Does Anyone Still Care About Inflation?

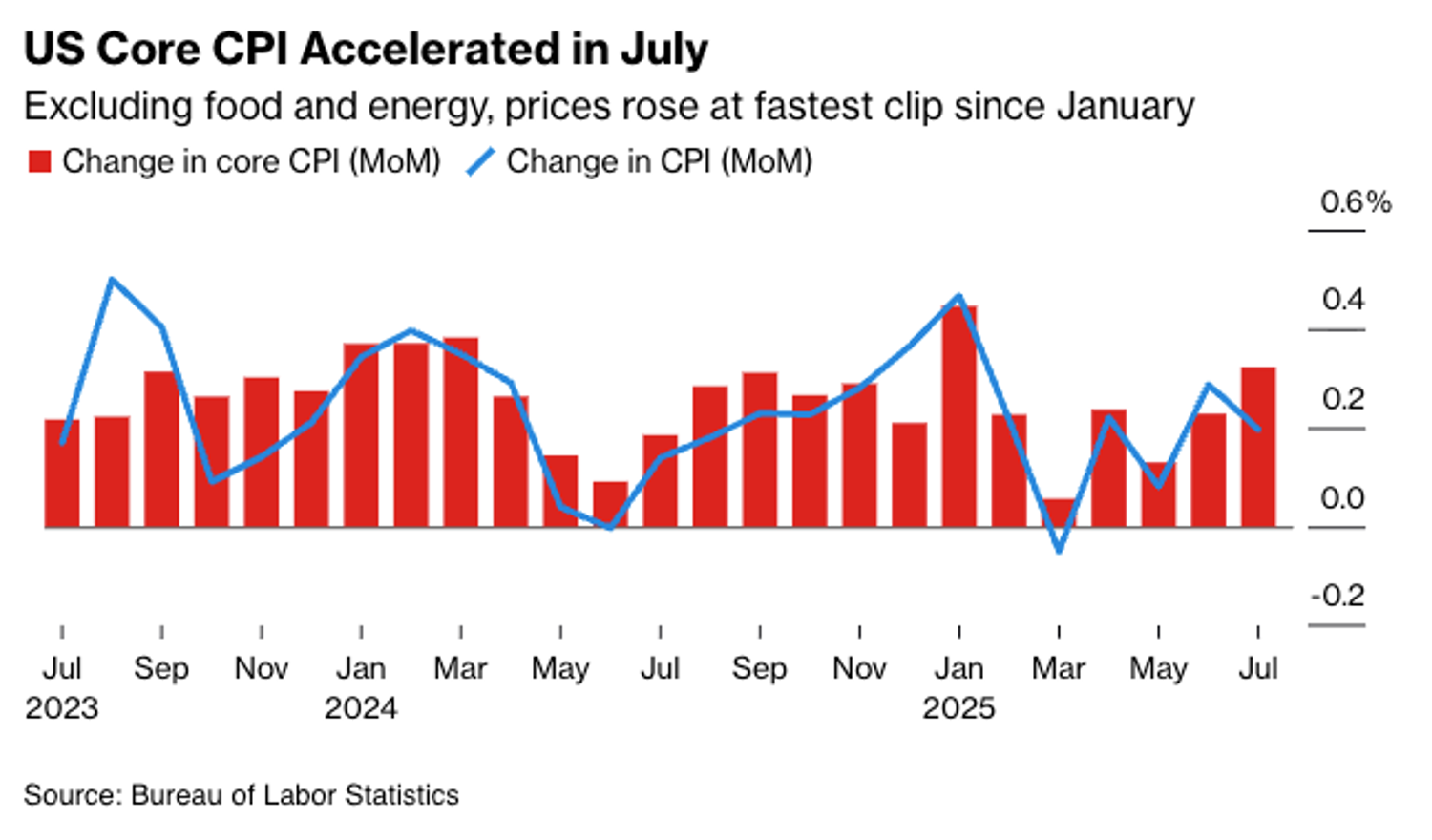

Admittedly, Tuesday's inflation data wasn't particularly optimistic. While headline inflation came in slightly below expectations, core inflation continued to rise (primarily driven by the services sector), reaching its highest point since the beginning of the year. The Federal Reserve typically prioritises core inflation data; in the past, such figures have often led to a contraction in market risk appetite.

