Examining the Fed's Internal Divisions

The Fed's schism stems fundamentally from differing interpretations of economic metrics: inflation paths, labour market indicators, policy trajectories, and approaches to data gaps. With core PCE inflation hovering around 3%—exceeding the 2% target—hawks perceive it as a latent rebound risk, amplified by escalating trade tariff uncertainties; doves maintain that inflation has moderated sufficiently to warrant additional easing. Both sides recognise the employment slowdown (September yielded only 119,000 jobs, below expectations).

Yet, hawks deem it insufficient to warrant immediate intervention, whereas doves fear it could cascade into broader economic fragility. On the policy front, hawks advocate a pause or measured adjustments from the prevailing 3.75%-4.00% federal funds range; doves press for a December cut, possibly extending to 50 bps. The data blackout heightens frictions: doves contend that available evidence is adequate for action, while hawks emphasise prudence to mitigate blind spots.

Statements from prominent figures in November delineate the split. Dovish advocates include Fed Governor Christopher Waller, who stresses labour market vulnerabilities, arguing that existing data justifies further cuts and downplays the blackout's impact—his November 25 remarks elevated the December cut probabilities to 65%-80%. New York Fed President John Williams supports easing, viewing labour cooling as a vital warning; his late-November comments boosted market odds to 69%. Fed Governor Stephen Miran calls for decisive action, advocating at least 50 basis points to forestall recession, observing in his 25 November statement that inflation remains persistent but employment is weakening more rapidly.

Hawks counter: Kansas City Fed President Jeffrey Schmid regards inflation as excessively high for adjustments, deeming October's cut superfluous; he reaffirmed on November 14 that progress could falter. Dallas Fed's Lorie Logan concurs that the October easing exceeded the requirements, urging caution to avoid over-stimulation—her discussions on 14 and 21 November highlight the constrained leeway for further moves. Cleveland Fed's Beth Hammack prioritises inflation risks, moderating December cut expectations in her comments on November 14. St. Louis Fed's Alberto Musalem urges circumspection with entrenched 3% inflation, prioritising dual-mandate equilibrium; his early and late-November cautions underscore the hazards of excessive easing.

Moderately hawk-leaning centrists include the Chicago Fed's Austan Goolsbee, who perceives inflation pressures as potentially delayed but employment deterioration as accelerating, having transitioned from a dovish stance in early November. Chair Jerome Powell adopts a neutral posture, facilitating potential cuts through allies while remaining data-contingent; his late-November tone, bolstered by individuals like Waller, maintains adaptability.

