US Treasury Supply-Demand Dynamics and Market Stress

Structural Challenges in Issuing $10 Trillion of US Debt

The US government plans to issue $10 trillion in Treasuries in 2025 to address escalating fiscal deficits and the looming debt crisis. This issuance significantly surpasses historical levels (net issuance was approximately $1.7 trillion in 2023), posing serious challenges to the market’s absorption capacity.

Under the current $10 trillion issuance plan, assuming major international buyers like China, Japan, and European nations maintain their historical participation rate of around 35%, approximately $3.5 trillion of demand could be expected. However, this would still leave a substantial funding gap of $6.5 trillion. Furthermore, escalating trade tensions, such as additional tariff hikes by the US, could push foreign demand below 30% (under $3 trillion), compelling the US to raise issuance yields to attract funds. Meanwhile, domestic capacity to absorb debt faces its own challenges.

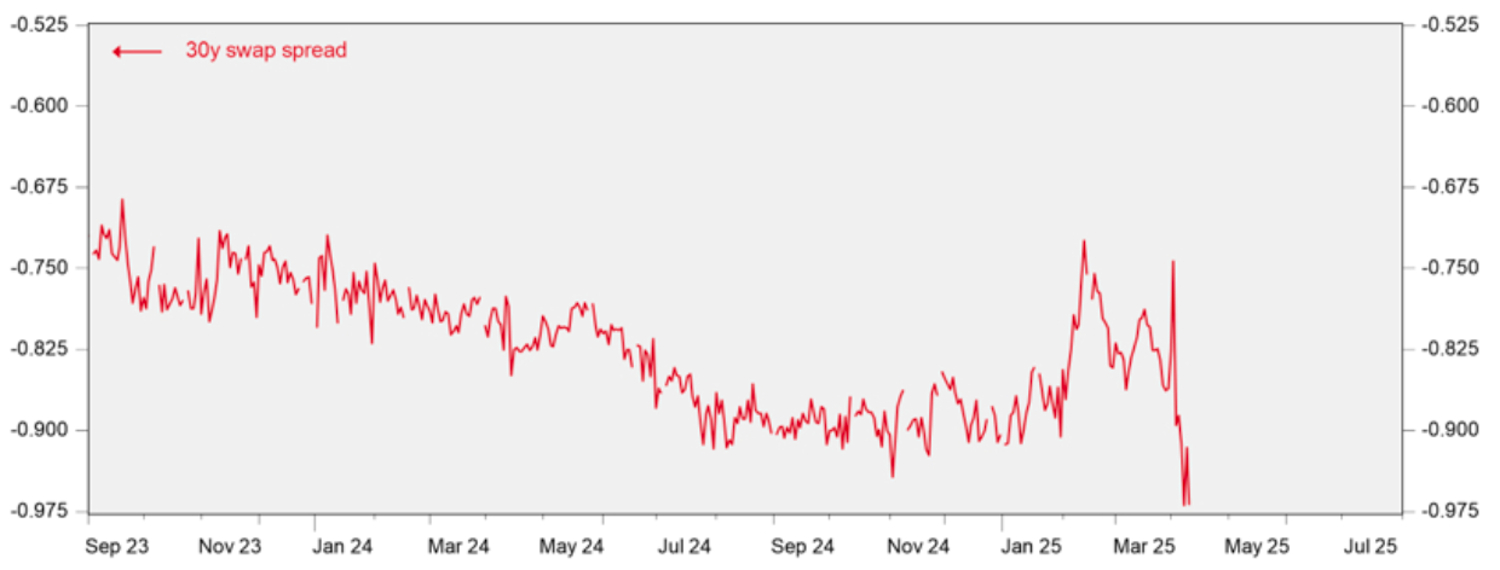

Although entities such as the Federal Reserve, pension funds, and banks could theoretically fill the gap, recent market signals have been discouraging—highlighted by a record-low 6.2% allotment to domestic direct bidders at the latest 3-year Treasury auction, reflecting weak domestic investor appetite. Additionally, liquidity constraints persist within the banking system, evident from persistently low swap spreads, signalling banks’ diminished capacity to absorb selling pressure in Treasuries. This dual pressure, both domestic and international, is creating systemic stress in the Treasury market.

The dynamics of the bond market are not only linked to domestic economic conditions but also closely intertwined with global trade and geopolitical considerations. Foreign governments’ appetite for US Treasuries is influenced by various factors, including confidence in the dollar, global economic trends, and shifts in trade policy. For instance, increased tariffs by the US could prompt retaliatory measures from key trading partners, further weakening their willingness to purchase US debt. A drop in foreign demand could drive yields higher, increasing the government’s borrowing costs and elevating market interest rates, potentially triggering ripple effects across sectors like real estate and consumer loans.