Source: Bloomberg

However, the current situation is different: investors' sensitivity to inflation appears to have significantly decreased. With Powell's influence on the Fed weakened, investors are increasingly betting that Trump's influence on the Fed will force the central bank to compromise, and the significantly downward revision of non-farm payroll data will provide justification for such a "decent compromise."

Of course, several Fed officials, such as Bostic, still cling to their previous views based on the data, and these officials still hold considerable influence, making the rate cuts after September still highly uncertain. However, many investors believe that, to some extent, whether or not to cut rates is no longer "a question"; the Treasury Department, not the Fed, is assuming the new role of "liquidity steward" under the Trump administration.

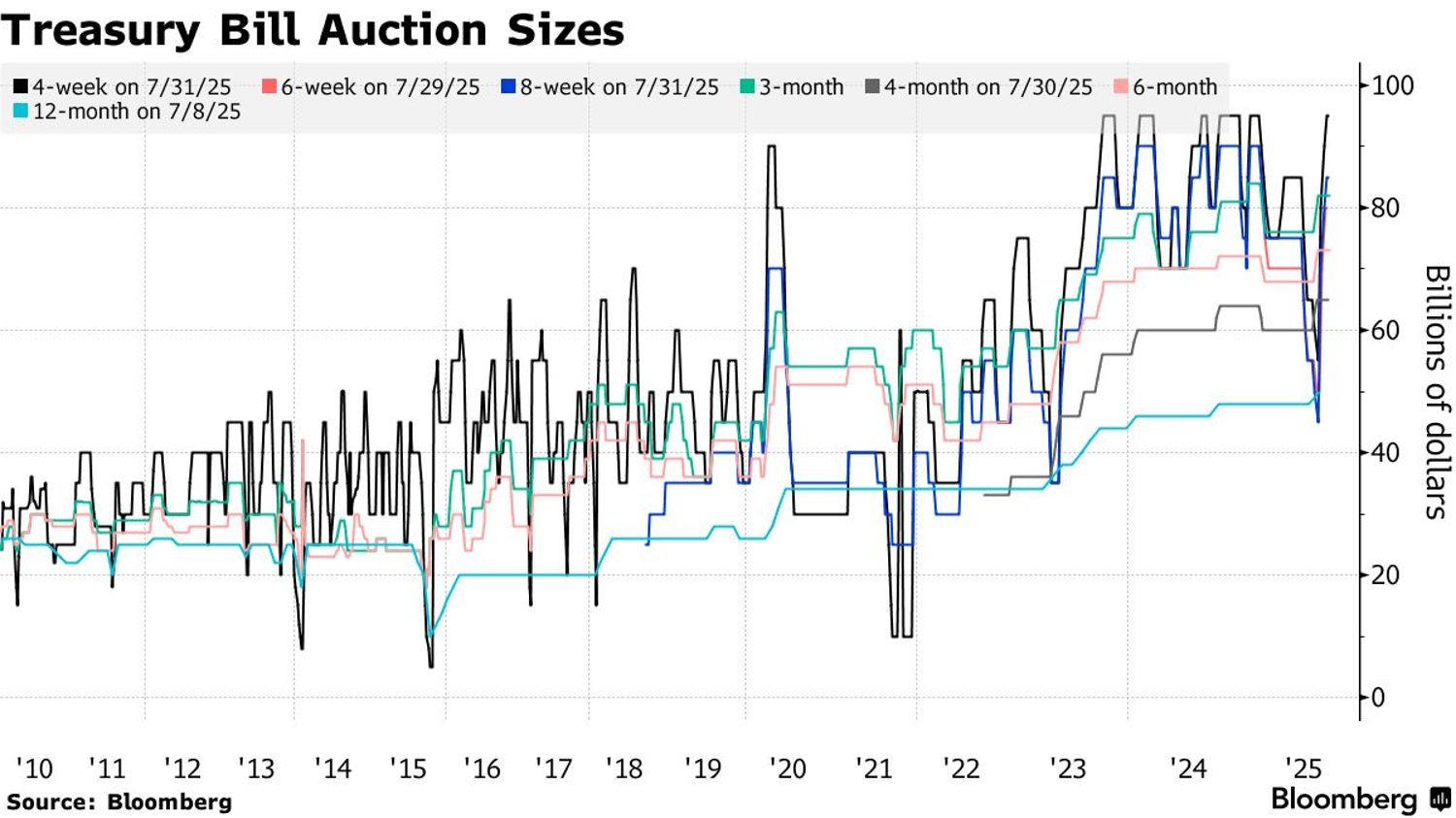

The OBBBA is creating a massive amount of debt, and under Bessent, the Treasury has significantly increased its T-bills issuance; last week, the Treasury auctioned $100 billion in four-week bills, setting a new record. But this is just the beginning: with tax cuts and increased government spending, the growing fiscal deficit will only increase demand for T-bills. The Treasury has stated that it will rely more heavily on T-bills to cover spending shortfalls until at least 2026, and expects to increase T-bills auctions further in October.

