Author: M2M Research

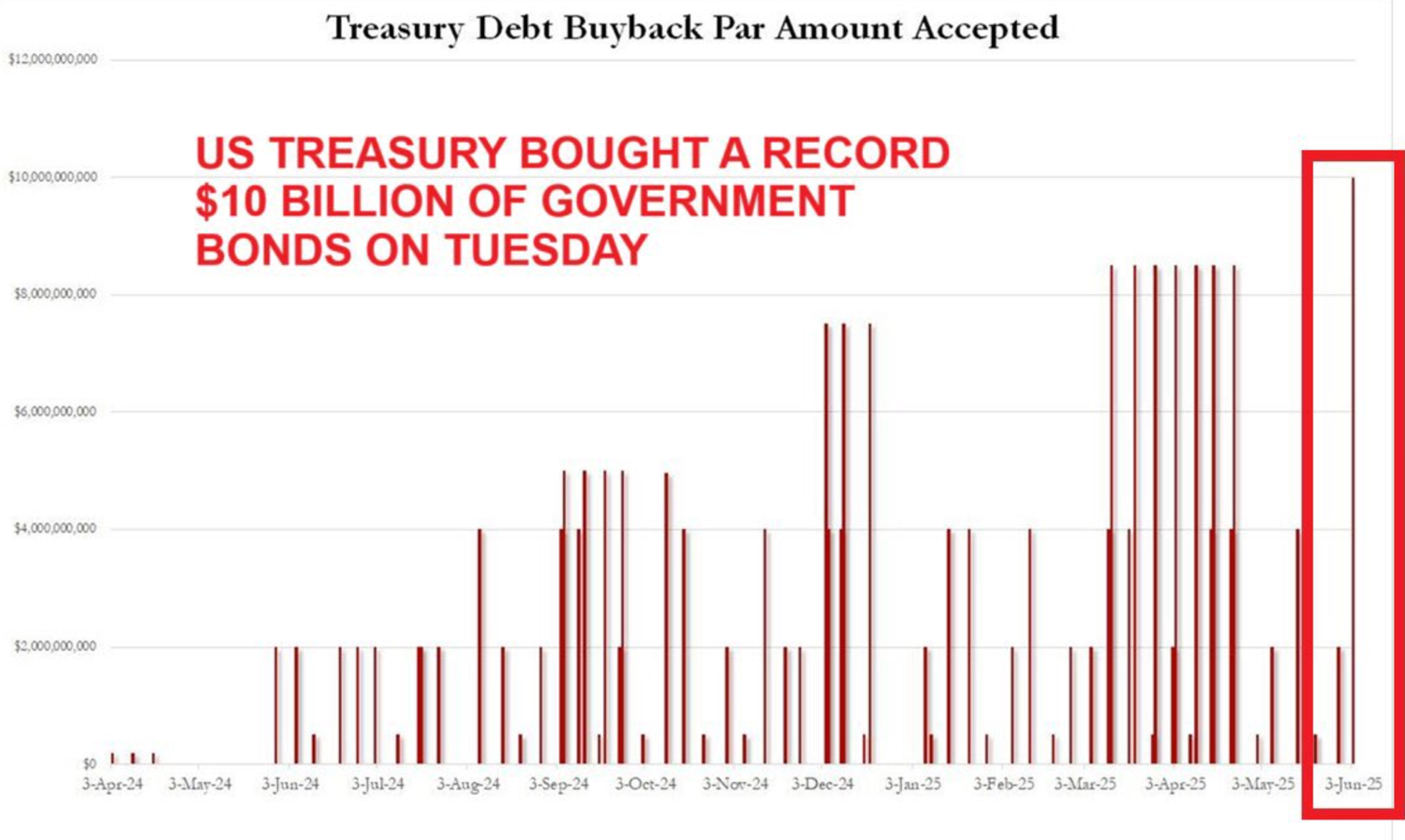

A recent media headline – "Secretary Bessent Intervenes to Support Bond Market with $10 Billion Buyback" – has generated considerable market chatter. The report highlighted the US Treasury's repurchase of $10 billion in government bonds on June 3rd, a record single-day amount. While the figure is notable, the interpretation that this constitutes a market rescue operation is fundamentally incorrect.

