When you're new to crypto, there's a lot to figure out. Trades to consider, products to explore, and a whole new vocabulary to get familiar with. Amid all of that, it's easy to overlook one of the simplest things you can do with your balance: put it to work while it's sitting idle.

BloFin Simple Earn lets you earn daily interest on the crypto you're not actively trading. And as a new user, you've received something to make that first step even more rewarding. An APR Booster Voucher has been credited directly to your account, giving you a boosted interest rate on top of your standard returns when you make your first Simple Earn subscription.

This article explains what that means, how it works in practice, and exactly how to apply it.

What is an APR Booster?

An APR Booster is a voucher that temporarily increases your interest rate on a Simple Earn subscription. When you apply it, you earn two layers of returns at the same time: your standard daily interest (the base rate), plus the additional interest from the booster on top.

APR stands for Annual Percentage Rate. It's the annualized rate used to calculate how much you earn on a deposit. A higher APR means more interest earned on the same amount over the same time. The APR Booster adds to that rate for the duration specified on your voucher.

Think of it like a welcome bonus that works as interest rather than cash. Instead of a flat amount deposited to your account, the booster earns you more on whatever you put into Simple Earn.

How the APR Booster works

When you apply an APR Booster Voucher to a Simple Earn subscription, it adds a boosted interest rate on top of your base rate for the number of days specified on the voucher.

Here's what your total earnings look like:

Base interest: Principal × Base APR ÷ 365 × Days subscribed

Boosted interest: Principal × Boosted APR ÷ 365 × Boosted Days

Both accrue simultaneously, and the full amount (base plus boosted interest) is distributed together when your order matures.

A simple example

Say you subscribe 1,000 USDT to a Simple Earn Flexible product with a 5% base APR, and you apply an APR Booster that adds 10% for 7 days.

Your base interest over 7 days: 1,000 × 5% ÷ 365 × 7 ≈ 0.96 USDT

Your boosted interest over 7 days: 1,000 × 10% ÷ 365 × 7 ≈ 1.92 USDT

Total over those 7 days: roughly 2.88 USDT, compared to 0.96 USDT without the booster.

After the 7 boosted days, your base rate continues as normal. The booster simply gives you a higher combined rate during that window.

The earnings cap

Every APR Booster Voucher comes with an earnings cap: the maximum amount of boosted interest it can generate. Once your boosted earnings reach that ceiling, the additional interest stops accruing, even if the boosted period hasn't ended yet. Your base interest continues unaffected.

Before applying your voucher, check the cap on it. If you're planning to subscribe a large amount, it's worth knowing at what point the booster effect cuts off.

A note on product length and boosted days

If your voucher specifies more boosted days than the length of the product you apply it to, the boosted period is automatically capped at the product tenor. For example, if your voucher offers 14 boosted days but you subscribe to a 7-day Fixed product, you'll only receive 7 days of boosted interest. To get the full benefit of the voucher, choose a product with a term at least as long as the boosted days.

Why it's worth using

The APR Booster is a free upgrade to returns you'd already be earning. If you're going to subscribe to Simple Earn anyway (and for most new users holding idle USDT or USDC, it may make sense to), applying the voucher costs you nothing and increases what you earn during the boosted period.

The compounding logic here is straightforward. The more you subscribe and the sooner you do it while the voucher is valid, the more the booster earns you. Leaving it unused means leaving interest on the table.

It's also a good opportunity to experience Simple Earn in a low-risk way. Simple Earn Flexible has no lock-up period, so you can redeem at any time. Applying the booster to a Flexible subscription gives you the benefit of the higher rate while keeping your funds accessible.

What to check on your voucher before applying

Your APR Booster Voucher will show:

- Applicable products: which Simple Earn products the booster can be used on. Make sure the product you're subscribing to is on that list.

- Boosted APR: the additional percentage rate you'll earn on top of your base rate during the boosted period.

- Earnings cap: the maximum boosted interest the voucher will generate. Once this is reached, the boost stops.

