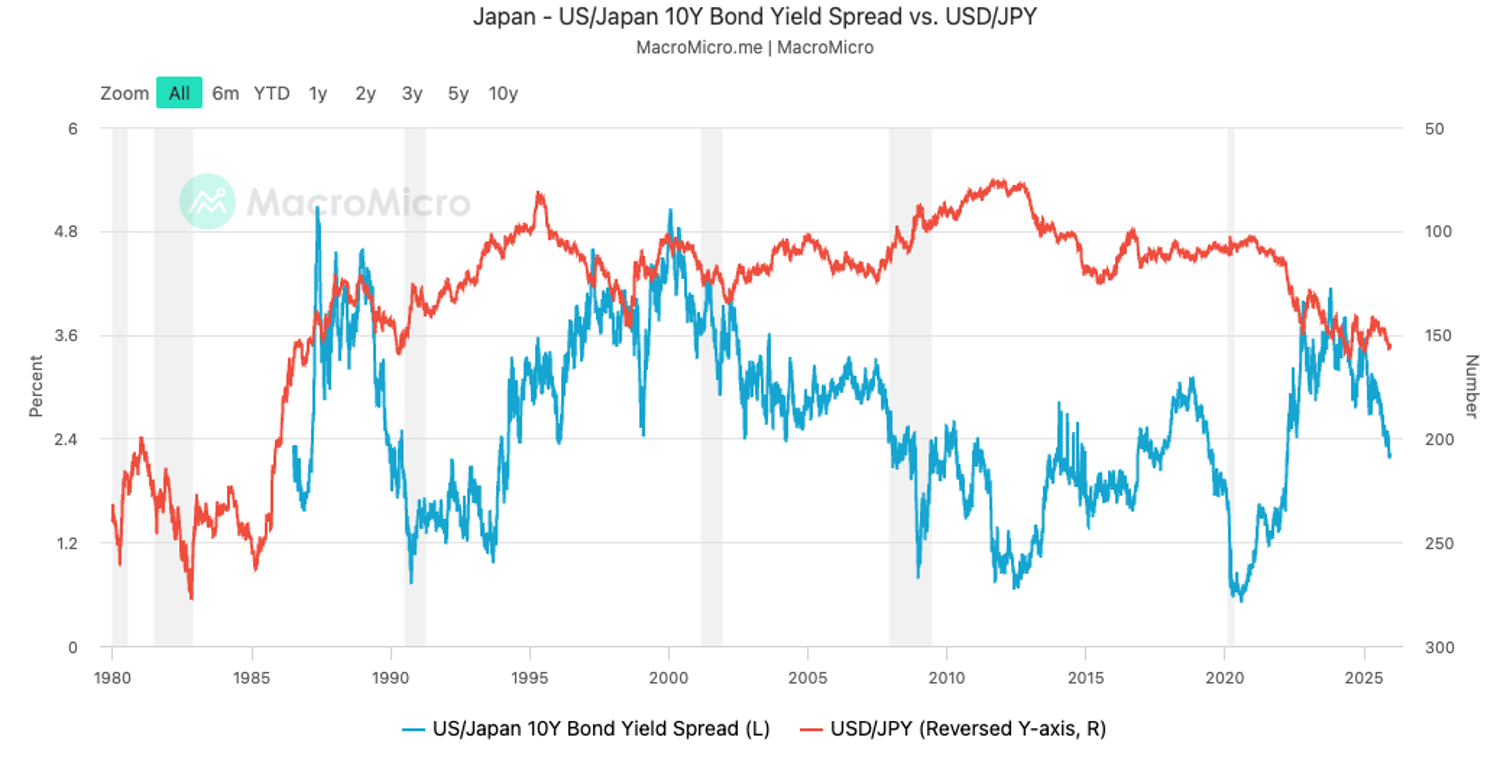

By contrast, interest rate derivatives now price in further hikes by the Bank of Canada and the Reserve Bank of Australia, of roughly 35bps and 50bps respectively next year. Only a few weeks ago, markets still viewed rate cuts in these two economies as more likely than hikes. Meanwhile, the yield on 10‑year Japanese government bonds (JGBs) has climbed above 1.9%, the highest level since 2008, indicating that offshore market liquidity is already starting to tighten.

