The epic crypto market liquidation of October 10th and 11th, 2025, is destined to go down in history. According to Coinglass, nearly $20 billion in delta one contracts were liquidated within 24 hours, and the actual liquidation volume may far exceed the record. The altcoin market was the hardest hit by these liquidations: BTC and ETH accounted for only about half of the liquidated positions; considering that their combined market share is close to 72% of the total, the scale and intensity of the altcoin liquidations can be imagined.

Many are searching for the culprit behind the liquidations. Some blame Trump's "Truthsocial blitz," while others point to flawed mechanisms within some exchanges. However, regardless, this "epic liquidation" was likely unavoidable; the seeds of potential risk were sown three months or even longer in the past.

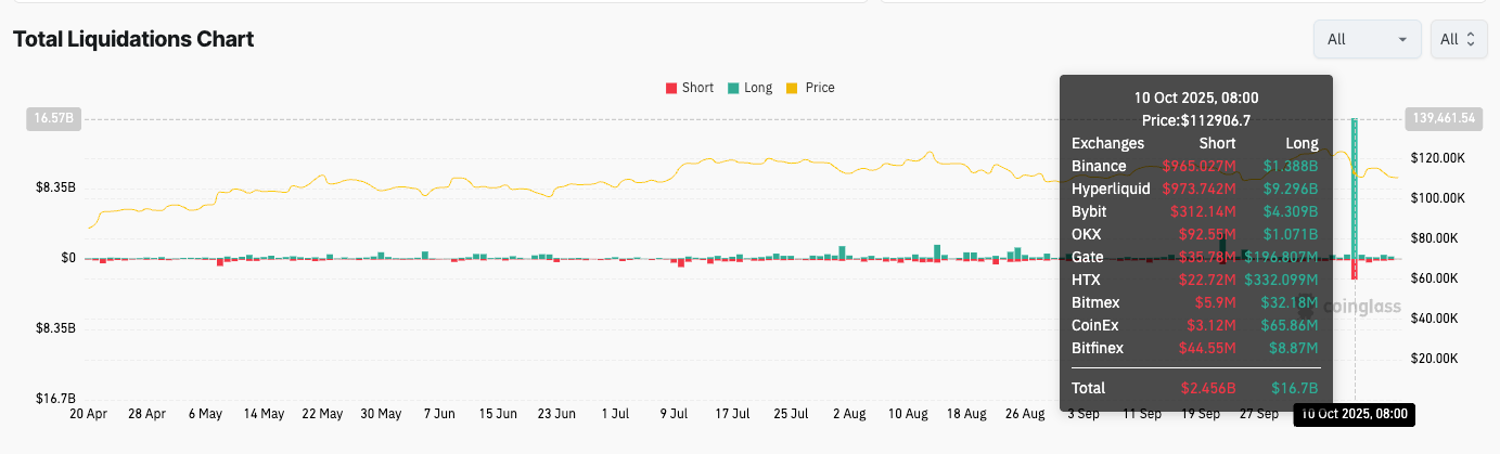

Compared with the epic liquidation on Oct 10, the scale of liquidation in the previous six months can even be described as "insignificant." Source: Coinglass

How Did the Seeds of Liquidation Germinate?

As a secondary, long-tail asset class, altcoins have historically been synonymous with "high risk" and "low liquidity." Institutional investors and altcoin investors seem to exist in two separate worlds. Aside from limited risk management needs, institutions rarely engage in altcoin-related businesses, and ETFs and other investments are naturally excluded from the vast majority of altcoins. As a result, altcoin liquidity comes almost entirely from within the crypto market, leading to a strong correlation between altcoin performance and the degree of liquidity easing. Given that altcoins are denominated mainly in US dollars, the actions of the Federal Reserve and the Trump administration, along with fluctuations in US dollar liquidity, directly determine altcoin trends.