- Validity period: the window within which you must apply the voucher. After it expires, it can no longer be used.

Take a moment to read these before subscribing. Applying the voucher to a product that suits your balance and the boosted period will get you the most out of it.

How to apply your APR Booster

The APR Booster voucher is given to all new BloFin users, so if you’ve yet to create an account, do so before following the steps below. If you require any assistance with creating an account, you can check out our sign-up guide.

Step 1: Log in to your BloFin account and hover your cursor over the Earn tab in the navigation bar. Then, select Simple Earn.

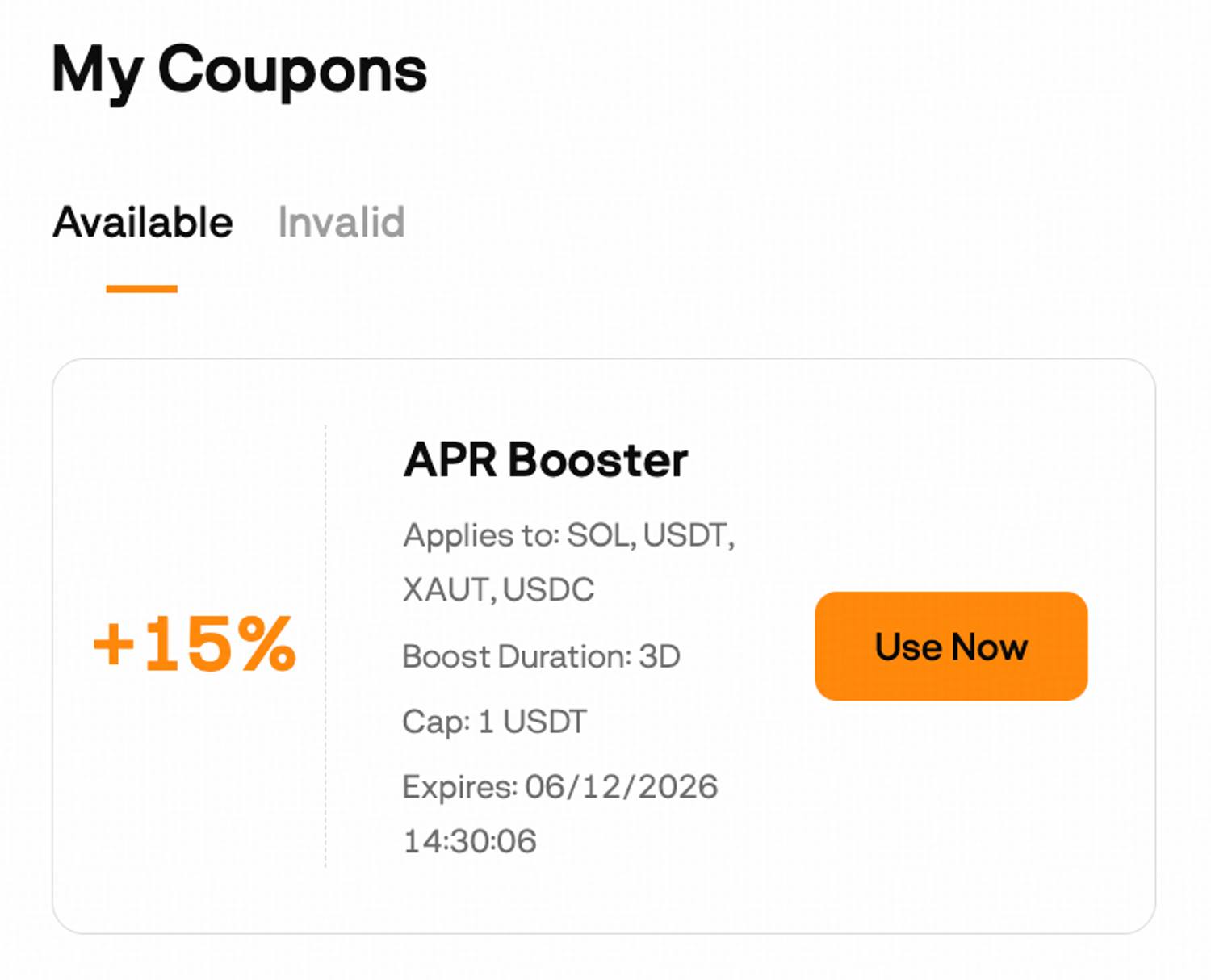

Step 2: On the Simple Earn page, click View My Coupons.

