"Confidence Lost"

In the decades leading up to 2020, the role of Treasury bonds in investment portfolios continued to grow. Whether it was the well-known "60-40 portfolio" or the bond performance during bubble bursts and financial crises, Treasury bonds from major countries often served as a "portfolio stabiliser." The default risk of major countries was generally "near zero," and the guaranteed returns offered by Treasury bonds made them a high-quality collateral, nearly on par with cash and widely recognised in global markets.

However, in financial markets, nothing is static: the outbreak of the European debt crisis demonstrated that bonds from developed countries are not necessarily as safe as advertised. Now, as countries like the United States and Germany continue to expand their debt, even raising their debt ceilings without limit (see the OBBBA Act), investors who had previously been confident in Treasury bonds, whether retail investors or central banks, are beginning to question their "sustainable" nature.

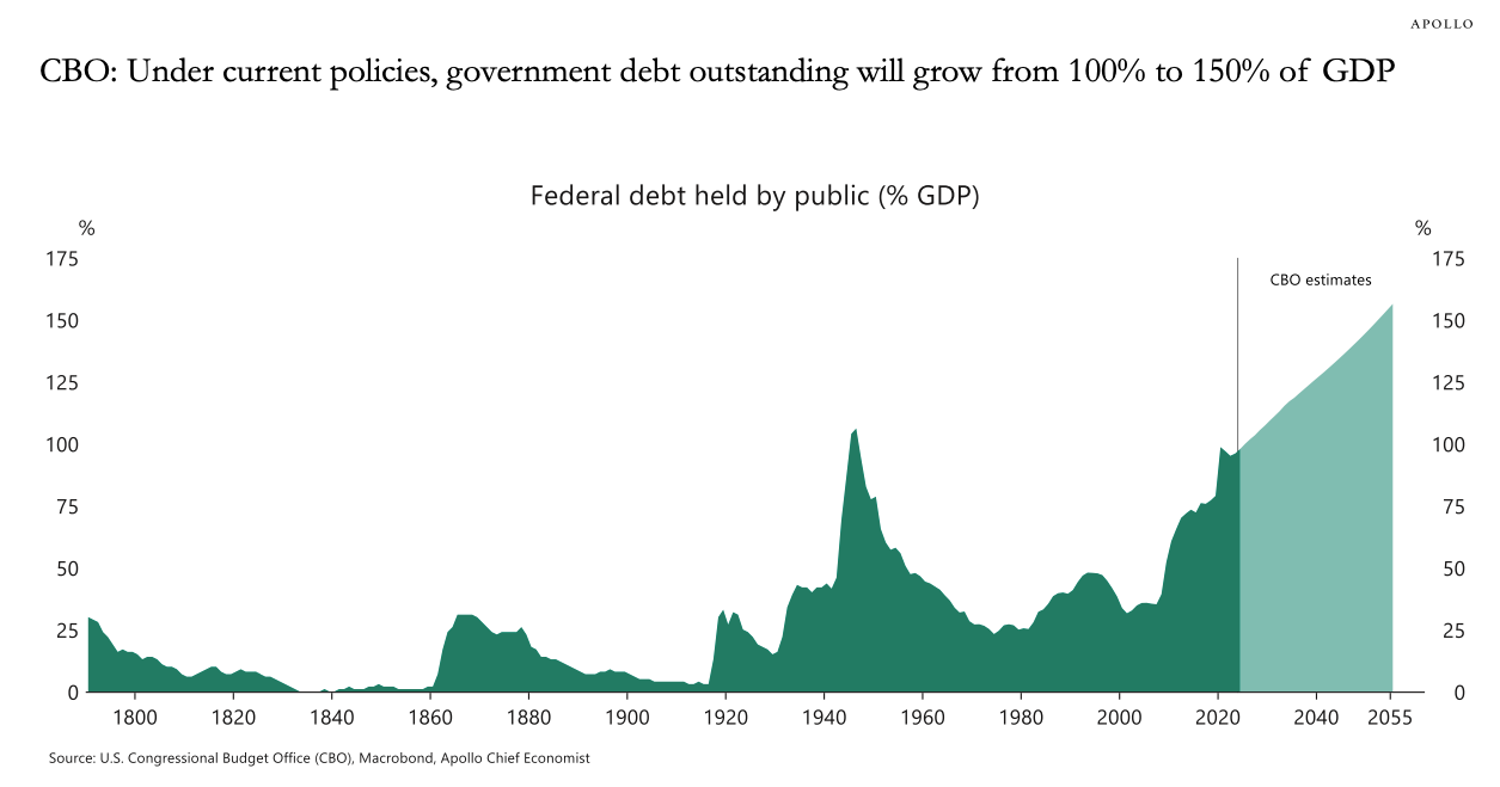

Since 2020, the economic recession and shutdowns caused by the COVID-19 pandemic have prompted governments worldwide to issue massive amounts of debt to cope. Following the pandemic's end, investment in national security, defence, and infrastructure, driven by factors such as the Russia-Ukraine war, further boosted demand for debt and its issuance. Investors are beginning to realise that debt-to-GDP ratios in major countries like the United States could quickly exceed 100%. In this scenario, even the United States' long-term debt repayment capacity is questionable, let alone other countries with smaller economies.