Source: Tradingview

What unsettles some investors is that this offshore liquidity squeeze may well accelerate. Typically, a narrowing of the yield spread between US and Japanese 10‑year government bonds would push the yen higher. This time, even though the spread has narrowed to levels last seen around 1990 and 2008, the yen has not strengthened meaningfully. At the same time, Prime Minister Sanae Takaichi unveiled an economic package last month, which included additional spending exceeding economists’ forecasts. Former BoJ chief economist Hideo Hayakawa has argued that Takaichi is creating a large fiscal deficit in an attempt to stimulate an economy that is not genuinely short of demand, and that the fiscal measures ostensibly designed to “offset the impact of inflation” are in fact likely to add further upward pressure on prices.

Against this backdrop, the BoJ may have little choice but to move from a largely passive stance to a more proactive one – accelerating the pace of rate hikes while working with the Ministry of Finance to intervene in the foreign exchange market via open‑market operations, to stabilise the yen. Such a course of action would likely drain even more of the already scarce pool of high‑quality dollar liquidity from global markets. In that scenario, from crypto assets to bond markets could come under significant pressure.

Source: MacroMicro

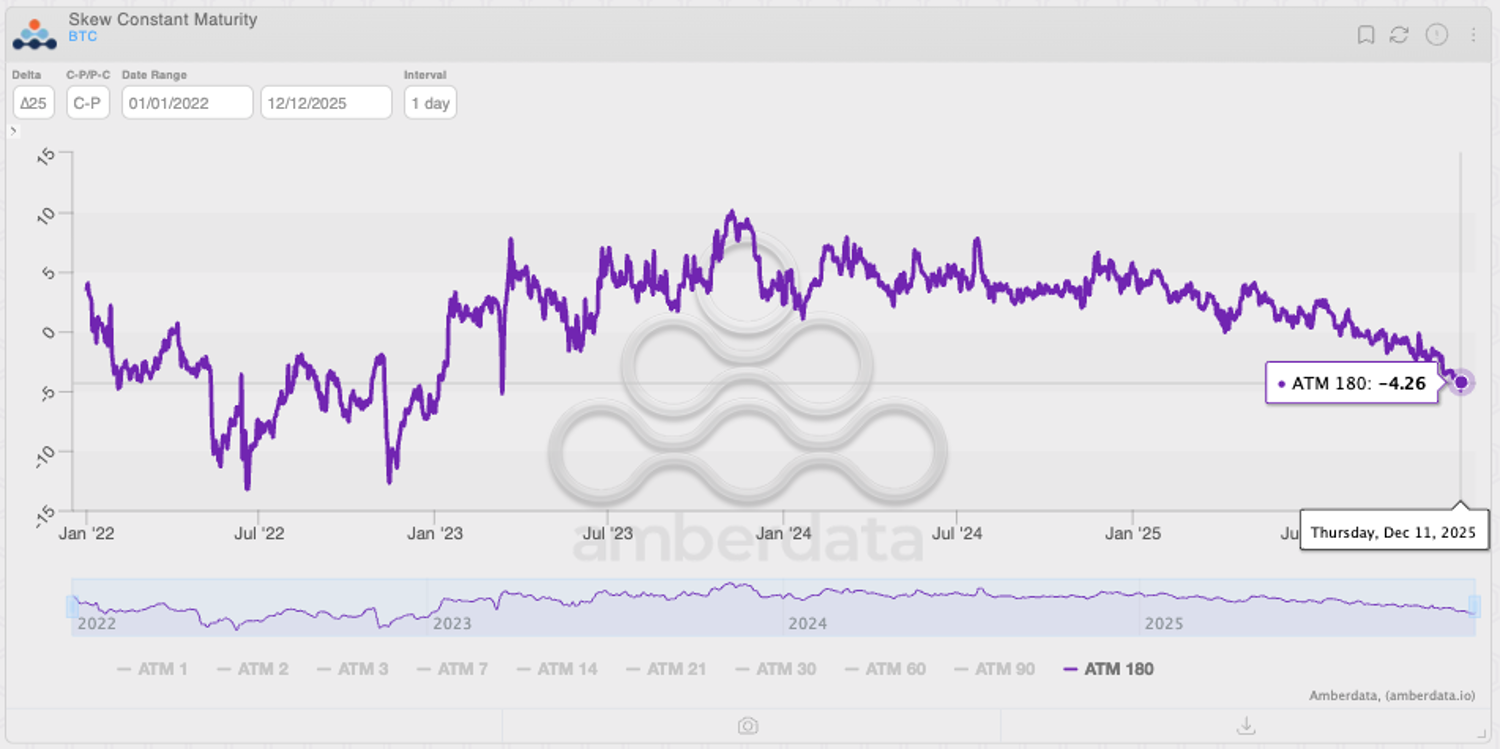

As one of the asset classes most sensitive to liquidity conditions, the crypto market has already begun to reprice the outlook. In the crypto options market, traders’ long‑term bearish stance on BTC and ETH has not moderated; if anything, it has deepened. Bullish sentiment is largely confined to ultra‑short‑dated 0DTE options and short‑term speculation. Notably, the persistent bullish bias in far-month ETH options has all but disappeared, with expectations shifting into a “neutral‑to‑bearish” range, while the degree of long‑term bearishness on BTC has already returned to levels last seen in the second half of 2022 – a period marked by a sharp contraction in liquidity.

Source: Amberdata Derivatives

As traders reassess the global monetary policy outlook, bond markets may prove particularly vulnerable, especially given that volatility in these markets is already hovering near historical lows. The MOVE index, which tracks implied volatility in the US Treasury market, has fallen below 70. Only in a handful of periods – such as 2006–07 and 2017–19 – has the MOVE index been at similar levels. Those episodes tended to mark the end of one cycle and the threshold of the next.