It must be acknowledged that the current liquidity environment is not hospitable to altcoins. Despite record-breaking stablecoin issuance, most of these stablecoins continue to flow into mainstream cryptos like Bitcoin and Ethereum or are used for payment purposes, leaving limited liquidity available for altcoin investment. Furthermore, central bank liquidity supply is not always smooth sailing: the European Central Bank's current cycle of interest rate cuts is nearing its end, while the Bank of Japan has already entered a period of liquidity contraction. The Federal Reserve is one of the few central banks still providing liquidity, but its "slow and steady" pace of interest rate cuts means that while liquidity can meet the needs of primary underlying assets, it doesn't necessarily satisfy the needs of secondary assets like altcoins.

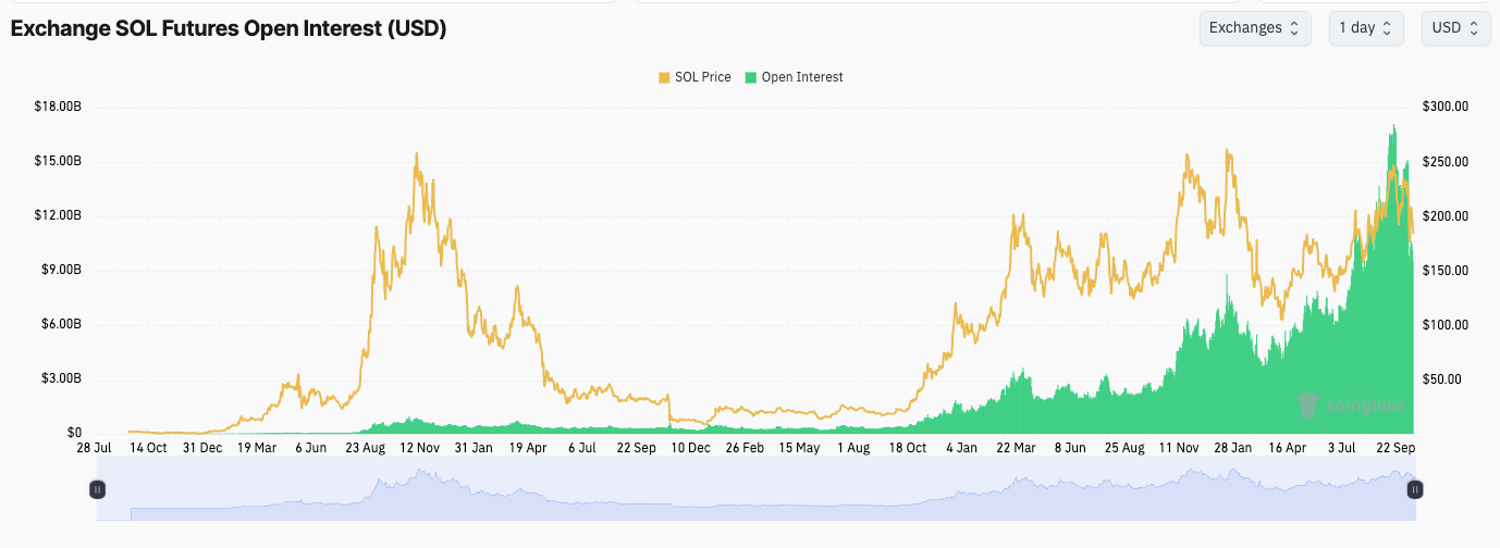

Under insufficient liquidity, the only thing that can support the prices of non-BTC crypto assets is leverage. Compared to 2021, when BTC reached $120,000, open interest in BTC perpetual swaps increased 4x. In contrast, while the prices of ETH and SOL haven't significantly broken through their historical highs, open interest in ETH perpetual swaps has increased 6x, and open interest in SOL perpetual swaps has increased 20x. The situation is similar for many altcoins. This means that the prices of the vast majority of non-BTC cryptos are almost entirely supported by leverage, significantly increasing their sensitivity to changes in liquidity.