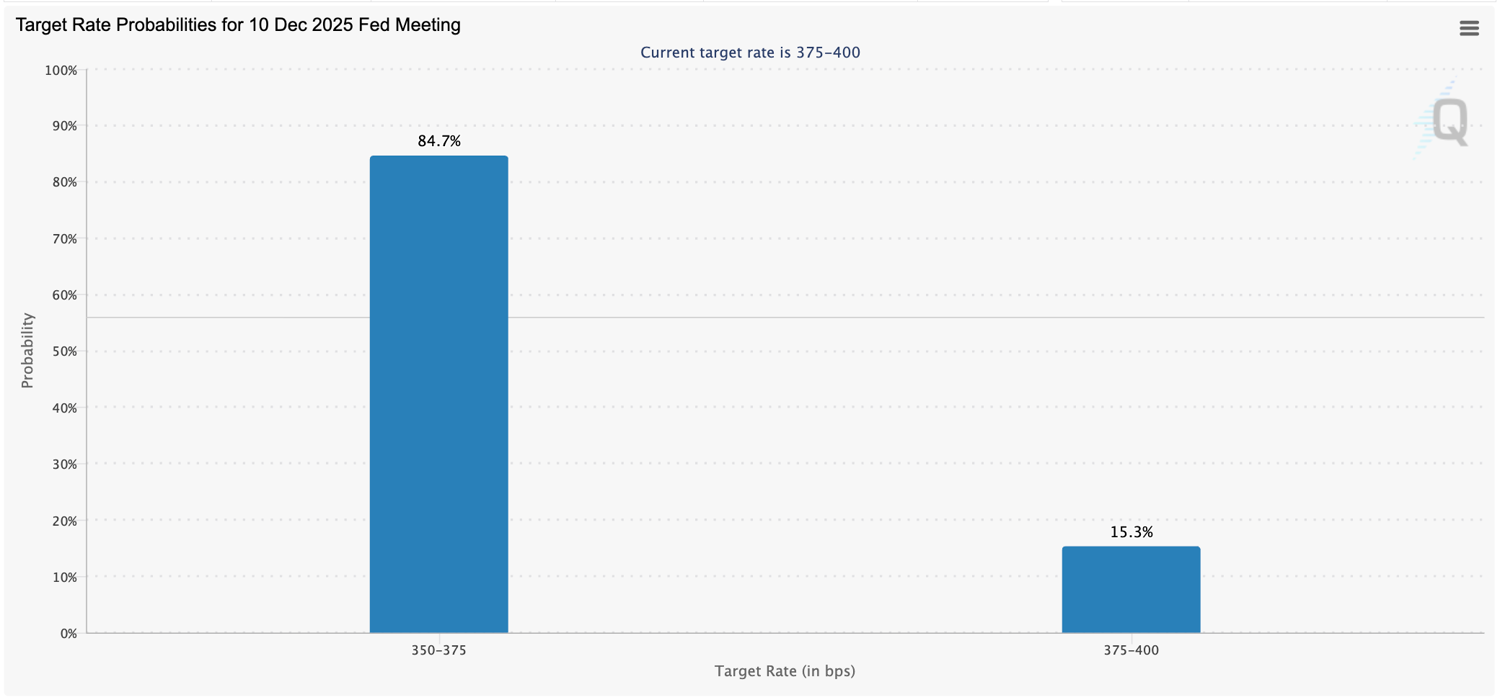

Source: CME Group

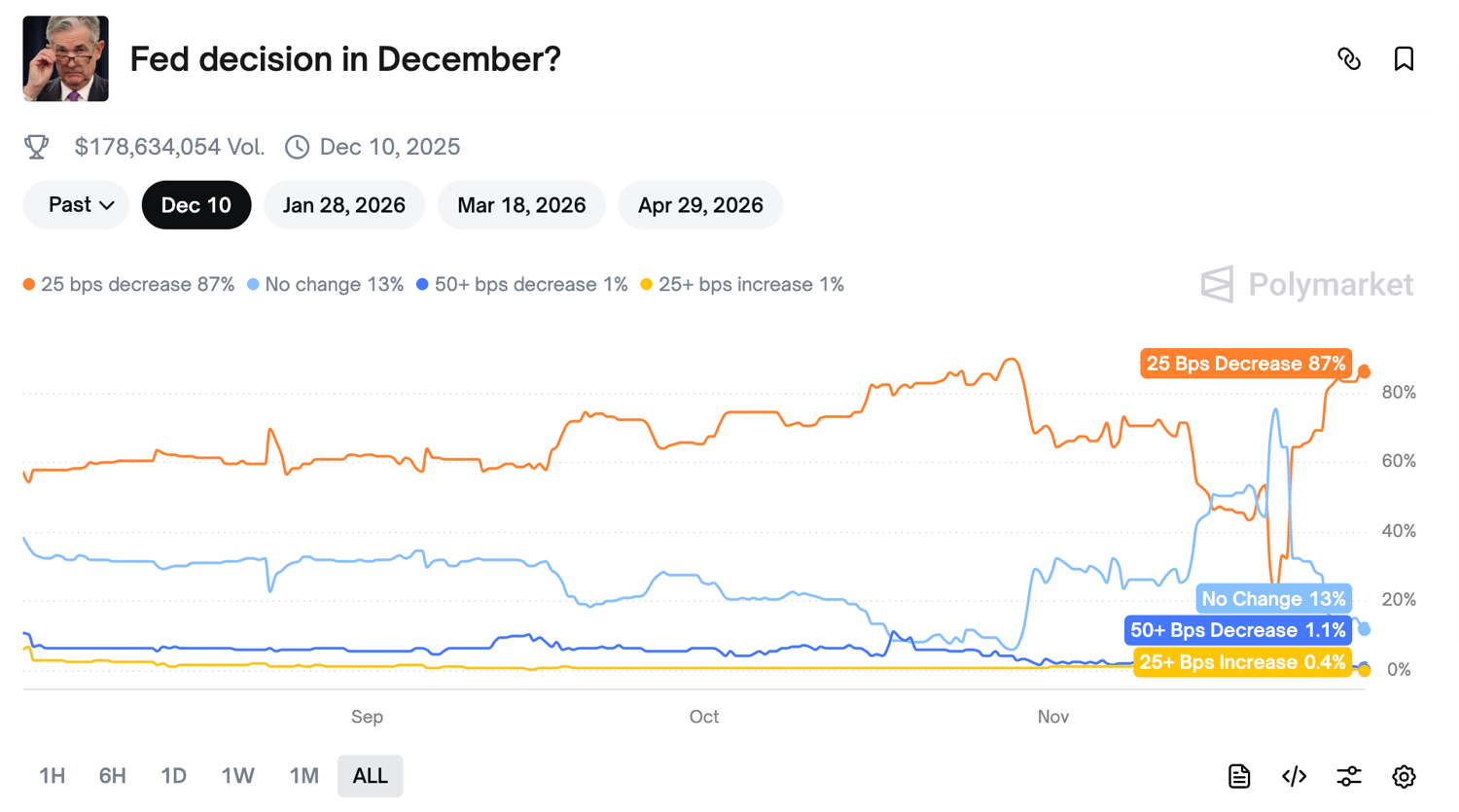

This dissonance is evident in October's FOMC minutes, where officials diverged sharply on sustained cuts—some suggesting a year-end suspension. Markets have fluctuated accordingly: the December cut odds dropped to 40% early in November, rebounding to 80% or higher amid dovish cues. On X, the contention is apparent, with Polymarket odds climbing to 87%.

Source: Polymarket

Outside the Fed, analysts are providing valuable context, highlighting the implications of the rift. Forbes' Simon Moore observes that the October minutes' hawkish inflection depressed cut probabilities, exposing "profound disagreements." Markets.com dissects 2025 FOMC outlooks: doves emphasise employment vulnerabilities, hawks inflation revival. Fortune's Siegel construes Williams' receptiveness as dovish preparation, contrasting hawks' insistence on data inadequacy. Reuters warns that conflicting views are intensifying market wager volatility, positioning December as a "contentious episode." Nuveen's investment perspective interprets Powell's press conference as hawk-leaning, recalibrating cut anticipations. BCA Research posits that the minutes reveal hawk-dove profundity, enhancing pause prospects. FXStreet notes officials' judicious yet fragmented path evaluation.

The prevailing view? Data delays and dual-mandate strains engender decision-making intrigue.

Potential Market Repercussions from the Divisions

The Fed's divisions not only amplify policy ambiguity but could also induce substantial financial market oscillations.

- If doves prevail and a cut materialises, equities stand to gain, particularly in growth and technology segments (Nasdaq has advanced 2.5% on dovish rhetoric), with the S&P 500 potentially advancing 1-2%. Historical easing phases have delivered average equity returns of 10-15% (as seen in 2023-2024). Bond yields would recede, with 10-year Treasuries falling below 4%, which would benefit REITs