Clearly, investors are unprepared for the possibility of a major Treasury bond default. The 1998 Russian Treasury bond default devastated a series of leading hedge funds and institutions like LTCM. However, investors still had the option of withdrawing liquidity into low-risk Treasury bonds like US and German bonds. However, once even these "low-risk Treasury bonds" began to face potential credit crises, no one knew which interest-bearing assets would be safe. As a result, the price of gold has risen 71.74% since 2024, while the price of Bitcoin has risen 158%.

Source: Tradingview

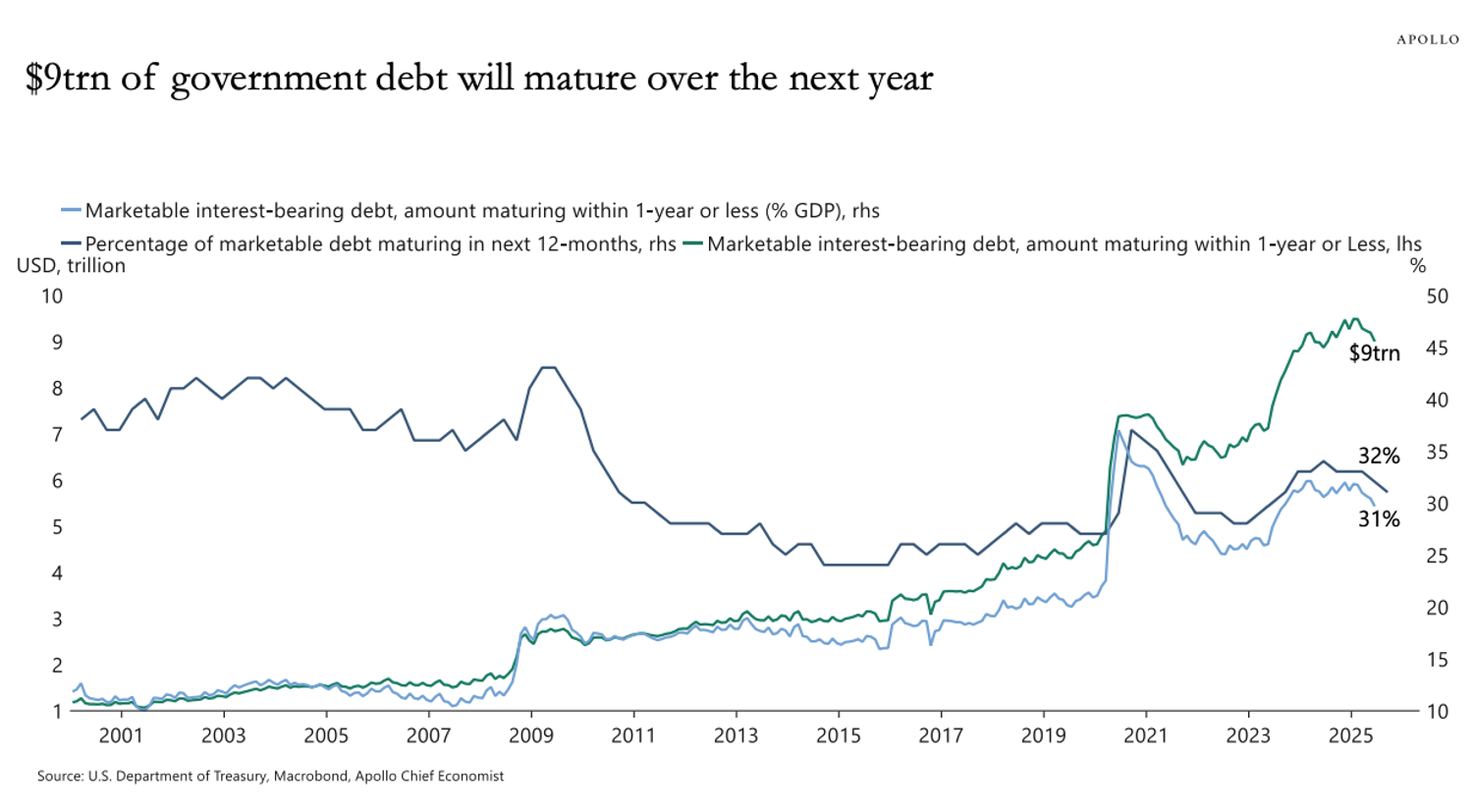

Critics argue that this situation is a step backward: Treasury bonds are interest-bearing assets, while gold and Bitcoin are not, and that investors turning to gold and Bitcoin is "unwise." However, with the US already facing $9 trillion in outstanding debt over the next year, the yield from Treasury bonds doesn't necessarily offset potential default risk. Strictly speaking, gold and Bitcoin are immune to default, but Treasury bonds are not.