The price of SOL has not broken through its previous high, but the open interest of its perpetual contract has increased 20x. Source: Coinglass

Similarly, leverage played a significant role in the 2024 US stock market bull run, particularly in small and mid-cap stocks. Therefore, the subsequent risk-off and deleveraging trends that followed April's "Liberation Day" were unsurprising. This is the natural course of market operations, but for the Trump administration, a sharp stock market decline was "unacceptable." Trump began demanding that the Fed slash interest rates to support the market, but faced with inflation risks, Powell was clearly unwilling to do so.

Since the president could not influence the Fed's independence (at least at the time), Trump seemed somewhat helpless. But he and his team quickly found an alternative: fiscal measures. Treasury bonds are one of the most popular collateral in the market, and banks have ample cash. Simply issuing a large number of Treasury bonds and then converting them into cash through financing channels could increase market liquidity.

This approach was not unique to Bessent. During economic difficulties (such as the Covid-19 pandemic in 2020 and the regional banking crisis in 2023), Treasury financing has often been a key means of relief alongside interest rate adjustments. However, this was likely the first time that it was used to influence real interest rates. Clearly, Bessent and Trump didn't care; they simply wanted "the stock market to rise and reach new highs."

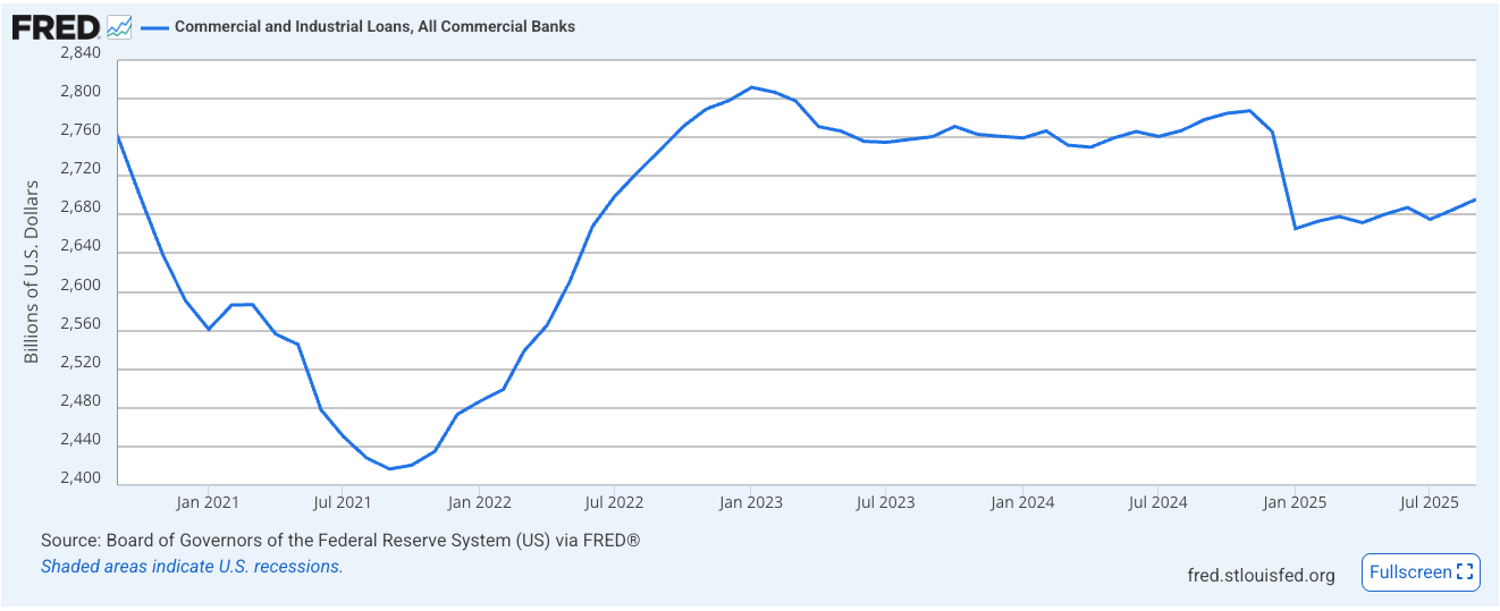

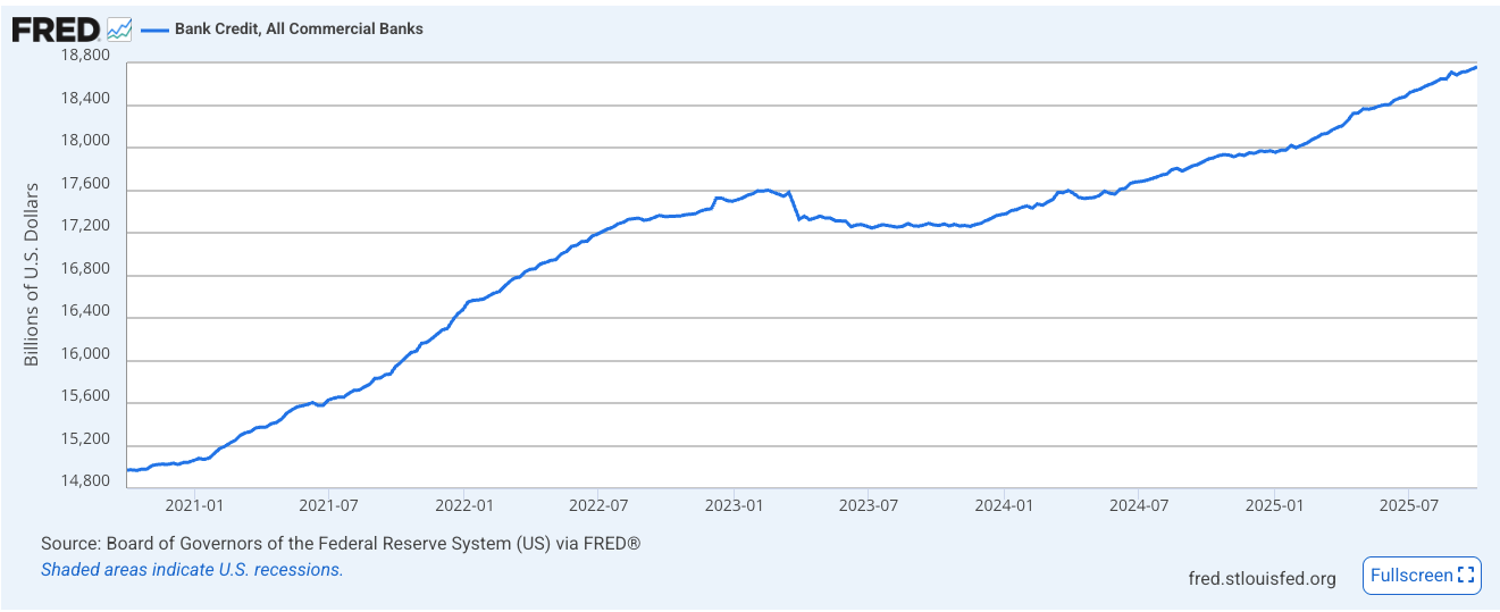

As a result, we witnessed an unprecedented expansion of the debt. In August, the amount of new T-bills issued in a single week exceeded $100 billion, while the debt ceiling was "indefinitely raised" through a series of debt-increasing bills, including OBBBA. Large amounts of bank credit were used to support the stock market, and both the stock and crypto markets quickly recovered from their lows, as expected. The SPX and QQQ hit new highs, while underperforming cryptos like ETH also set new historical records through DATs and other methods.

