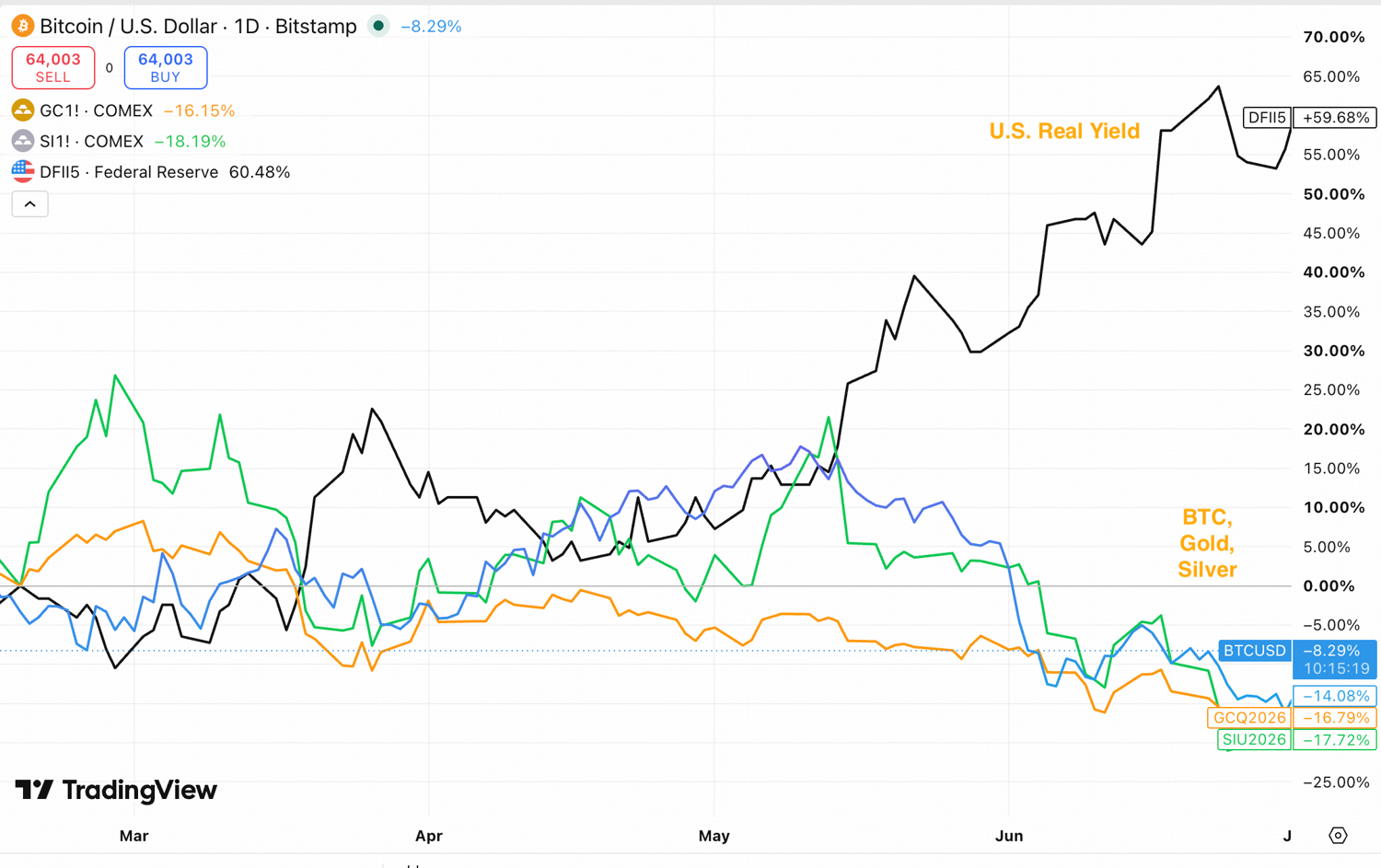

Bitcoin, gold, and silver have different long-run fundamentals. Over the past two months, however, they have traded off the same short-run macro impulse: inflation expectations, the Fed reaction function, and real yields.

As the 5-year TIPS yield rose from 1.33% on May 1 to roughly 2.0% by early July, higher real yields raised the opportunity cost of holding non-yielding stores of value and pressured the broader scarcity trade.

