Defending Against More "YOLO"

As investors opened the economic calendar, a wave of key economic data (such as the PPI) was not released. The CPI data, originally due in early October, was delayed until this week, but it appears to be "significantly outdated" and no longer reflects current economic conditions.

Numerous new sources have indicated that the US government shutdown may last "far longer than expected." Some lawmakers have stated that they believe the shutdown will continue and that there is "little to no sign" of progress toward reopening the government. The public is focusing on specific dates (such as federal employee payday, military paycheck day, and congressional staff payday). Still, the conflict between the Donkey and the Elephant will not be temporarily resolved by employee payroll issues, significantly reducing the likelihood of a government reopening.

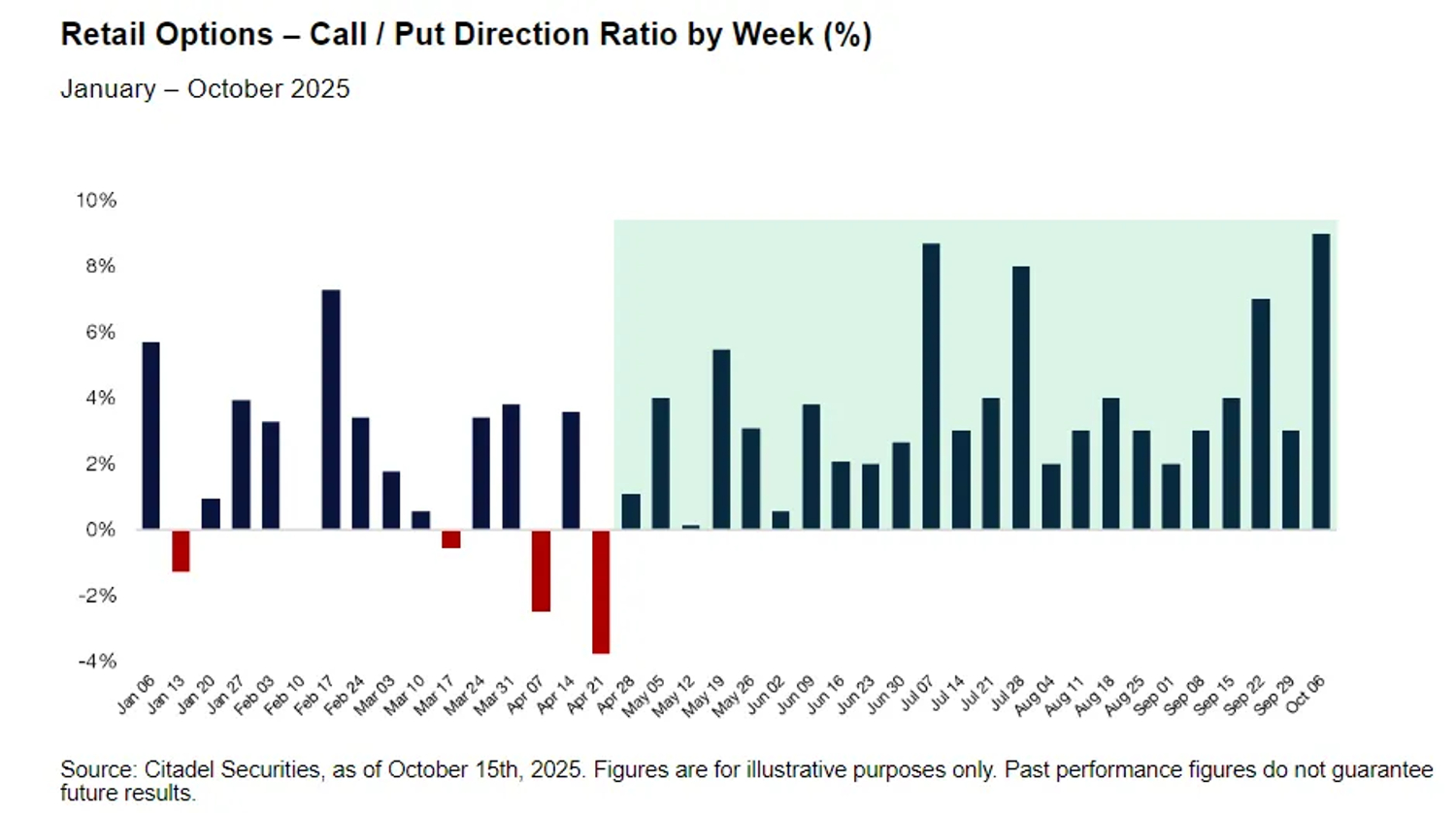

Only "events" continue to stimulate the market. The renewed risk of a trade war has led to a wave of deleveraging, but interestingly, this deleveraging has not triggered widespread risk aversion. Retail investors are actively buying on dips, and recent bullish sentiment has reached a new high since April. In the eyes of retail investors, inflation and debt are "not a big deal": the absence of inflation data is a positive development, and as long as interest rate cuts continue, dollar-denominated liquidity will continue to flow into the market. For dollar users, potential debt risks only have a negative impact offshore. Onshore, where survival depends on the dollar, the national debt is negligible—you still need to use dollars to pay your bills in daily life.