To address the funding gap, the Federal Reserve may be compelled to initiate a third round of quantitative easing, injecting liquidity through Treasury purchases. Yet, such a move could exacerbate inflationary pressures, further eroding the dollar’s purchasing power and raising market concerns about long-term economic stability. Moreover, bond market volatility could influence trade negotiations and tariff agreements, with countries potentially leveraging the US’s urgent financing needs to achieve more favourable trade terms.

Historical Reference: The 2020 Q1 Treasury Sell-off Crisis

In the first quarter of 2020, the COVID-19 pandemic triggered intense global financial turmoil, leading to unprecedented selling pressure in the US Treasury market. Research from the NBER indicates that foreign investors sold approximately $287 billion in US Treasuries, driven primarily by foreign official institutions such as central banks and sovereign wealth funds. These sales predominantly targeted long-term bonds, while the purchase of short-term Treasury bills remained relatively limited. This large-scale sell-off severely impaired market liquidity, prompting emergency intervention from the Federal Reserve, including the launch of quantitative easing in March 2020, purchasing over $1 trillion in Treasuries in a brief period to stabilise the market.

Similar episodes have occurred in other financial crises. For example, during the 2013 “Taper Tantrum,” foreign investors also became net sellers of US Treasuries, though on a smaller scale than in 2020. Likewise, in September 2022, the UK government’s “mini-budget” triggered sharp volatility in UK gilt markets, forcing intervention by the Bank of England.

These historical precedents indicate that during heightened periods of global economic or policy uncertainty, foreign investors might massively liquidate their holdings of US Treasuries, significantly disrupting markets. Considering the planned issuance of up to $10 trillion in US debt in 2025, a similar market upheaval may recur if foreign demand declines.

Recent Auction Weakness and Liquidity Stress

Recent US Treasury auctions have displayed marked divergence, with weak demand at the short end and relatively stable performance at the long end. The 3-year Treasury auction was notably poor, with direct bidders’ share plunging to 6.2%, sharply lower than last month’s 26%, signalling a near-collapse of domestic demand. In contrast, the 10-year and 30-year Treasuries benefited temporarily from optimism triggered by the “90-day tariff suspension,” exhibiting relative stability. However, market participants remain cautious regarding the long-term sustainability of demand.

Meanwhile, various liquidity indicators continue to deteriorate, exacerbating market stress. The MOVE index remains elevated at highs not seen since early 2024, indicating heightened volatility and pricing disruptions. Swap spreads are approaching historical lows, reflecting increasing pressure on dealers’ balance sheets and deteriorating market-making capacity. Additionally, the SOFR-ON RRP spread rose to 17 basis points, hitting a non-month-end record high and underscoring sharply increased interbank funding costs. According to J.P. Morgan’s assessment, the liquidity situation in the Treasury market has reached a state of “moderate deterioration,” and should foreign investors withdraw further, liquidity strains could quickly escalate into systemic risk.

Is the Cash-Future Basis Trade a Decisive Factor?

In recent weeks, Treasury yields surged during Asian trading hours but retreated somewhat in the US session. Overall, the 10-year and 2-year yields rose by 8 bps and 20 bps, respectively, significantly flattening the yield curve. The surge in 2-year yields primarily stemmed from improved market sentiment following Trump’s tariff postponement announcement. The sharp rise and subsequent decline in 10-year yields have sparked widespread speculation, with prevailing theories pointing to the unwinding of cash-future basis trades as a major driver.

Yet, such interpretations remain uncertain. On the one hand, yesterday’s yield spike occurred during the Asian session, typically the lowest liquidity period, making it improbable for hedge funds to choose this timeframe for unwinding significant positions. More importantly, today’s J.P. Morgan report analysed relevant market indicators associated with cash-future basis trading around the tariff news. Theoretically, if spot selling originated from basis trade unwinds, substantial widening should have occurred between the cheapest-to-deliver bonds and other Treasuries, as basis traders predominantly sell CTDs. However, J.P. Morgan’s analysis reveals no significant widening in the CTD-to-non-CTD spread.