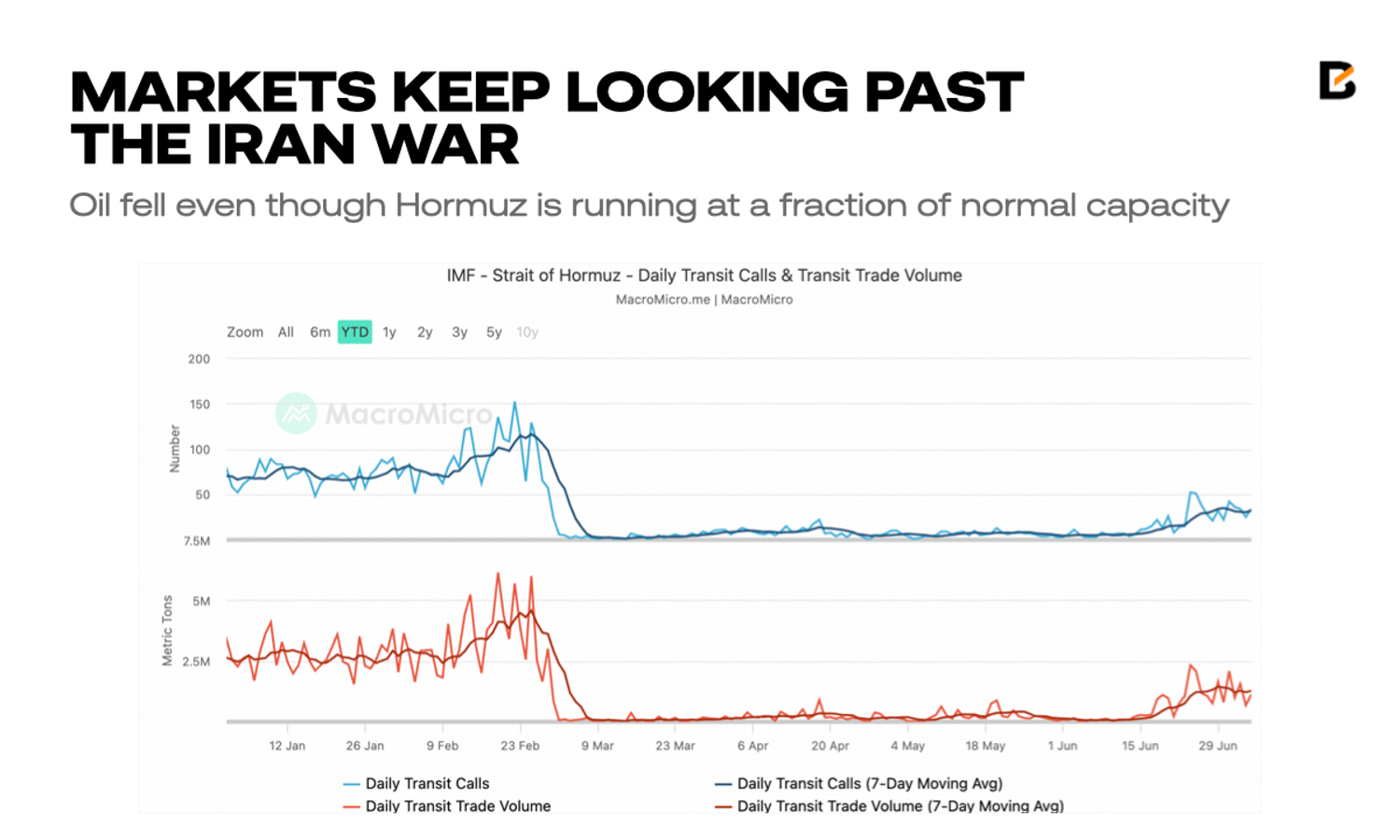

Markets Are Now Looking Past Energy Shock

The closure of the Strait of Hormuz drove the inflation spike that defined the first half of 2026. Brent traded above $120 at its spring peak, and energy accounted for over 60% of May's monthly CPI gain.