Thus, retail investors' "YOLO" sentiment is understandable. At least for now, investing in stocks won't make their situation any worse: "Oh, I have some money in my 401k, and the S&P is down. I want to buy some stocks because they can only go up. Even if I suffer short-term losses, Trump will find a way to protect the stock market, so there's no need to worry."

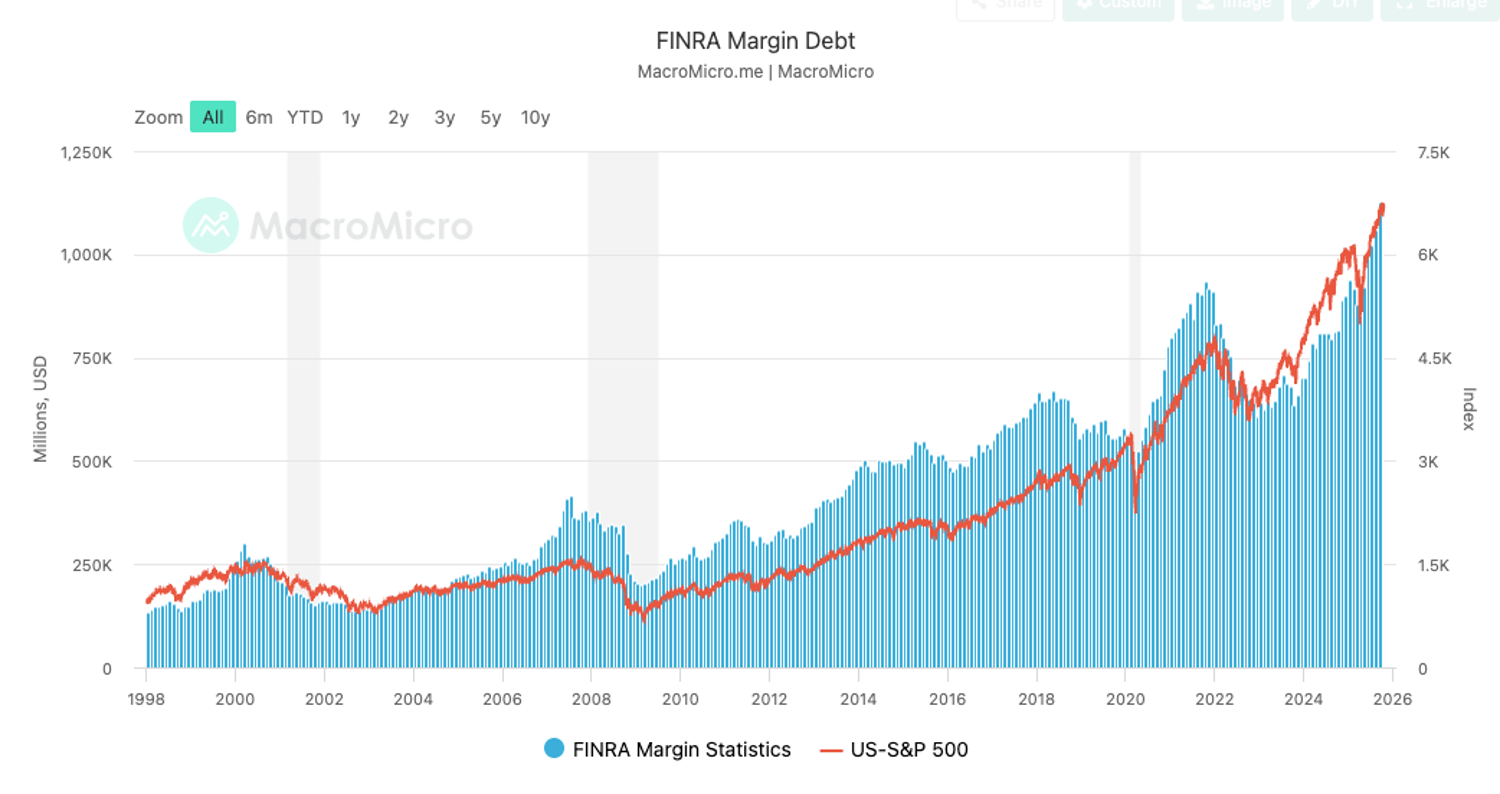

But institutional investors clearly don't see it that way anymore. All the data points to a more fragile future: margin debt has hit record highs for several consecutive months and is growing exponentially. The average duration of Treasury bonds is shrinking, and the overall quality of liquidity is deteriorating (as evidenced by the resurgence of regional banking crises), with no sign of improvement in the near future. The Federal Reserve is no longer as independent as it once was, and a more accommodative interest rate environment has already been priced into the interest rate market—despite the well-known implications of consecutive rate cuts without a sufficient easing in inflation.