Source: ZeroHedge

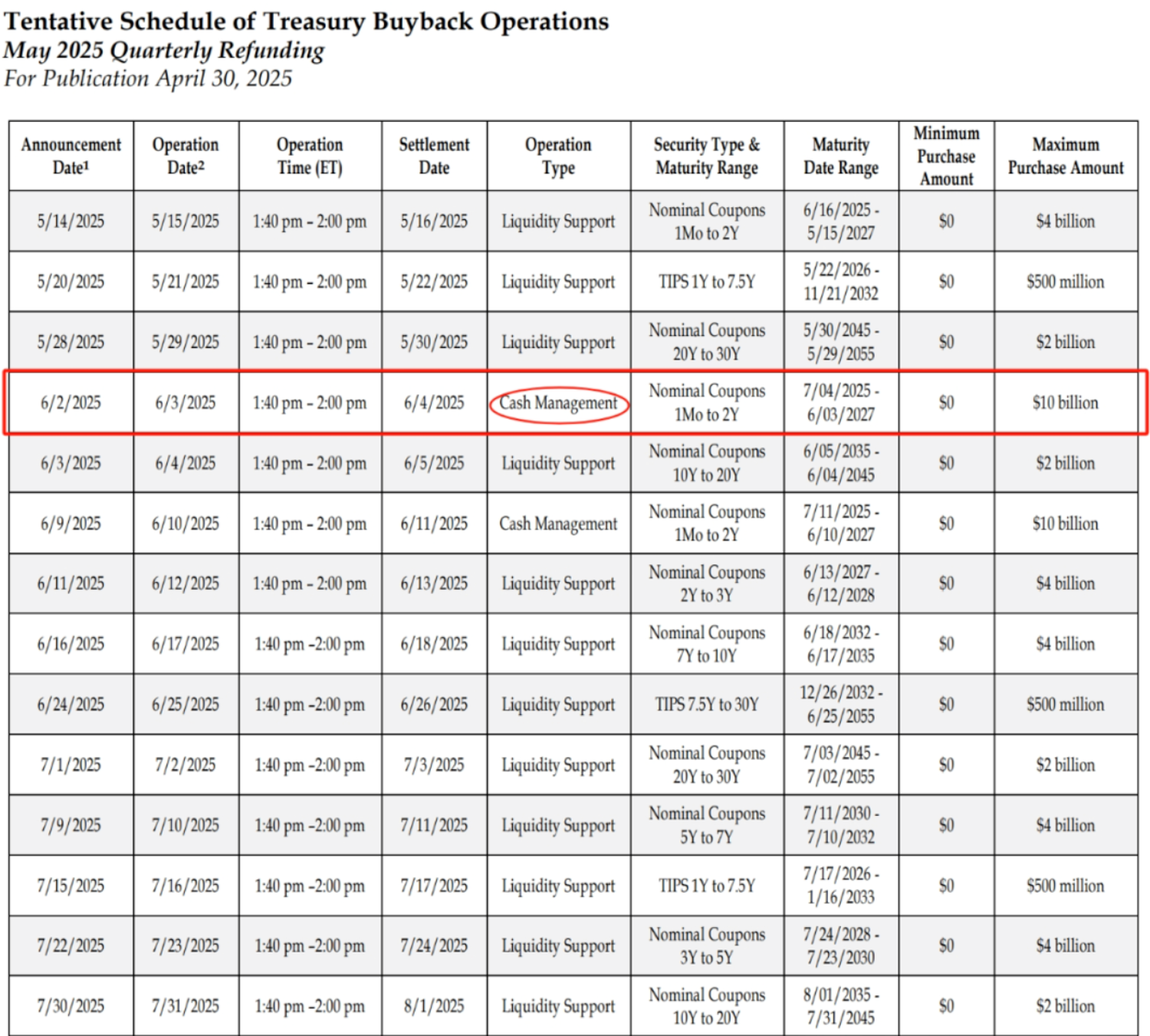

The buyback was not an ad-hoc decision by Treasury Secretary Scott Bessent in response to market pressures. The operation was part of a pre-announced schedule. The Treasury's May quarterly refunding statement had already detailed the buyback plans for the coming quarter, explicitly setting the maximum repurchase amount for June 3rd at $10 billion. Therefore, the notion that the Treasury suddenly scaled up its operations to alleviate current debt market stress is unfounded. The execution of the $10 billion buyback was simply the fulfilment of a previously communicated plan. Moreover, this $10 billion operation was a "cash management buyback," specifically targeting short-dated securities—in this case, T-notes with maturities under two years.

It is crucial to distinguish between the Treasury's two types of buyback facilities. One is Liquidity Support Buybacks. These are regular, predictable operations designed to purchase off-the-run securities to enhance market liquidity. These occur weekly, with maximum limits of $4 billion for nominal coupon debt with maturities under 10 years, $2 billion for debt with maturities over 10 years, and $500 million for TIPS.

The other is Cash Management Buybacks. These operations are designed to smooth the Treasury's volatile cash flows. The Treasury experiences significant cash inflows during tax seasons (mid-April, June, September, and December) and substantial outflows for maturing quarterly refunding bonds (mid-February, May, August, and November). Cash management buybacks help to mitigate this volatility. By repurchasing securities nearing maturity during periods of high tax receipts, the Treasury creates a cash outflow, which smooths its cash balance and reduces the volume of debt maturing at key quarterly intervals. The underlying securities for these operations are exclusively short-term, with maturities ranging from one month to two years.