Source: ustreasuryyieldcurve.com

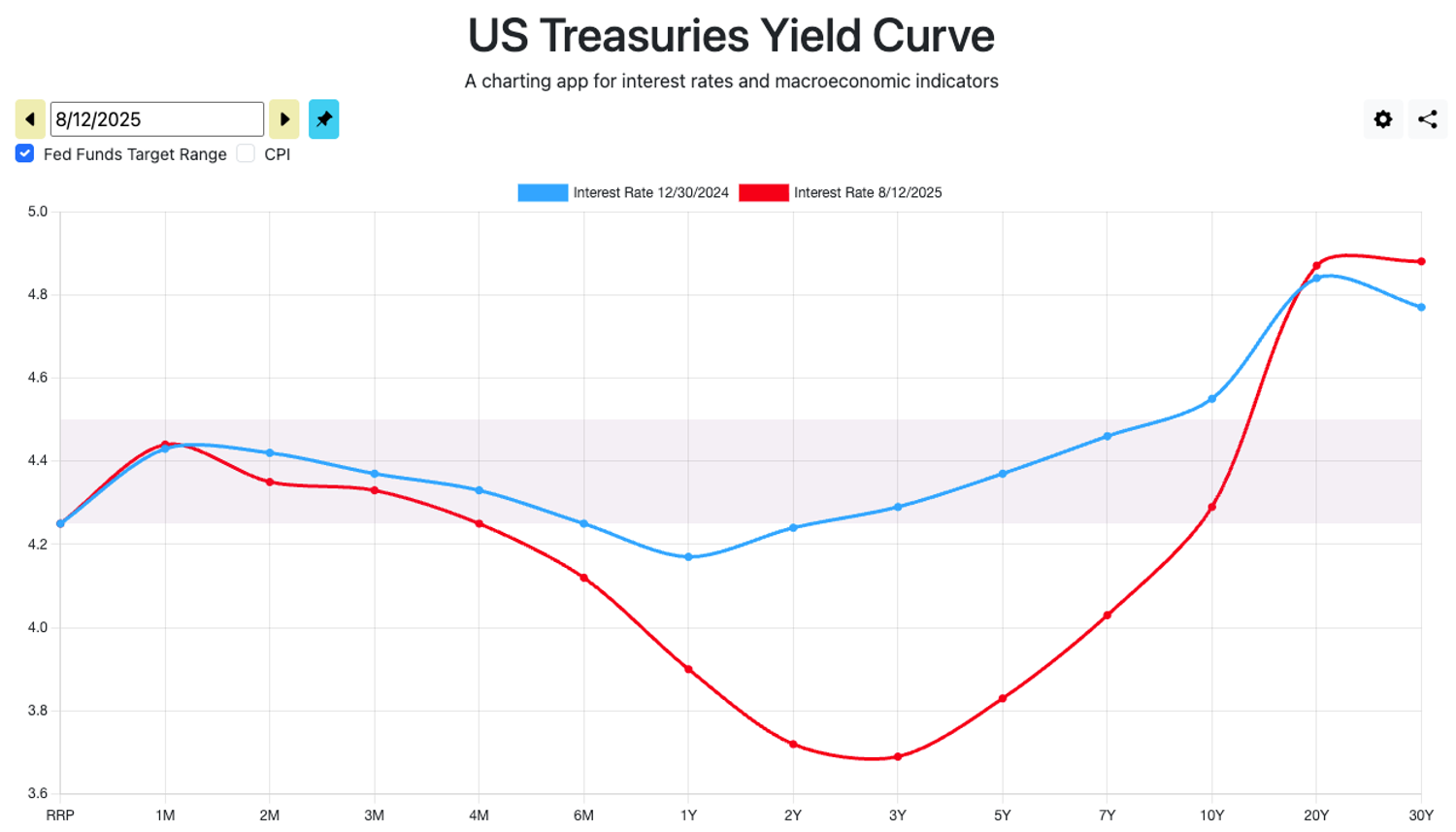

This situation has created a "de facto rate cut": even though the federal funds rate remains in the 4.25%-4.5% range, the Treasury's record T-bills auctions and issuance have pushed short-term yields below the Fed rate. Even if Trump's attempt to rein in the Fed fails a year from now and rate cuts remain slow, the Treasury can still use large-scale T-bills auctions to inject liquidity into the market and weaken or even "partially neutralise" the Fed's role in monetary policy.

Fragile "Treasury QE"