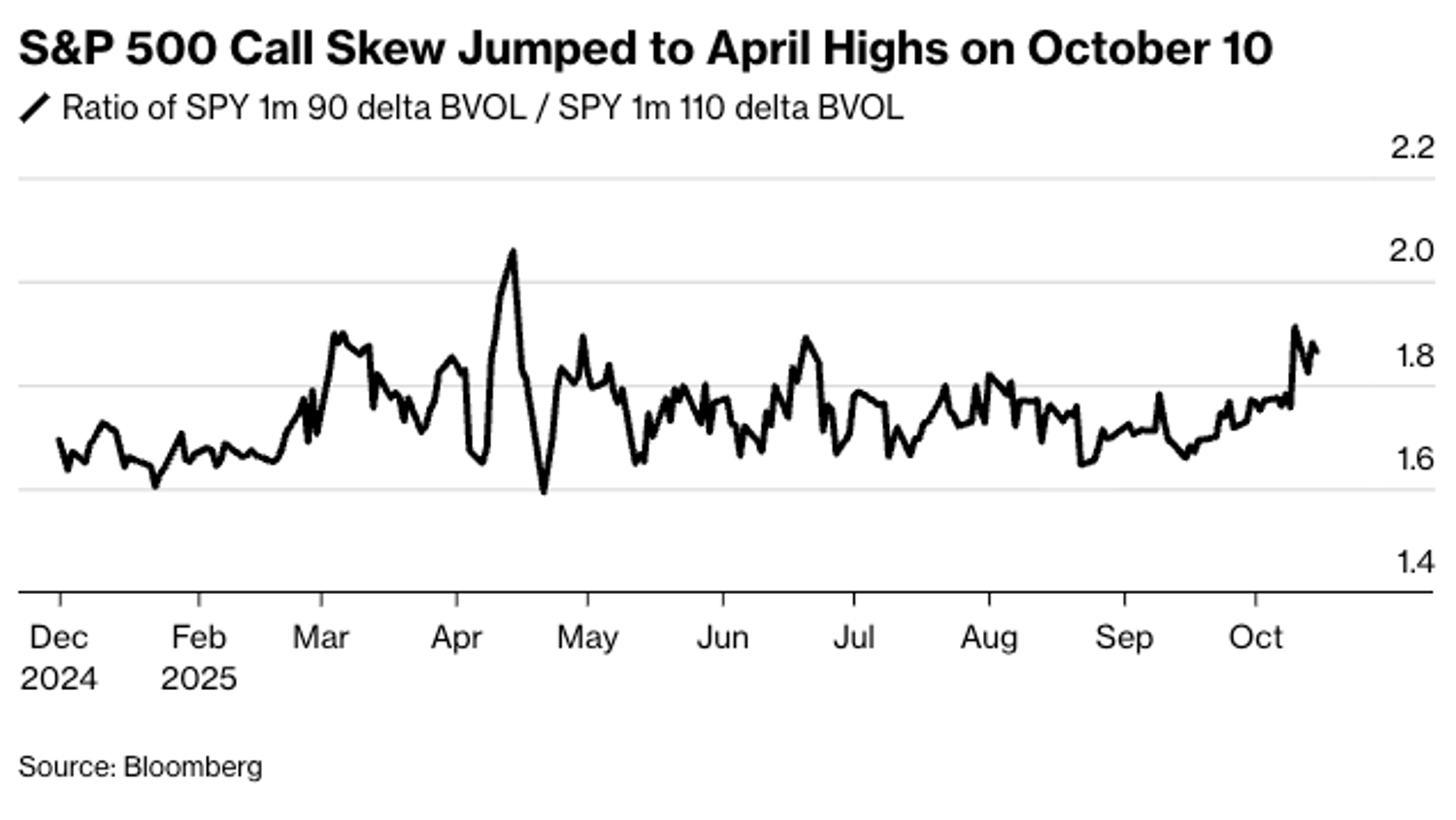

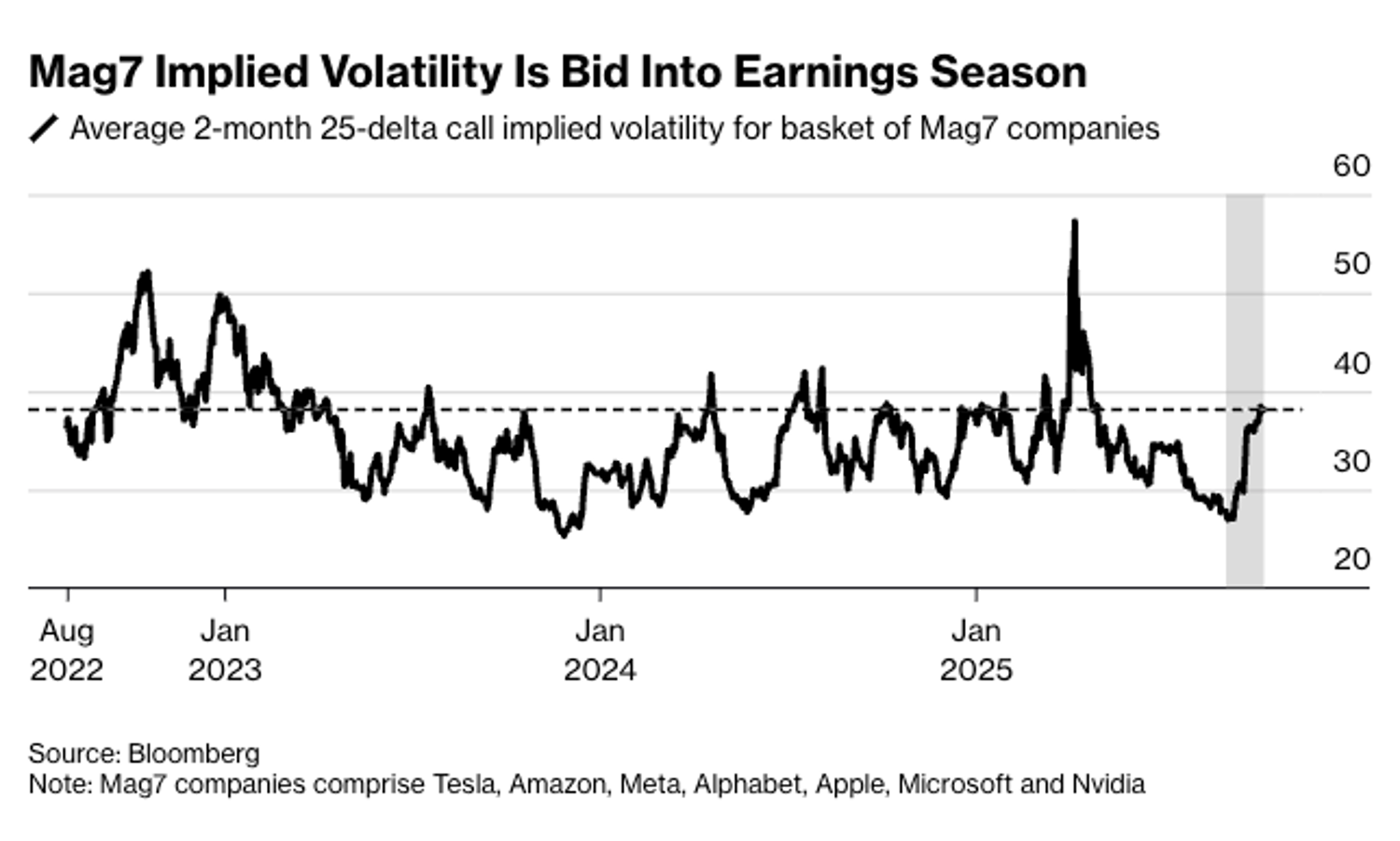

As a result, institutional investors are choosing to sell. In fact, they have been selling US stocks for five consecutive weeks. Demand for risk management in equity assets is also increasing: data from Citadel Securities shows that institutional clients are busy purchasing hedging instruments, and traders are paying to hedge against a range of potential risks during earnings season, leading the market to price in higher potential volatility in the coming weeks. "More YOLO" hasn't led to a better outlook; on the contrary, it has further deepened institutional investors' concerns.