While commercial, industrial and consumer loans did not show significant growth, the total credit scale even accelerated in 2025, indicating that a large amount of credit may have entered the financial sector, such as the stock market. Source: St. Louis Fed

Of course, the Trump administration's actions are not without cost. The massive issuance of T-bills has directly led to a "less healthy" liquidity structure: in 2021, T-notes and T-bonds were a significant component of new liquidity, but now, T-bills account for almost entirely of new liquidity. T-bills typically mature within a year, making it difficult for investors to use T-bills-based liquidity for long-term investments. This forces them to be used only for short-term trading or even speculation. Furthermore, the shorter duration of Treasury necessitates frequent issuance and rollovers to maintain current liquidity levels, leading to rapid liquidity fluctuations over short periods, which undoubtedly increase market fragility and potential risk.

In response to potential liquidity risks, everyone from whales to retail investors sought to achieve their profit targets in the "shortest possible" time. Leveraging the massive influx of short-term liquidity and readily available Delta 1 leverage, everyone was desperately trying to push prices higher. The lack of liquidity in the crypto market wasn't a problem; DATs enabled many cryptos to achieve a "disguised listing," indirectly receiving "liquidity airdrops" from Bessent. Retail investors followed the whales' lead and went long, driving the price of ETH and many other cryptos up by over 60% in just two weeks. Many profit targets that would have previously taken months or even years were achieved in just a few weeks.

We shouldn't blame these investors; they just made the best choice given the current liquidity environment. But the facts remain: massive amounts of leverage accumulated in the crypto market in a short period of time, and all the epic liquidation needed was a trigger.

How Did Deleverage Explode?

Liquidity risks had already begun to surface in early October. With the US government shutdown and the halt in economic data releases, investors struggled to make decisions, and risk aversion was already brewing. Another issue posed by the government shutdown was that, while it didn't affect Treasury auctions, the heightened uncertainty raised collateral risks, undoubtedly negatively impacting liquidity.

Trump's threat of a trade war served as the direct trigger for leveraged liquidations. When faced with macroeconomic risks, investors typically first reduce their portfolio's leverage and gradually sell off their high-risk assets. Due to excessive leverage accumulation in the market, once selling began, many investors holding this leverage started experiencing automatic liquidations or margin calls.

Notably, some commonly used risk mitigation mechanisms in the crypto market (such as unified accounts and cross-asset margin) can actually amplify volatility when deleveraging occurs. Because deleveraging doesn't discriminate based on underlying assets, when margin calls are issued, the exchange's risk control system will sell available collateral in the account to support positions and avoid liquidation. However, the selling of assets triggered a chain reaction: the prices of certain illiquid assets (such as some altcoins) plummeted significantly upon being sold. This price drop led to the liquidation of leveraged positions linked to these assets. This further drove down prices and collateral devaluation, prompting the system to sell collateral even more aggressively. This created a vicious cycle until prices reached zero, which is what happened on Oct 10 and 11.

So, are low-leverage or arbitrage positions safe? Clearly not. In the derivatives market, the ADL (Automatic Deleveraging) system takes precedence over all systems and accounts. Mainstream coin arbitrageurs were fortunate: thanks to relatively ample liquidity, their positions did not suffer losses. However, for altcoins, the liquidity collapse occurred in a matter of minutes. At this point, the ADL mechanism kicked in, liquidating arbitrage positions, and delta neutrality became ineffective. In the subsequent decline, even relatively conservative arbitrageurs suffered heavy losses.

The automated selling of large amounts of collateral also claimed additional victims. USDe, currently the third-largest stablecoin in the market (in fact, a "money market fund"), has also experienced significant selling. USDe can be used as collateral within an account, but unlike USDT and USDC, it cannot be used directly for trading and clearing. Therefore, in the event of a deleveraging, USDe will be quickly converted into stablecoins like USDT and USDC.

Staking USDe can earn interest. Many crypto investors, despite understanding the potential risks of altcoins and liquidity, are unconcerned about the potential of USDe. What could be wrong with a "stablecoin"? To maximise returns, they employ a "repeated pledging" strategy widely used in the 1990s:

- Stake USDe to obtain USDT or USDC.