and ETFs such as TLT and VNQ by approximately 2%. The dollar would depreciate (DXY repelled at 100), bolstering gold (reaching two-week highs, eyeing $4,190-4,245). Cryptocurrencies like Bitcoin might surge. In sum, recession probabilities would diminish, albeit with risks of subsequent adjustments if inflation reaccelerates. JPMorgan has revised its stance to endorse a cut.

- Conversely, a hawk-dominated pause elevates retrenchment hazards. The S&P 500 could retreat to 4,800 (mirroring 20 November's $1 trillion market capitalisation erosion). AI leaders, such as Nvidia, would likely encounter heightened post-earnings volatility. Rising yields would escalate borrowing expenses, constraining REITs and fixed-income instruments. Dollar appreciation would suppress commodities (gold and crypto declining). Hawkish indicators have historically propelled VIX spikes of 20-30%. Wider ramifications: heightened inflation and tariff apprehensions fostering risk aversion, with commodities already subdued by hawkish undertones.

Ambiguity itself magnifies impacts; over the longer horizon, 2026 policy may ease (hawks frequently yield to doves), but near-term fissures could engender "sugar-rush" economic patterns—swift easing succeeded by abrupt corrections. Continued employment erosion (e.g., Verizon's 13,000 redundancies) would fortify dovish positions.

Bottom Line

The Fed's split stems from a data drought and a mandate on a tightrope, with markets pricing in a dovish tilt—but fresh numbers or speeches could flip the script. It is clear that this isn't policy as usual; it's a test of resolve shaping global finance. Traders, keep a close eye on the charts next week and use them to navigate the turbulence. The Fed's moves—or lack thereof—will echo far beyond the Eccles Building.

Economic Calendar of This Week

Tuesday 13:30

- US PPI MoM

- US Retail Sales MoM

Wednesday 12:30

- UK Autumn Budget 2025

Wednesday 13:30

- US Durable Goods Orders MoM

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.