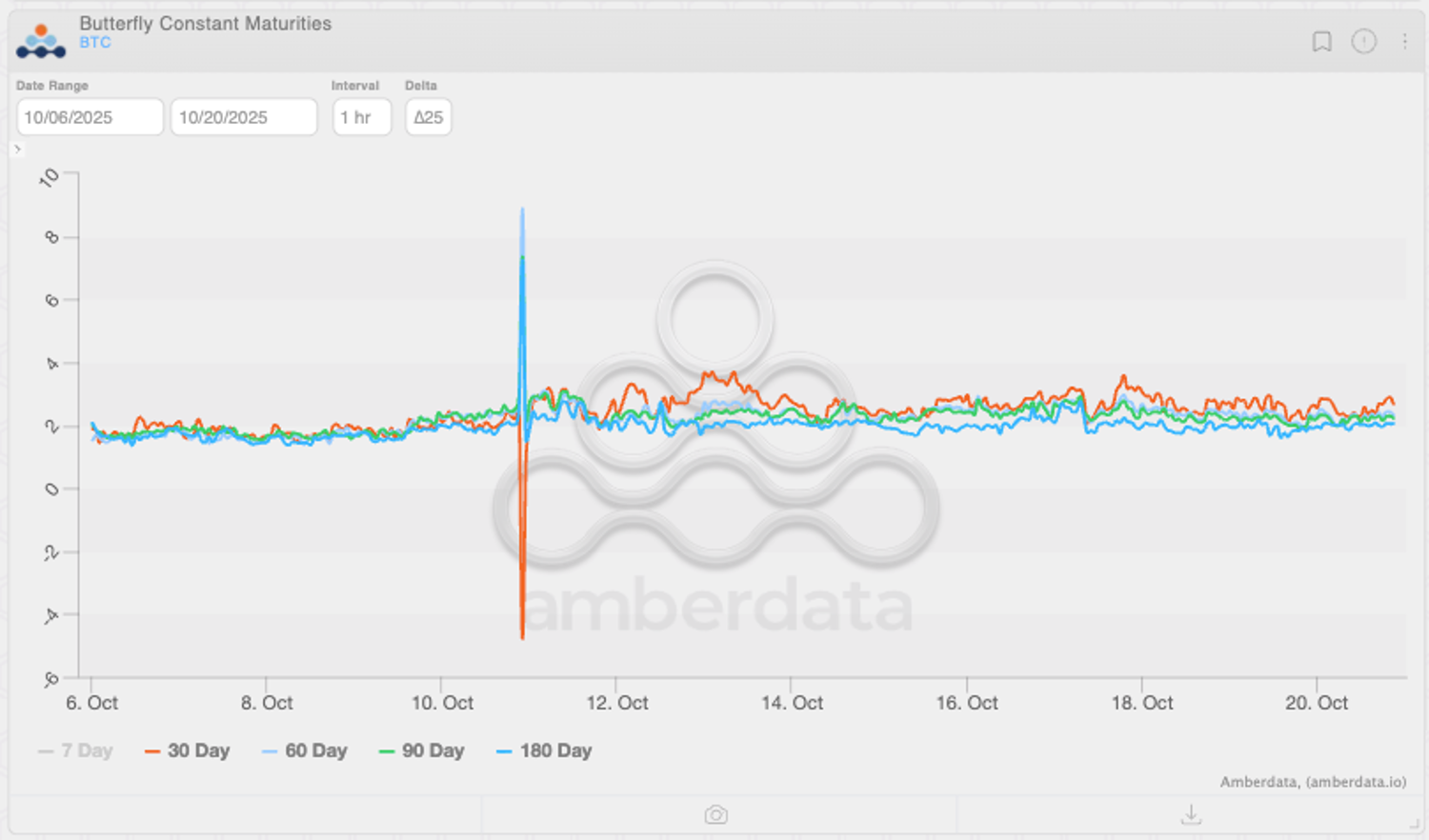

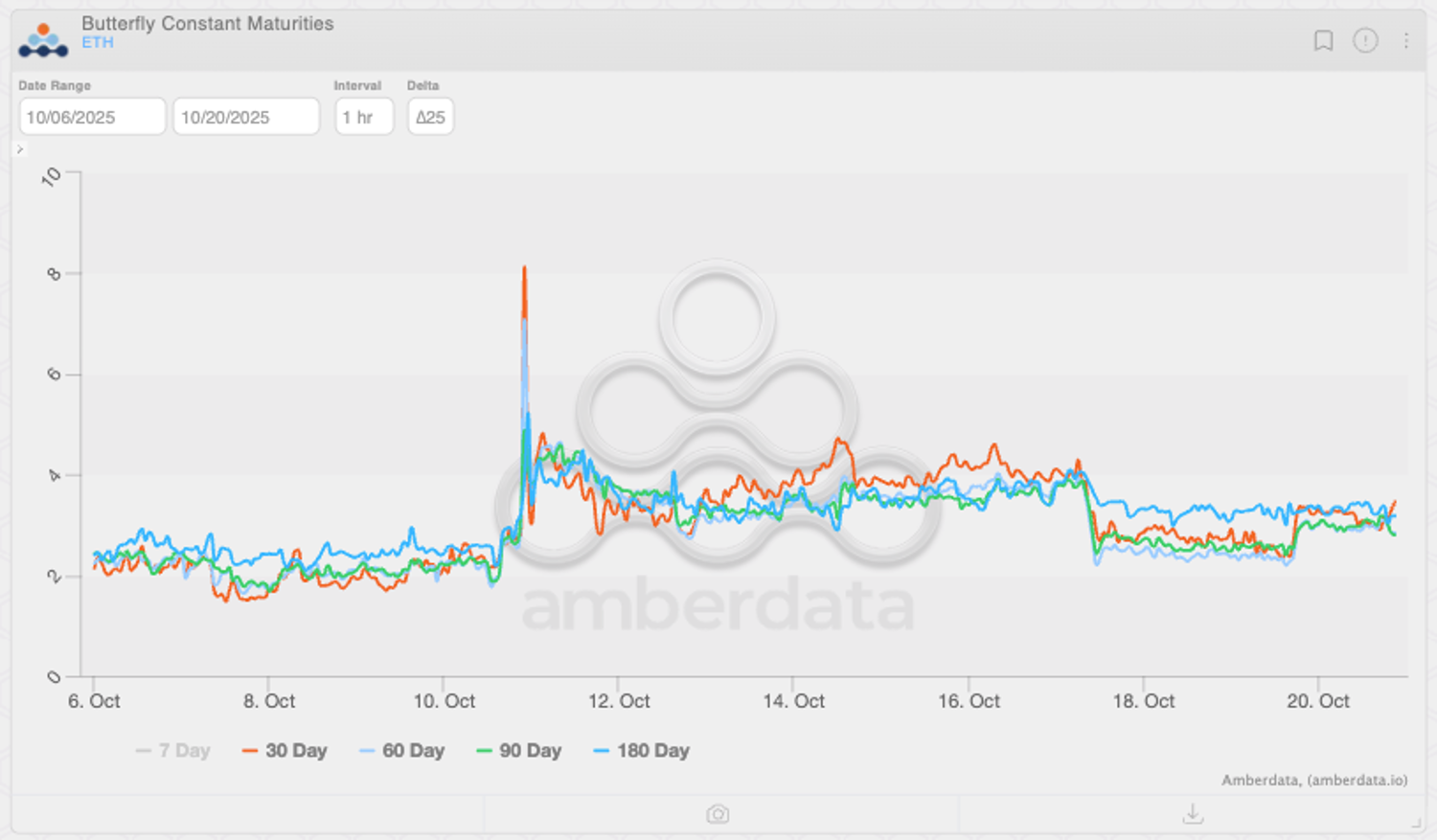

A similar situation appears to be playing out in the crypto market. While pricing in BTC's tail risk has seen only a limited increase after a brief bout of volatility around October 10th, pricing in ETH's potential volatility has increased significantly, with tail risk pricing for the coming weeks higher than in other periods. It seems that no matter which market, professional investors remain sufficiently vigilant and cautious about assets with equity attributes and closely pegged to the US dollar.

Compared to BTC, ETH is priced in higher potential tail risk by traders, especially for the next few weeks. Source: Amberdata Derivatives