- Buy USDe with USDT/USDC.

- Stake USDe again, repeating the previous two steps.

Those familiar with financial history will immediately recognise this strategy as the one employed by LTCM. They used this strategy to multiply their positions in Treasury bond arbitrage. Still, a single event (the Russian Treasury default) caused all positions, along with the entire fund, to become part of history.

The same situation recurred in October. Due to the high leverage caused by "repeated collateralisation," the sharp fluctuations in USDe prices led to the liquidation of these "wealth management positions." The entire crypto market was in panic; however, likely, this is not the end of this round of deleveraging, but only the beginning. The resurgence of regional banking crises has indicated a further deterioration in liquidity conditions and has led to increased risk aversion. How long this trend will last remains unknown.

How to Prevent Such Risks?

- Stay Alert to Market Risk Signals.

One of the simplest ways to monitor potential leverage risk is by watching open interest (OI), a metric that shows how many futures contracts are currently open. A spike in OI means lots of new positions are being opened, often with high leverage, indicating speculation is running hot.

In practical terms, when OI is surging, many traders are piling into bets using borrowed money, which can lead to more violent price swings. Conversely, a drop in OI suggests traders are closing positions or getting liquidated, which can actually stabilise the market as risky bets wash out.

Keeping an eye on OI can tip you off to rising risk. If you notice OI climbing rapidly alongside euphoric sentiment, it's a signal to be cautious; the market may be over-leveraged.

According to data from Coinglass, which tracks top cryptos' open interest, the total open interest in the crypto market reached an all-time high before the market crash on Oct 11. Market sentiment was extremely bullish, with many investors anticipating a strong "Uptober" rally. However, such euphoric conditions often precede heightened volatility, making it a critical time to tighten risk management strategies.

Source: Coinglass

- Stick to High-Liquidity Tokens.

Larger-cap coins tend to have deeper liquidity, meaning it’s easier to buy/sell them without drastic price swings. During crashes, liquidity is king. High-liquidity assets like Bitcoin and Ethereum have heavy trading volumes and big buyer/seller interest, so their prices, while volatile, won’t typically free-fall in seconds.

In contrast, low-liquidity altcoins can see their order books dry up, there are few buyers when everyone rushes for the exits.