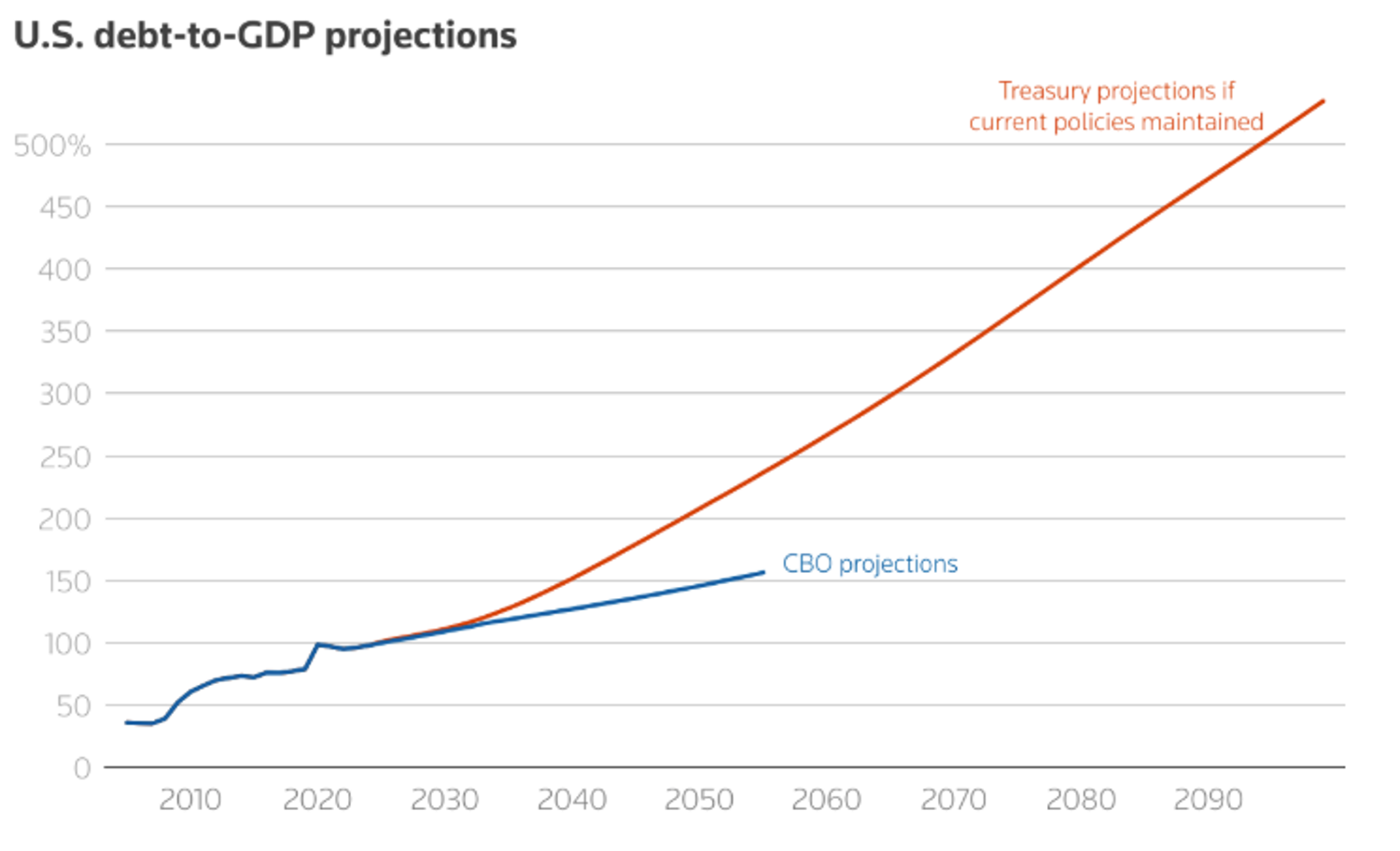

The Treasury's attempt to increase its influence on liquidity is not without cost. Massive government bond issuance will continue to push up the deficit, something that tariffs and economic growth will struggle to offset in the future. Consequently, as the deficit grows, investors, concerned about debt risk, will seek higher risk premiums as compensation, pushing up real yields on government bonds and increasing repayment pressure. Since the beginning of this year, T-bond yields have not fallen significantly, and investor concerns are already being reflected in the bond market.