New Opportunities and Diversified Trading

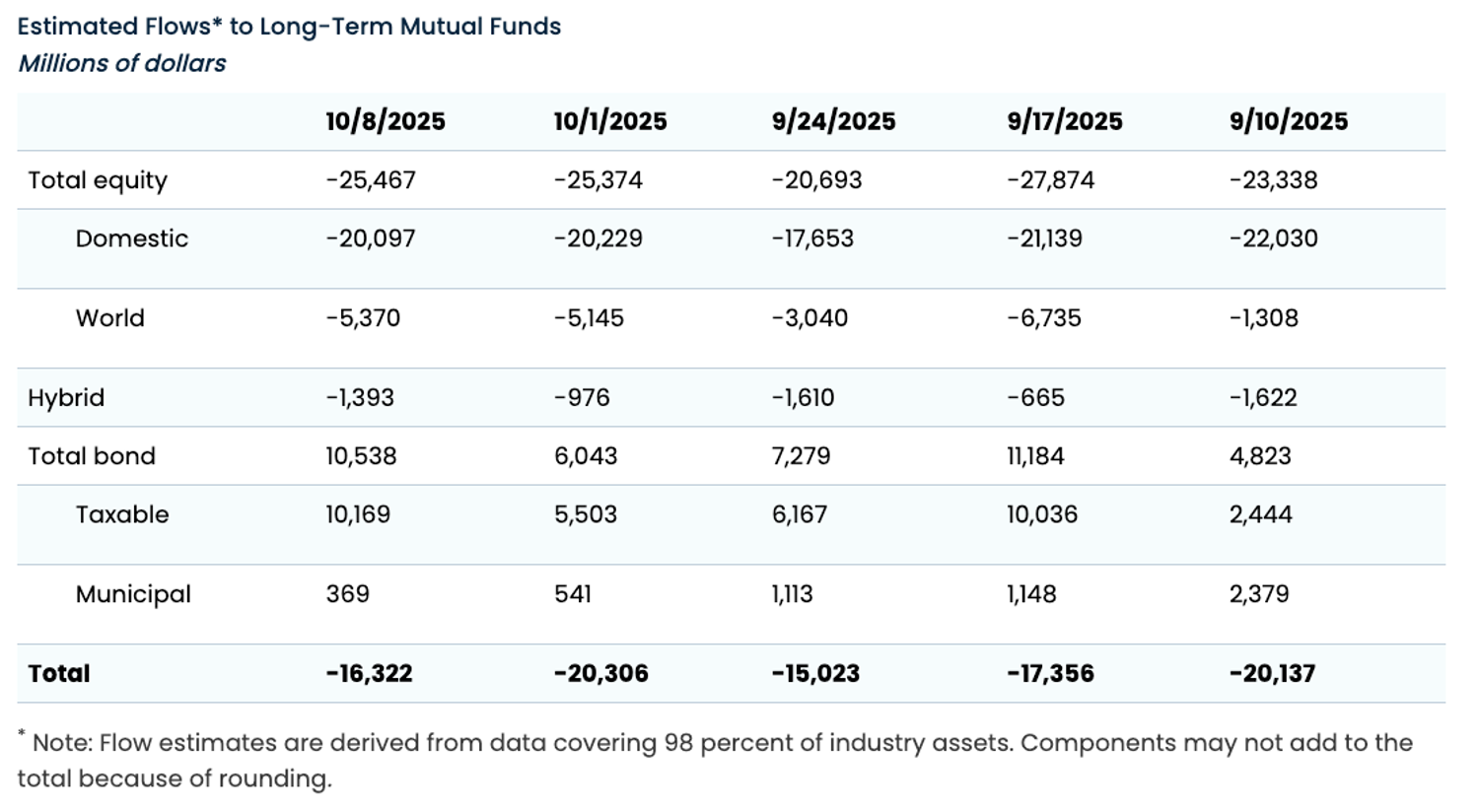

Faced with a host of potential risks for US dollar assets, institutions are reluctant to go down with the Titanic. In the first week of October alone, long-term equity mutual funds saw net outflows exceeding $25.4 billion, with $20 billion coming from domestic institutions. While significant inflows continued into bond funds, net outflows from long-term mutual funds reached $16.32 billion. Meanwhile, FX trading volume has shown a significant upward trend since April 2025, exceeding 20%-25% compared to the same period in 2024. This is because institutions are actively hedging the additional foreign exchange risk associated with the shift to offshore investments.