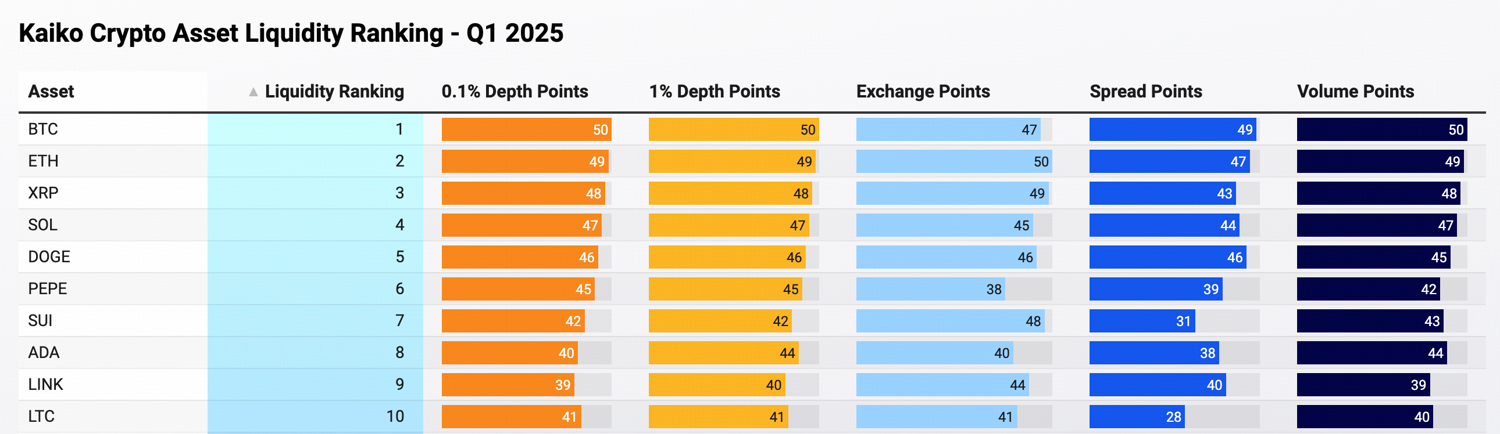

Research platforms such as Kaiko periodically publish crypto token liquidity rankings, providing investors with insights into which tokens are the most liquid.

Source: Kaiko

However, some tokens may appear highly liquid due to market-making activities rather than genuine investor demand. While in normal conditions, market makers can help maintain liquidity, during periods of market turbulence, they may withdraw to protect themselves, causing liquidity to evaporate rapidly. This makes it difficult to distinguish which assets have real, sustainable market interest. Since even experienced investors may find it hard to tell the difference, truly risk-averse participants may be better off sticking with Bitcoin and a handful of widely accepted tokens such as ETH, SOL, and XRP.

- Be Careful with Collateral and Leverage.

Crucial to long-term survival is understanding fundamental risk management, especially regarding collateral and leverage. Many crypto investors learned this the hard way: using volatile assets as loan collateral or taking on heavy leverage can wipe you out fast.

For example, if you borrow money against volatile assets, a sudden price drop in those assets can trigger a margin call or automatic liquidation. In plain terms, the exchange or lending protocol will sell your crypto (collateral) if its value falls too much, potentially at rock-bottom prices, to repay your loan.

It’s best to use only the most established and liquid stablecoins, USDT and USDC, as trading collateral. These stablecoins have the strongest market depth, widest adoption, and proven resilience during market stress. In contrast, lesser-known or algorithmic stablecoins can lose their peg during volatility, putting borrowers at risk of unexpected liquidation or loss of collateral value.

Leverage in trading similarly demands strict caution. While leverage can boost gains, it also magnifies losses during downturns. When using leverage, it’s crucial to consider the liquidity of the token you’re trading. Deeply liquid assets like Bitcoin or Ethereum can generally absorb large orders without extreme price swings, but low-liquidity tokens can crash 80–90% in a short time. In such cases, even a modest 2x leverage position can be completely wiped out.

Moreover, traders should also account for market volatility and liquidation mechanics. On many exchanges, price wicks caused by thin order books or sudden liquidations can trigger forced sell-offs even when the broader market hasn’t moved much. Maintaining conservative leverage levels, using stop-loss orders, and sticking to major assets with deep liquidity are key to avoiding unnecessary liquidation risk.

What’s Next for Crypto Markets?

Bitcoin’s Reinforced Role as "Digital Gold"

This flash crash underscored Bitcoin’s safe-haven status. Bitcoin’s decline was comparatively modest (13% at its worst), and it quickly stabilised. This resilience boosted Bitcoin’s market share as altcoins absorbed “immense damage”.

Altcoin Credibility Crisis

Altcoins are facing a credibility crisis. The crash exposed how fragile many tokens are in stressed conditions. Even before the crash, capital was concentrating in “high-liquidity, high-certainty” assets like BTC and ETH, while many altcoins remained far below past highs. The crash amplified this divide.

The Rise of “BTC+” Portfolio Strategies

In the aftermath, a clear investment strategy shift is emerging: the rise of “BTC+” portfolios. Rather than spreading bets across dozens of speculative alts, investors are now centring portfolios on Bitcoin and adding only selective complements, such as Ethereum or a few high-conviction plays, effectively a “Bitcoin-plus” approach. This trend is driven by hard lessons from repeated boom-bust cycles.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.