Source: Reuters

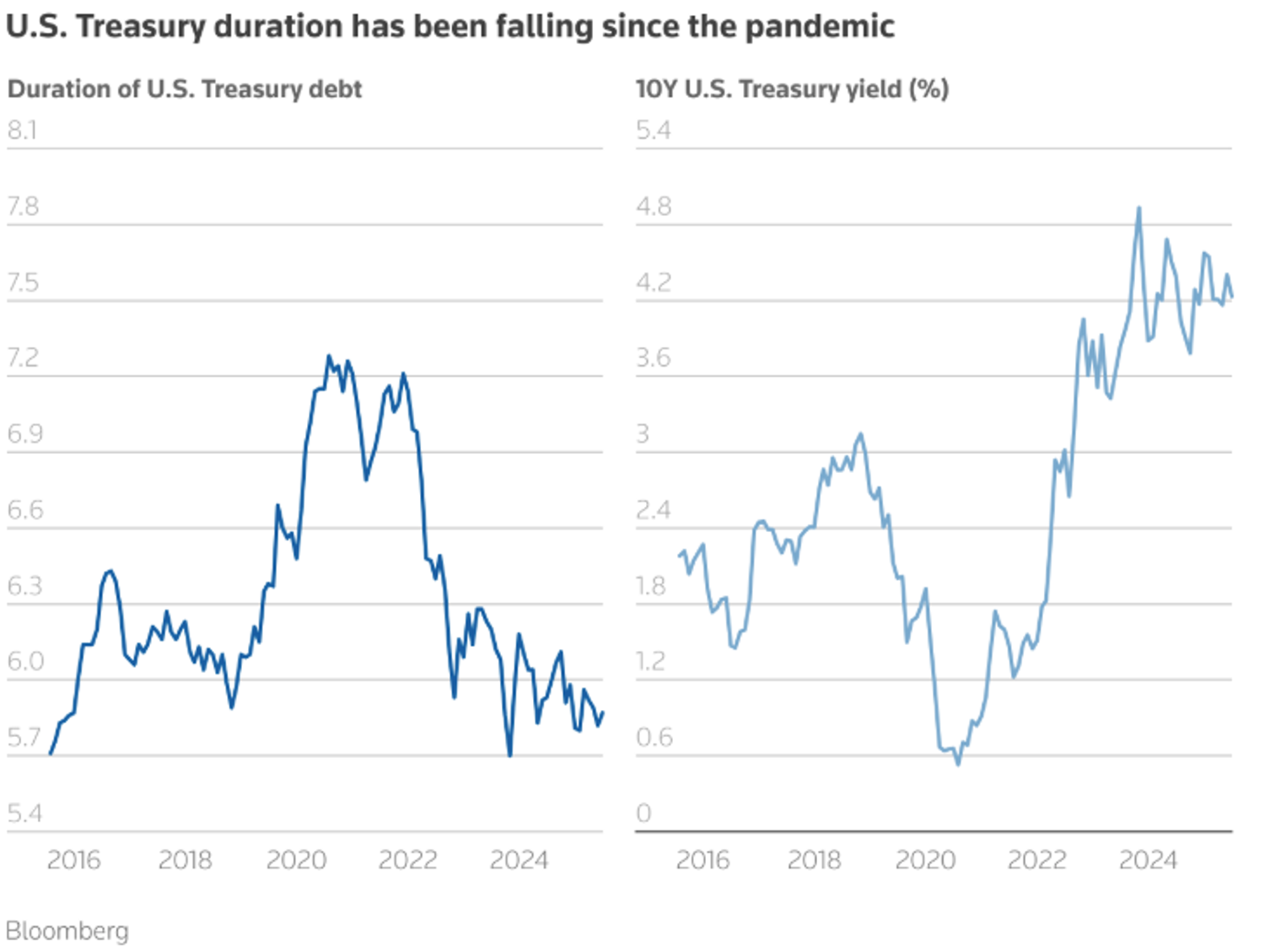

Faced with this situation, Bessent's Treasury chose to significantly increase the proportion of T-bills in total financing and reduce the proportion of bonds of other maturities. This has led to a further decline in government bonds' average duration, which had fallen sharply since 2020. While the current average duration is still higher than at some point around 2016, the current debt level is no longer comparable to a decade ago.