Long-term mutual funds have seen net outflows for five consecutive weeks. Source: ici.org

Many institutions are investing in emerging market stocks and bonds, generating substantial returns significantly higher than those from the US stock market. However, for hedge funds and trading firms facing investment restrictions, their options are limited.

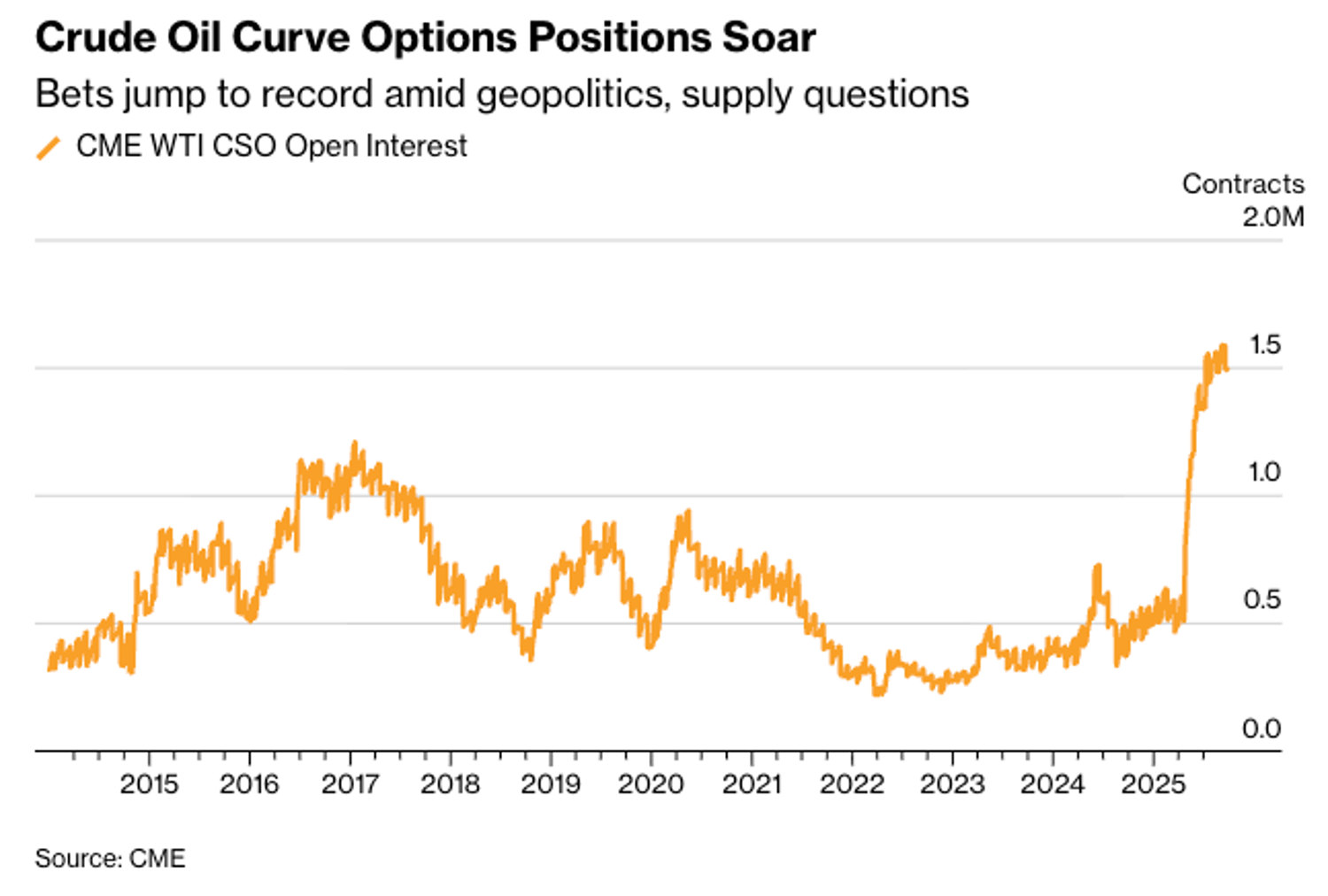

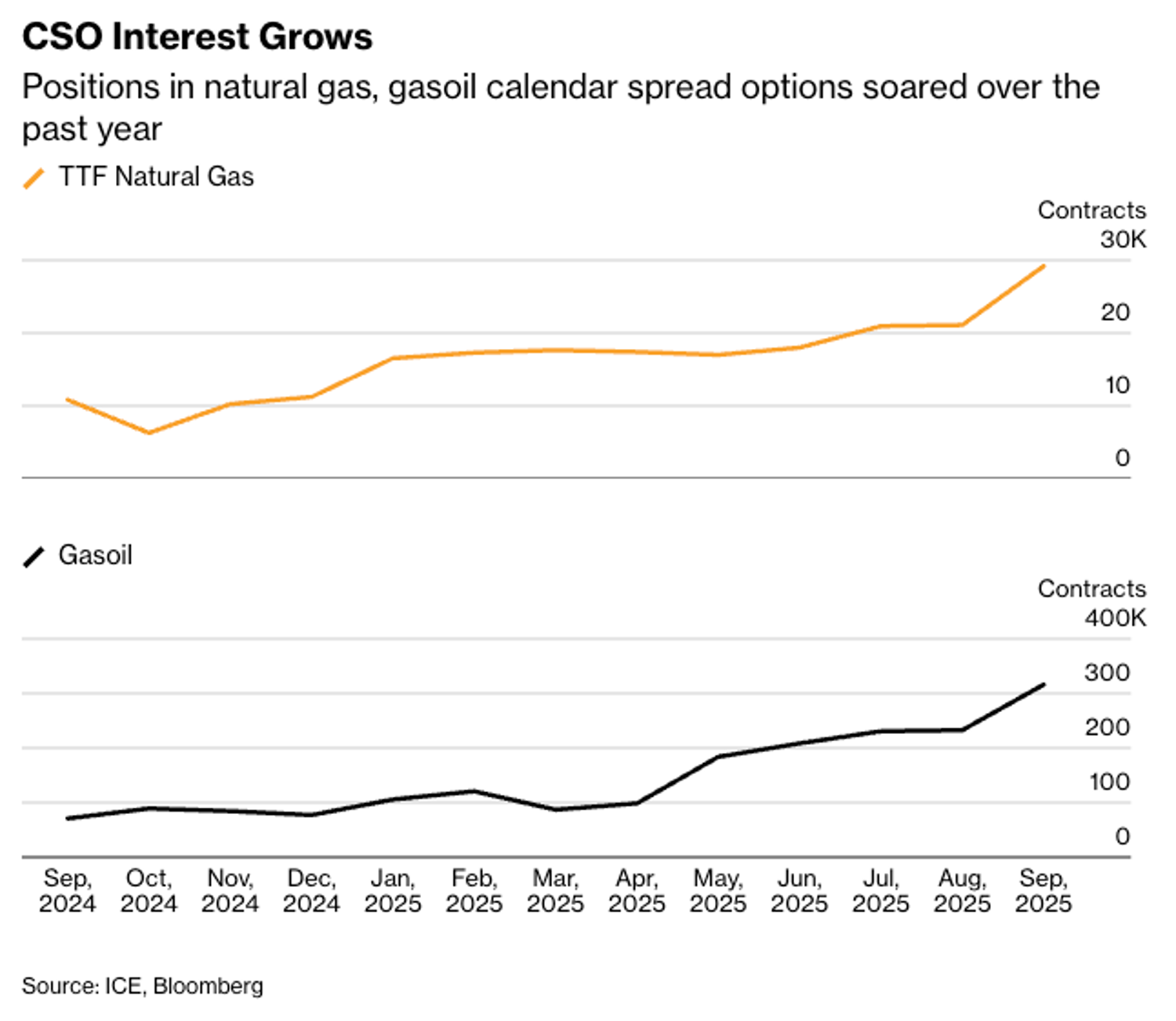

As an alternative choice, "diversification" is gaining popularity on the streets: Following the lead of major trading desks, many are beginning to explore previously untapped areas beyond equities, such as commodities, interest rates, and cryptocurrencies. Since April 2025, open interest in crude oil calendar spread options has surged by 300%, while open interest in agricultural calendar spread options has increased by 50% this year. Traders are also showing a surge in interest in natural gas and diesel contracts, not to mention gold and silver, already considered among the "star assets of 2025."

It's worth noting that these investments aren't solely driven by increased hedging demand due to geopolitical and trade risks. Calendar spread strategies have long been a favourite "safe" strategy for hedge funds, but it's clear that overall stock risk is accumulating due to YOLO sentiment and high leverage. A few words from Trump can trigger significant fluctuations in specific stocks. Even if traders can effectively respond through AI agents and robust infrastructure, the increased volatility in net asset value will raise concerns among LPs.

It's understandable, therefore, that fund managers are favouring "diversified trading." Commodities and interest rate markets have relatively low correlation with stocks, and with increasing participation, liquidity is improving, providing a good foundation for the deployment and implementation of multiple strategies. Similarly, the fund's net value also benefits from relatively low correlation and a relatively larger market. Especially when the stock market becomes increasingly regionalised and more easily manipulated by various factors, the net value changes of a diversified investment portfolio are relatively more stable.

Economic Calendar of This Week

Wednesday 06:00

- UK Inflation Rate YoY

Thursday 14:00

- US Existing Home Sales

Friday 06:00

- UK Retail Sales MoM

Friday 08:30

- UK S&P Global Manufacturing PMI Flash

- UK S&P Global Services PMI Flash

Friday 12:30

- US Inflation Rate YoY

- US Inflation Rate MoM

- US Core Inflation Rate MoM

- US Core Inflation Rate YoY