The spike in inflation pushed the Fed to hold policy restrictive and lift its rate path. Inflation-adjusted Treasury yield, real yield, rose with it. For an investor, a rising real yield lifts what a safe, inflation-protected Treasury pays in real terms and raises the hurdle for holding an asset that yields nothing

Oil has since come down. Front-month WTI fell about 20% in June as traders leaned toward the view that broader escalation can be contained. But the Strait has not reopened in any meaningful way, and the energy-risk premium is unresolved. The key question is whether the decline in crude reflects a genuine improvement in supply conditions or merely a temporary reduction in tail-risk pricing.

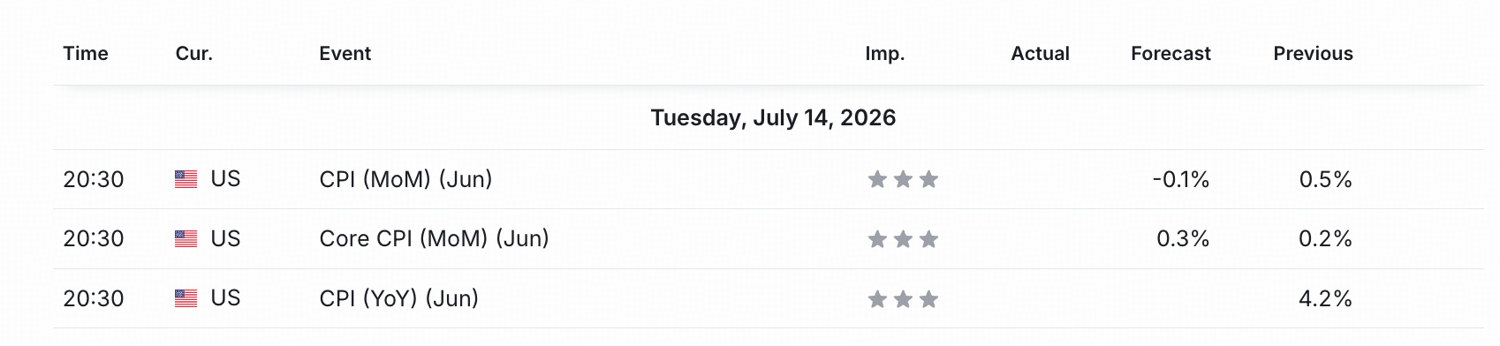

June CPI Likely to Show Cooling

June CPI is due Tuesday, July 14, the final CPI print before the July 28–29 FOMC meeting, and it tests whether the energy-driven spike has rolled over or leaked into core.