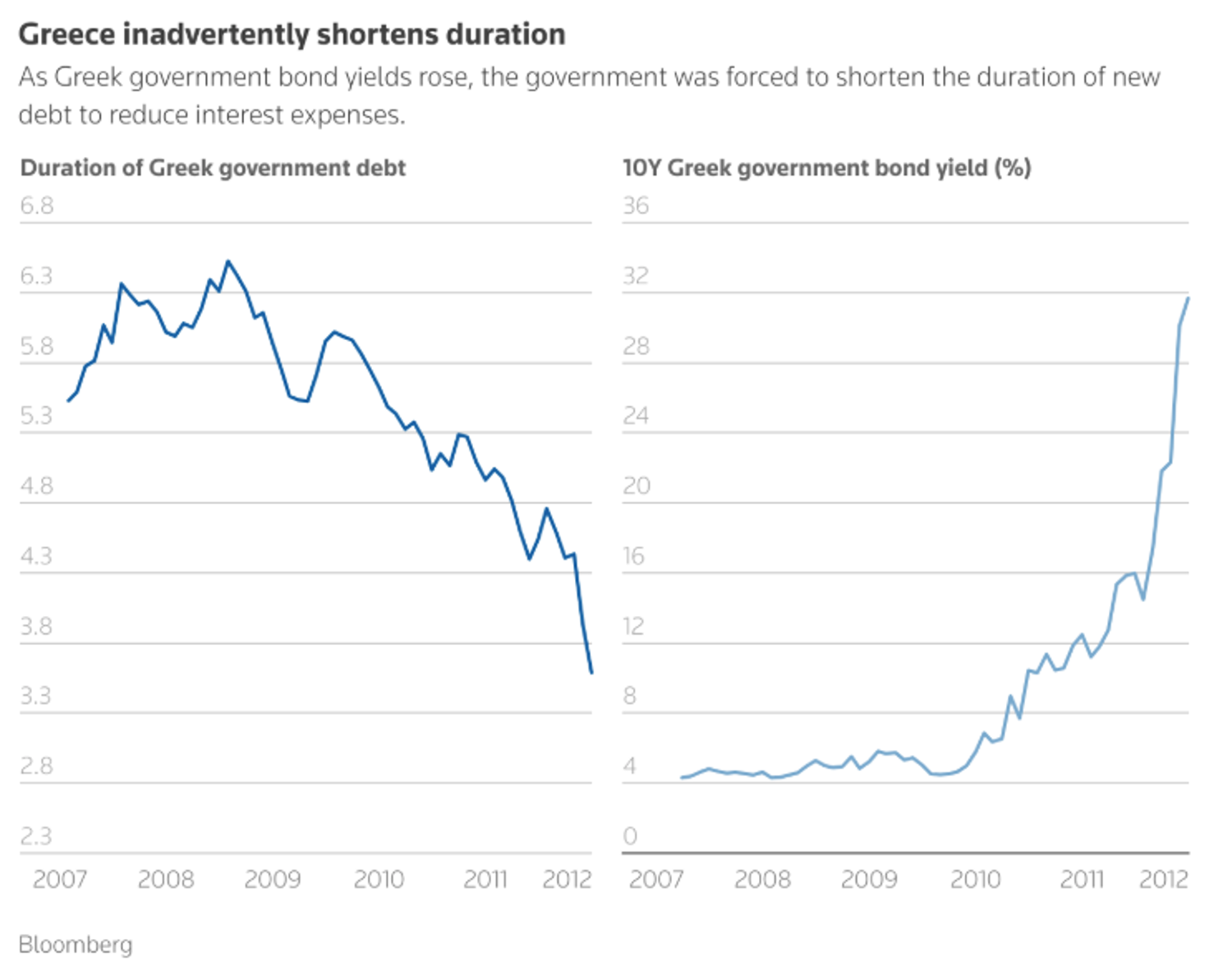

Historically, a decline in the average duration of government bonds has often signalled a government's growing debt repayment capacity: the average duration of Greek bonds fell sharply around the 2009 Eurozone debt crisis. Admittedly, the United States is not Greece; it still possesses one of the world's most resilient economies. However, once a reliance on short-term bonds develops, government cash flow volatility will increase, further fueling investor scepticism about the government's ability to repay its debts and leading to a demand for higher risk premiums. The Treasury, in turn, is forced to finance itself through shorter-term bonds to reduce interest expenses—a vicious debt cycle.

Source: Reuters, Bloomberg

In fact, the government's reliance on short-term bonds not only amplifies government cash flow volatility but also fuels potential volatility in the capital market. Banks are among the first to be impacted: many banks' investments are concentrated in long-term government bonds and are the primary counterparties for T-bills. Due to the mismatch between interest rates and short-term bond yields, banks tend to short T-bills to hedge their own interest expenses and go long on long-term government bonds for investment. However, as long-term government bond yields remain high due to debt risk, and the Treasury intentionally shifts demand from long-term to short-term bonds to reduce government interest expenses, banks suffer losses on both short-term and long-term bond trading, which ultimately forces banks' lending and financing strategies to favour the short term over the long term to align with treasury curve, driving up long-term financing and investment costs.