Alternatively, you can also view your coupons by hovering your cursor over the avatar icon and clicking My Coupons.

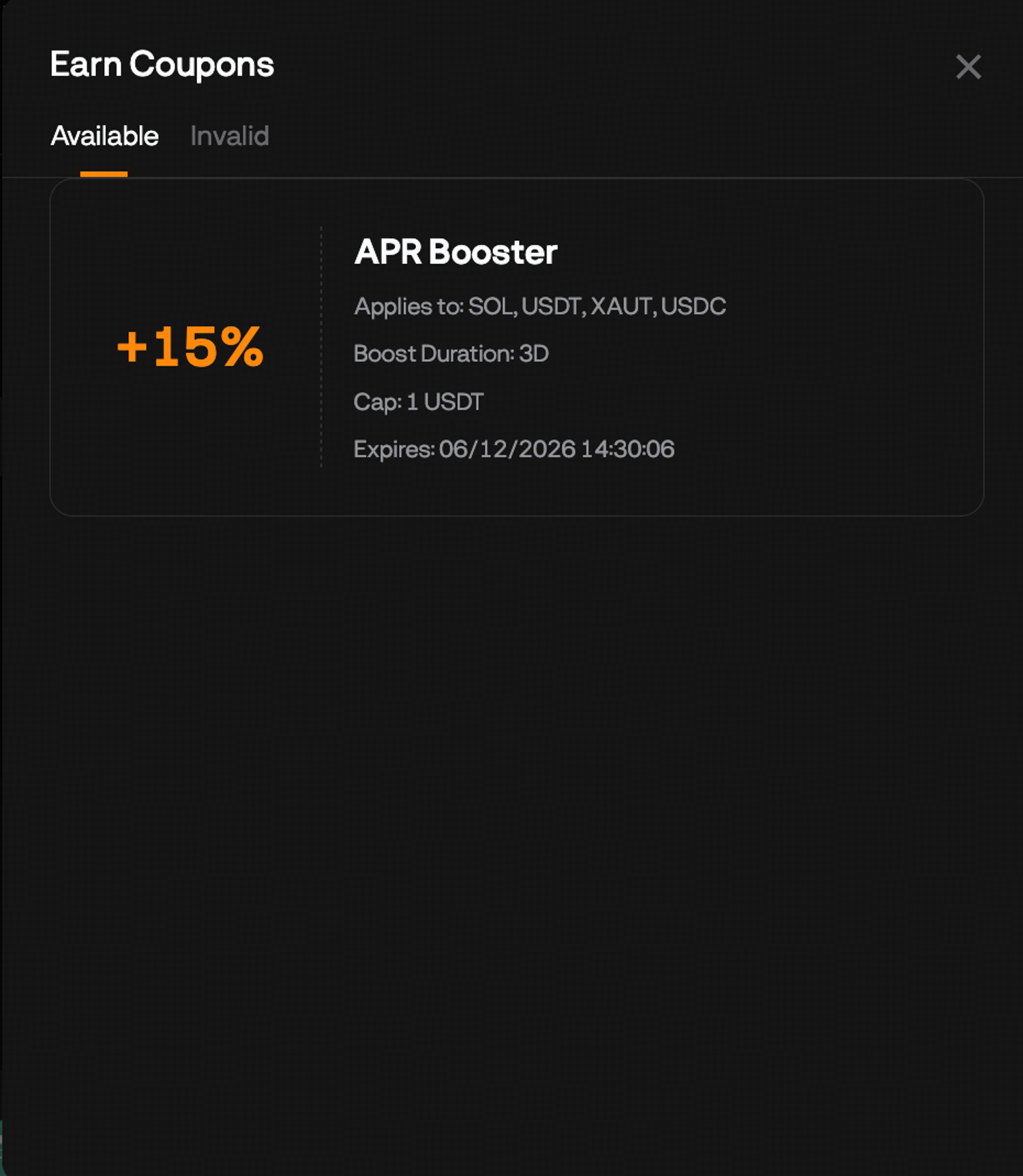

Both of these open your coupon wallet, where you can see available and expired vouchers. Your APR Booster Voucher will appear under Available.

If you’re viewing the coupon from My Coupons, click Use Now and it will direct you to the Simple Earn page.

Please note that the APR Booster is not available on all Simple Earn tokens. Only products listed on this screen are eligible, so check which tokens and terms are available before deciding where to apply it. In this example, the APR Booster only applies to SOL, USDT, XAUT, and USDC.