At present, currency and bond markets display an apparent paradox:

- Investors are increasingly uneasy,

- Yet volatility remains low.

Historically, such a configuration has not typically persisted for long. As the new year approaches, this uneasy equilibrium may be put to the test.

Source: Tradingview

Over the past decade or so, investors have grown used to a world in which “liquidity eventually comes back”: every spike in volatility has, sooner or later, been met with larger waves of monetary easing and more abundant dollar liquidity. The current macro environment is quietly eroding that habit. With inflation still sticky, fiscal expansion increasingly rigid, and demographics and geopolitics being reshaped in parallel, central banks are being forced into harsher trade‑offs between growth and inflation. This implies that monetary easing is no longer a safety valve that can be relied upon indefinitely, and liquidity is no longer a free public good.

For investors, the key challenge is no longer to guess whether the next move is a hike or a cut, but to rebuild a risk framework suited to an era of “chronic tightening”: how to identify the weak spots in highly leveraged and long‑duration assets beneath a veneer of low volatility; how to distinguish between forced selling and genuine fundamental deterioration during structural liquidity withdrawal; and how to locate new anchors of equilibrium between exchange rates, interest rates and asset prices.

The most important opportunities in this new cycle may emerge precisely from this sense of discomfort. Those who most quickly accept the reality that liquidity is no longer unconditionally on their side are likely to be better placed in the next round of asset repricing.

Want to know how to trade for the scenario above? Please see this article: Whale's Tradingview: Why the Fed's 'Gift' Won't Fuel a Crypto Santa Rally

Economic Calendar of This Week

Tuesday 03:30

- AU RBA Interest Rate Decision

Tuesday 15:00

- US JOLTs Job Openings (Sep)

- US JOLTs Job Openings (Oct)

Wednesday 14:45

- CA BoC Interest Rate Decision

Wednesday 19:00

- US Fed Interest Rate Decision

- US FOMC Economic Projections

- US Fed Press Conference

Friday 07:00

- UK GDP MoM

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.