Similarly, for traders, "investment"-based trading will face significant costs associated with long-term financing, and the expected availability of funding will be further limited due to the decline in long-term debt and rising yields. In contrast, "speculation"-based trading is less costly and more profitable due to ample short-term liquidity.

Source: Reuters, Bloomberg

However, this situation suggests a "fragile bull market": due to sovereign credit risk, the long-term issuance of T-bills is questionable. Furthermore, since the funds driving the stock and crypto markets primarily come from short-term speculative funds, rather than long-term investment funds, traders generally tend to use leverage to maximise returns. If T-bills yields rise significantly or issuance declines, the liquidity in the capital market will dramatically fluctuate, leading to a chain reaction of liquidation or even a crash.

The above is one reason why Trump wants to "force" the Federal Reserve to ignore inflation and slash interest rates: If the Fed cooperates, the "fragile bull market" driven by short-term speculation can at least continue for a while before inflation spirals out of control again. However, if the Fed does not cooperate, the market will experience significant fluctuations due to changes in short-term liquidity, and a crash is imminent.

Economic Calendar of This Week

Tuesday 06:00

- UK Unemployment Rate

Tuesday 12:30

- US Inflation Rate YoY

- US Inflation Rate MoM

- US Core Inflation Rate YoY

- US Core Inflation Rate MoM

Thursday 06:00

- UK GDP MoM

- UK GDP Growth Rate QoQ Prel

- UK GDP Growth Rate YoY Prel

Thursday 12:30

- US PPI MoM

Friday 12:30

- US Retail Sales MoM

- US Michigan Consumer Sentiment Prel