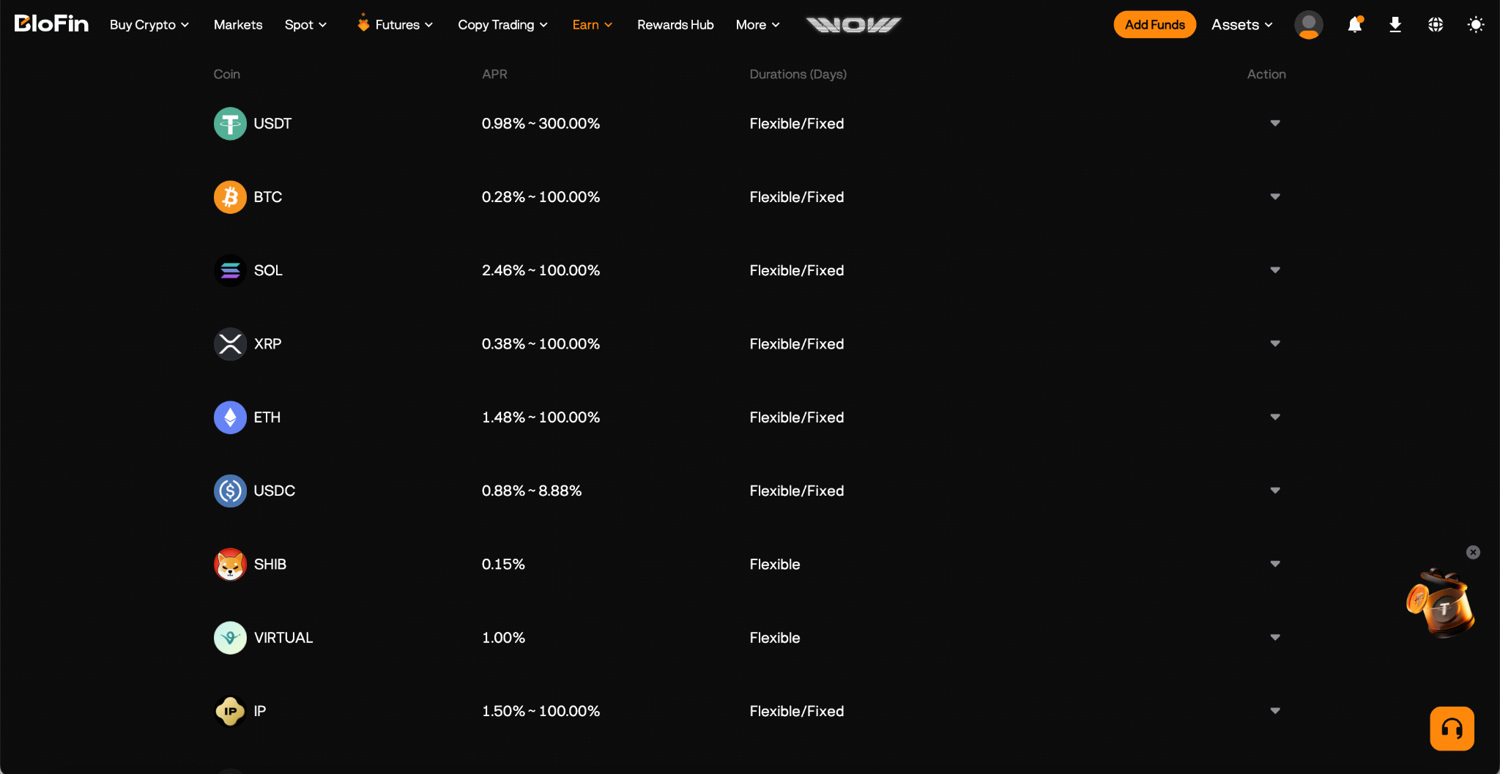

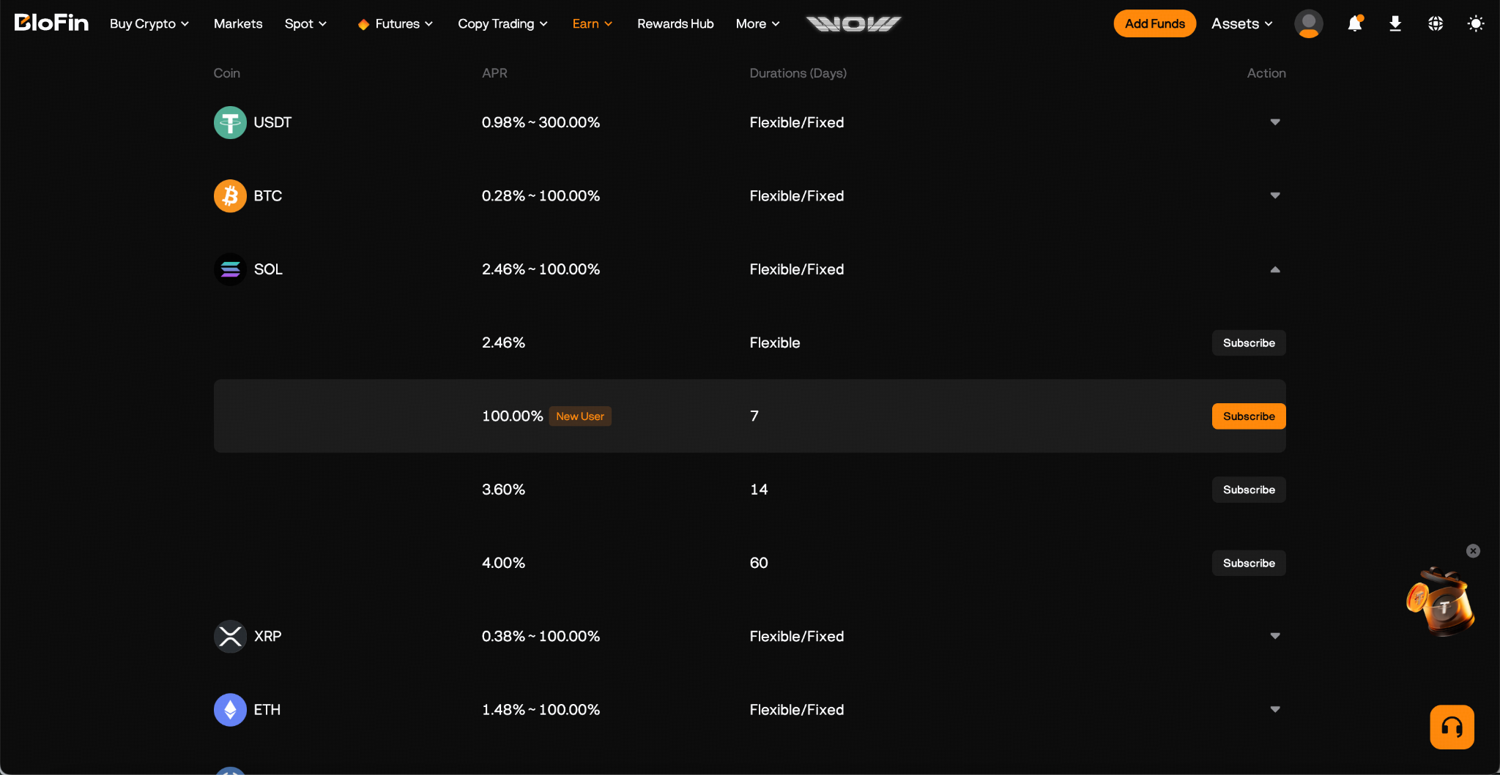

Step 3: Browse the eligible products and select the one that suits your needs. Consider the term length relative to your voucher's boosted days (a longer term gets you the full boost), the base APR on offer, and whether you want the flexibility to redeem early. Once you've decided, click Subscribe.