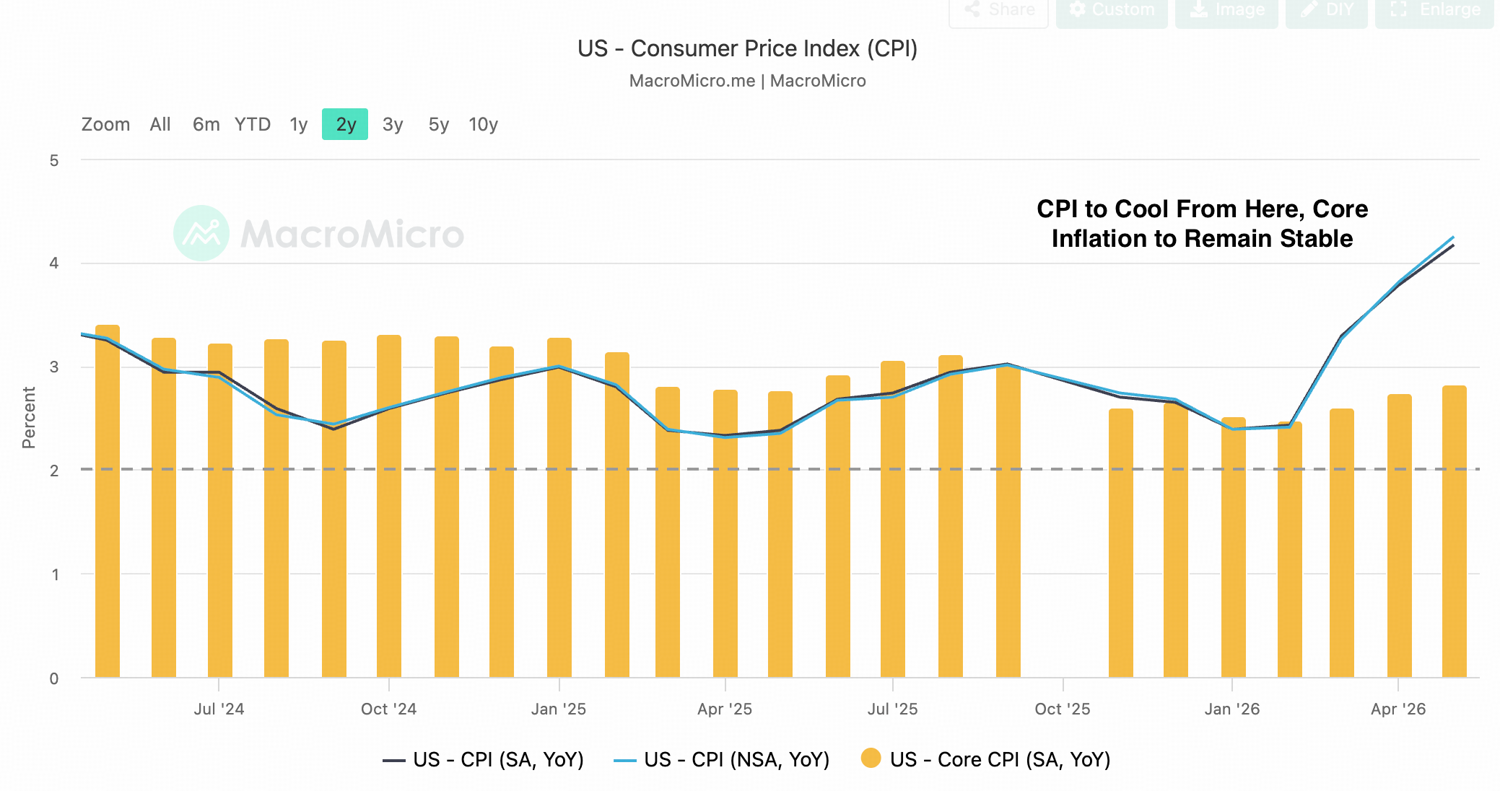

Consensus looks for headline CPI to fall 0.1% month over month, taking the annual rate to roughly 3.9%, while core CPI is expected to rise 0.3% and hold near 2.9%. That would mark a sharp reversal from May, when CPI rose 0.5% on the month and 4.2% from a year earlier, with energy accounting for more than 60% of the monthly increase.

Our view is that the inflationary impulse from the energy shock has probably peaked. Gasoline and crude price pressure moved from a CPI driver to a June drag, and base effects become more favorable from here. Fed staff made a similar distinction in the June minutes, projecting total inflation to slow in the second half as retail gasoline prices decline, while core inflation changes little over the rest of the year.

The Strait premium remains the tail risk. Flows through Hormuz have improved unevenly, security risks remain elevated, and the reopening process still faces technical, commercial, and geopolitical constraints. That keeps renewed energy pressure on the risk map.

Inflation Is Backward-Looking; Warsh Is Forward-Looking

The June CPI report tells us where inflation has been. Fed Chair Kevin Warsh's testimony will offer a clearer signal on where he believes it is heading. With the Fed placing less emphasis on explicit forward guidance, policymakers' public remarks have become a key window into their evolving reaction function.

The key uncertainty is AI. In the near term, AI looks inflationary. Demand for GPUs, memory chips, data centers, electricity, and transmission infrastructure is driving a new investment cycle, while some of those costs are already being passed on to consumers. New versions of electronic products, like smartphones, are priced above their predecessors, and rising electricity demand is contributing to higher utility bills. Rather than lowering prices immediately, AI is first creating a new wave of capital spending that supports inflation.

Over a longer horizon, however, AI could prove disinflationary. If the technology delivers meaningful productivity gains, higher output per worker would ease unit labor costs and expand supply capacity, reducing inflationary pressure across the broader economy. Warsh has acknowledged both possibilities. At the ECB's Sintra Forum, he expressed optimism about AI's productivity potential while cautioning that the evidence has not yet appeared in the inflation data.

Our base case is that the inflation impulse from the energy shock is largely behind us. The more important policy question is whether AI-driven investment creates a new source of persistent inflation before productivity gains materialize. That uncertainty is likely to keep the Fed cautious, supporting a higher-for-longer policy stance and elevated real yields even as energy-driven inflation continues to recede.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.