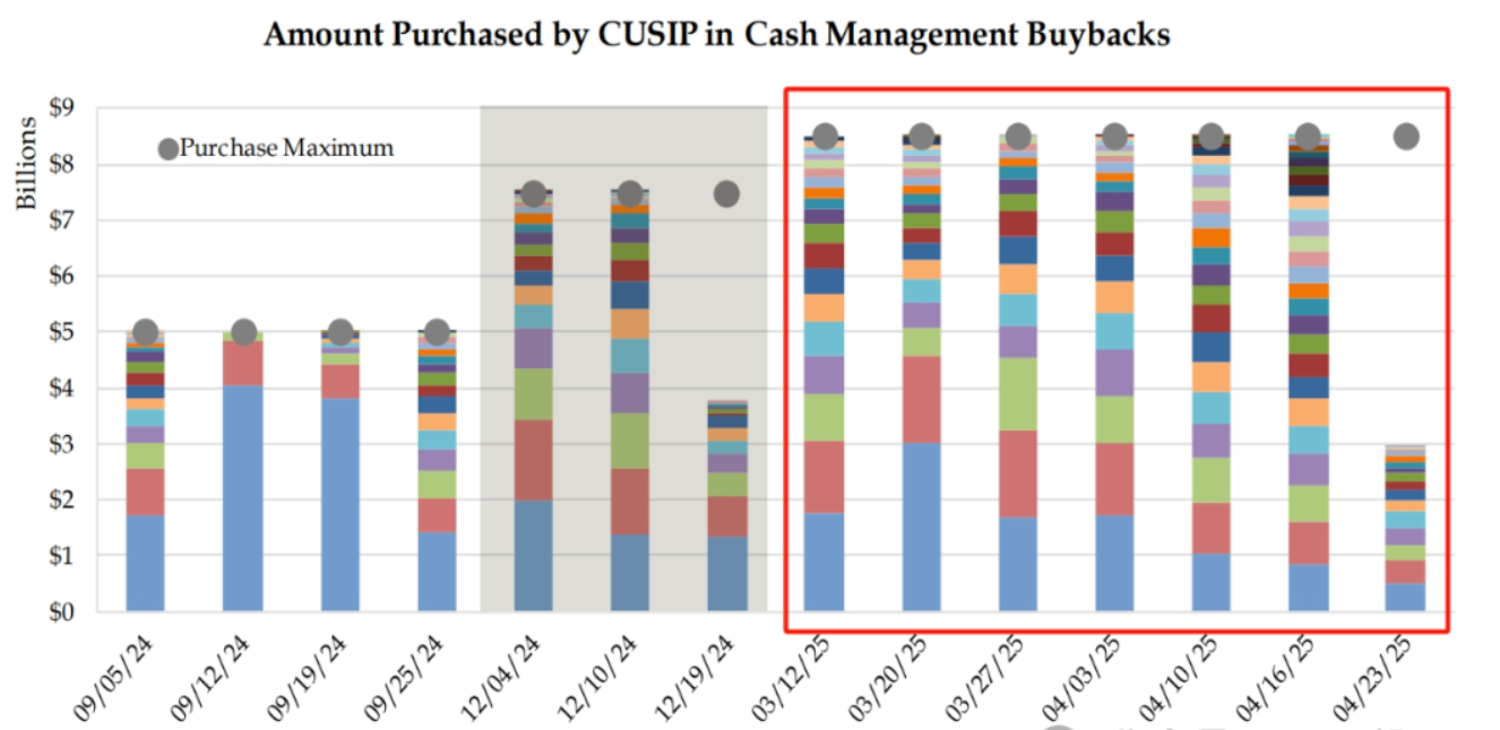

The recent operation was explicitly for cash management purposes. In fact, to manage the April tax inflow period, the Treasury conducted seven such operations between mid-March and late April, with maximum amounts reaching $8.5 billion per operation. The June 3rd buyback was a preparatory measure for the June tax collection period, and another $10 billion operation is scheduled for June 10th.

Finally, the Treasury Borrowing Advisory Committee (TBAC) has advised against using buybacks as a tool for actively managing the Weighted Average Maturity (WAM) of the government's debt portfolio. In its May 2025 report to the Secretary of the Treasury, the TBAC stated, "The Committee believes there is scope to continue to evolve the [buyback] program, in line with these stated goals [of liquidity support and cash management]. However, the Committee felt it important that broader metrics such as WAM still be managed through Treasury's issuance decisions."

It is also crucial to remember that Treasury buybacks are not equivalent to the Fed's quantitative easing (QE). The Treasury does not create new money; it must finance these repurchases. If the Treasury were to fund the buyback of long-term bonds by issuing more short-term bills, it would indeed be a form of active WAM management. However, this would not be fundamentally different from the current passive approach of adjusting the WAM by increasing the issuance of short-term debt while maintaining constant long-term issuance. Both methods are constrained by the prudent limit on the proportion of short-term debt in the total debt stock.

Currently, the proportion of short-term debt is already elevated. While there may be some capacity for this to increase relative to pre-2000 averages, the overall debt stock is significantly larger today, magnifying the associated rollover risk. With approximately $450-500 billion of short-term Treasury bills maturing each week, an increase in the short-term debt share to, for instance, 30% of the total, would substantially heighten the operational risk associated with rolling over this debt.

In conclusion, the $10 billion buyback was a routine, pre-planned cash management operation. It was not a discretionary market intervention by Secretary Bessent, nor a change in the Treasury's approach to debt management.