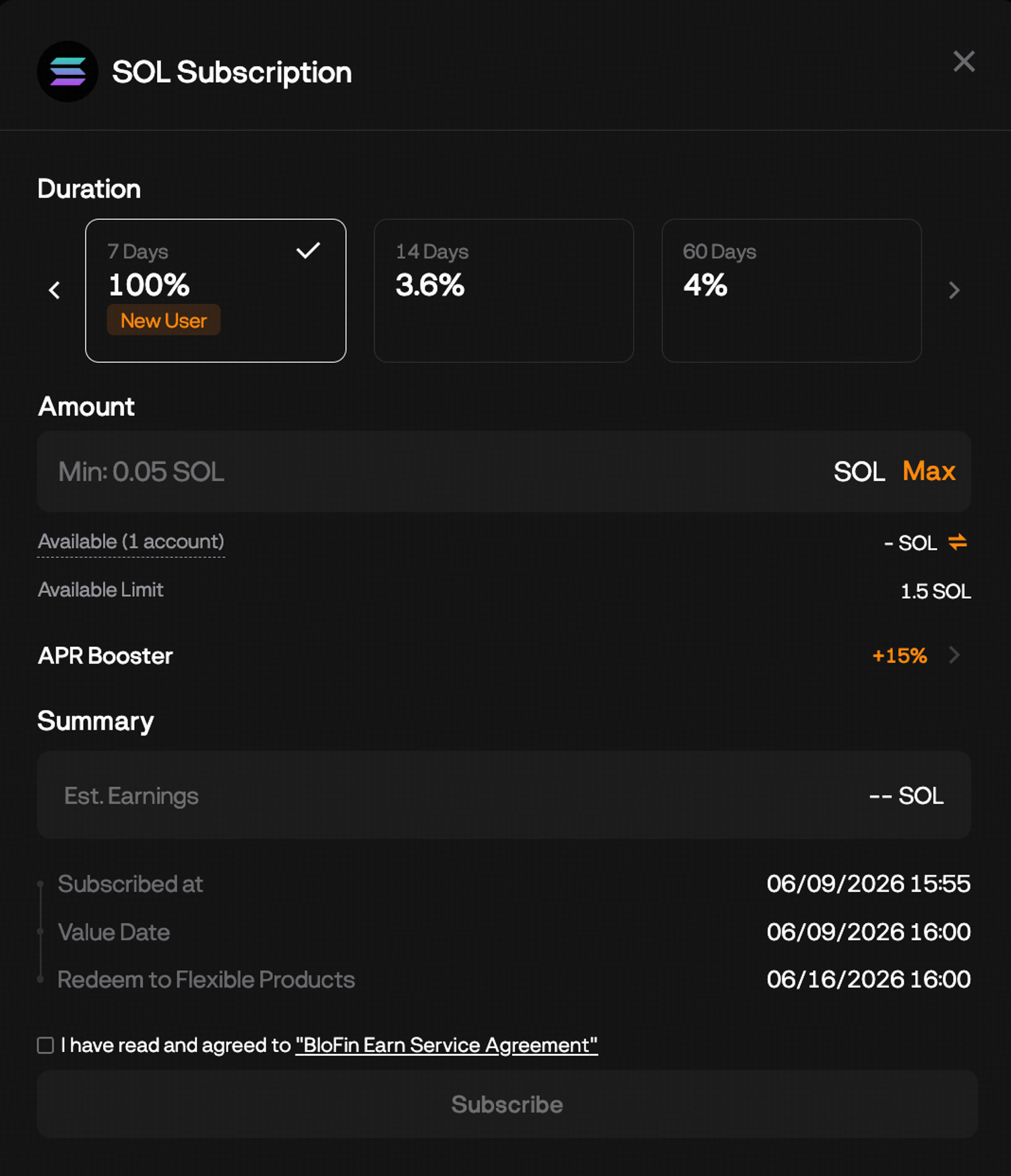

Step 4: On the subscription screen, check that the APR Booster is shown as applied before proceeding. You should see both your base rate and the boosted rate reflected.

Step 5: Input the amount you would like to subscribe. Keep the earnings cap in mind here. If your voucher has a cap, subscribing a very large amount doesn't increase the boosted earnings beyond that ceiling. The cap is the limit regardless of principal size.

Step 6: Review the details one final time, then click Confirm. Your subscription is now active. Interest (base plus boosted) will begin accruing from the following day and will be distributed to your Earn Account at maturity.

A few things to keep in mind

One-time use. Each APR Booster Voucher can only be applied once. Once you've used it on a subscription, it cannot be reapplied to a different order.

One voucher per order. You can only apply one APR Booster Voucher per subscription. If you have multiple vouchers, each one will need to be applied to a separate order.

It doesn't affect your principal. The booster only changes how much interest you earn. Your subscribed amount is untouched and returned to you at maturity alongside all accrued interest.

Flexible products remain redeemable. If you apply your booster to a Flexible product and redeem before the boosted period ends, boosted interest stops accruing from the redemption request date. No interest (base or boosted) accrues on the redemption day itself.

Frequently asked questions

Where is my APR Booster Voucher?

It's in your coupon wallet. Go to Earn > Simple Earn > View My Coupons and look under Available. Alternatively, you can hover your cursor over the avatar icon and click My Coupons.

Do I have to use the APR Booster right now?

No, but check the validity period on your voucher. Once it expires, it can no longer be applied. Using it sooner gives you more time to benefit from the boosted rate.