It is important to reiterate that any Treasury spot selling could produce the observed rise in yields from Monday to Tuesday and the associated narrowing of swap spreads. This is because Treasury spot instruments are the least liquid and most sensitive to selling pressure among interest rate products compared to derivatives. Hence, market signals alone cannot conclusively identify the sellers, who could be engaged in basis trades, risk parity strategies, or retail and other institutional investors. Given the Asian session timing of the sell-off, it’s more plausible that the selling originated from the Asian private sector, particularly Japan, as indirectly evidenced by a concurrent significant appreciation of the Japanese yen.

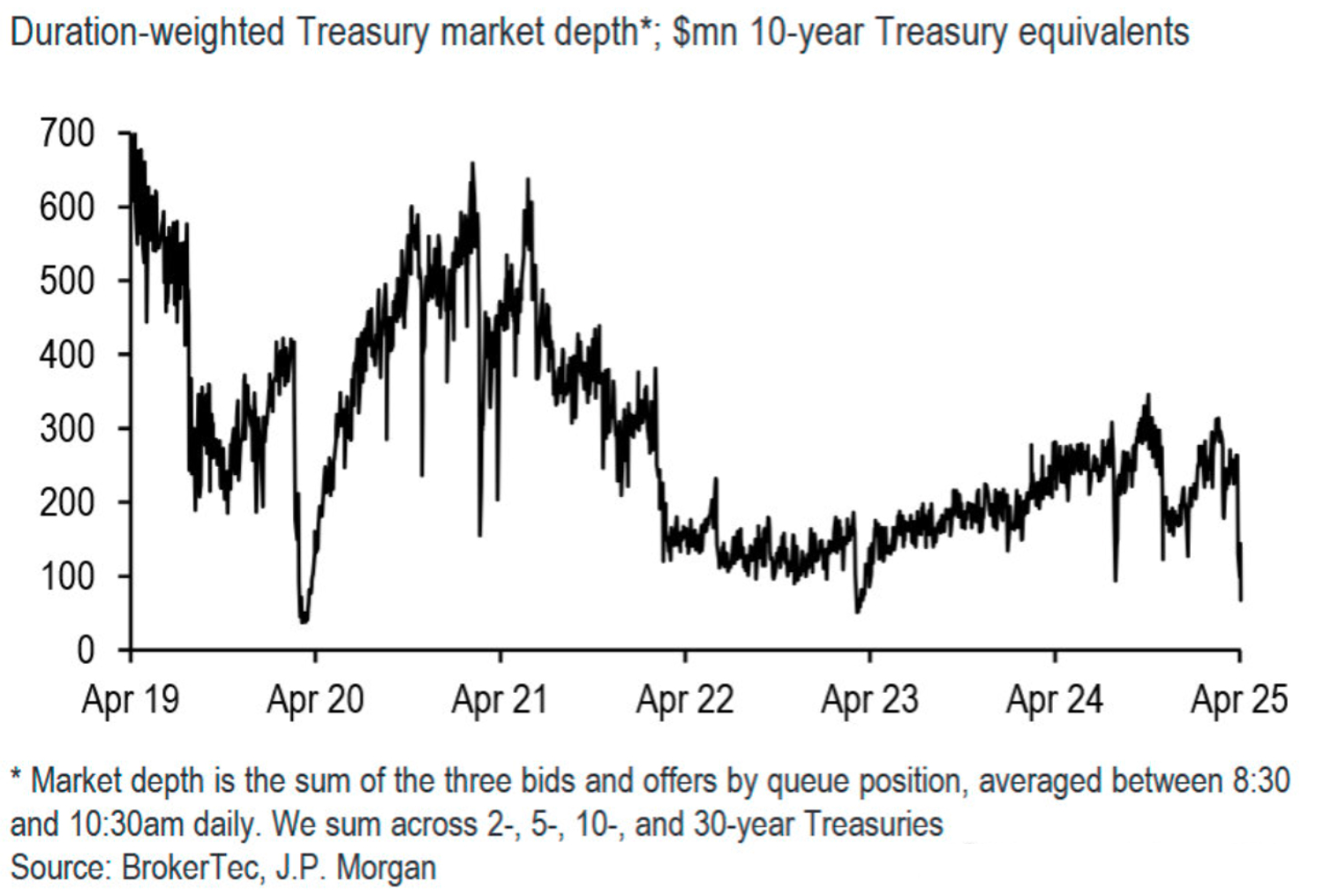

From the broader perspective of Treasury market liquidity, conditions have somewhat improved. J.P. Morgan’s market depth indicator rebounded modestly, though it remains relatively weak. Additionally, swap spreads, reflecting dealer balance sheet pressures from selling, rebounded noticeably yesterday. The 10-year Treasury auction result also outperformed expectations, stopping through by 3bps—the largest positive surprise since 2021.