What is an earnings cap and why does it matter?

The earnings cap is the maximum amount of boosted interest your voucher will generate. If you subscribe a very large amount, your boosted interest will stop accruing once it hits the cap, even if the boosted period is still running. Knowing the cap helps you decide how much to subscribe.

Can I apply the APR Booster to any Simple Earn product?

Only to eligible products. Your voucher will specify which products it applies to. The voucher is applied automatically when you select an eligible product.

What happens if my product term is shorter than my boosted days?

The boosted period is capped at the product tenor. If your voucher offers 14 boosted days but you subscribe to a 7-day Fixed product, you'll receive 7 days of boosted interest. To get the full boosted days, choose a product with a term at least as long.

When is my interest paid out?

For Flexible products, base interest accrues daily. For Fixed products, both base and boosted interest are distributed together when the product matures. Either way, the boosted and base earnings are paid out as a combined amount.

Does using the APR Booster lock up my funds?

The APR Booster doesn't change the terms of the product you apply it to. If you apply it to a Flexible product, your funds remain redeemable at any time. If you apply it to a Fixed product, your funds are locked for the term as usual.

What if I forget to apply the voucher before subscribing?

Unfortunately, vouchers cannot be applied to existing subscriptions. You'll need to start a new subscription and apply the voucher at the time of confirming.

Disclaimer: This content is for educational purposes only and does not constitute financial, investment, legal, or tax advice. Crypto assets are highly volatile and carry significant risk of loss. Always verify local regulations and consult a qualified professional before making financial decisions.