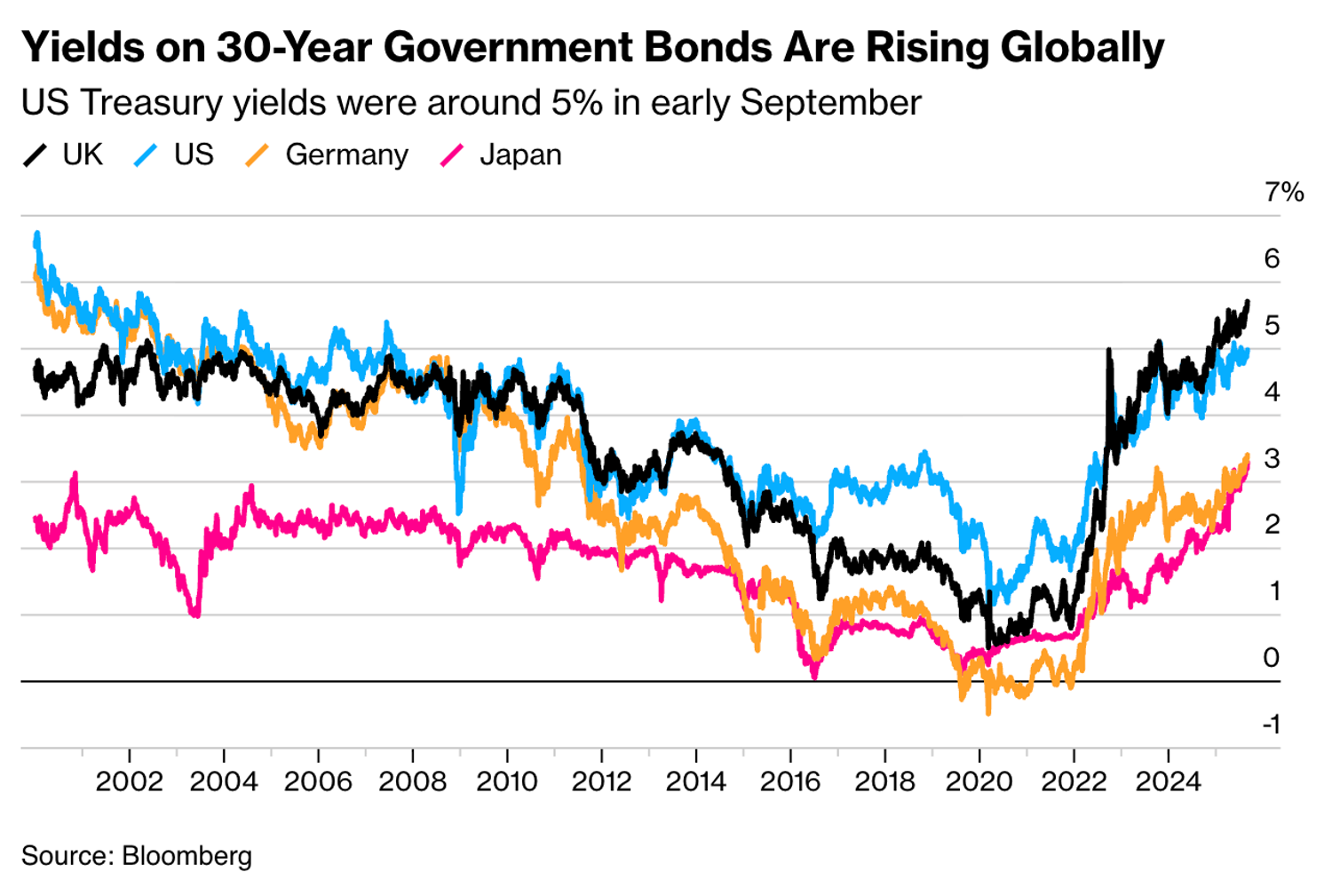

In reality, the risks associated with Treasury bonds extend beyond default risk. Long-term Treasury bonds are often considered more than just default risk, including inflation and central bank independence. Investors holding European Treasury bonds typically focus solely on deficits and the burden of a higher debt ceiling, but for those holding US Treasury bonds, concerns about reflation and the independence of the Federal Reserve may be key drivers in seeking higher yields. Regardless of the reasons, the result is the same: long-term Treasury bond yields in Europe, Japan, and the US have reached their highest levels since 2002, making it appear that Treasury bonds are no longer the "safe haven" they once were.

Debt Isn’t the Only Thing That Will Be Affected...

Rising long-term bond rates go beyond simply increasing future government interest payments. Banks use Treasury bonds to lock in base yields and profit through term structure allocations. Treasury bond yields serve as a crucial anchor for both short-term and long-term borrowing. Rising long-term government bond yields mean the "risk premium" (a measure of the difference between the expected returns of risky assets and those of risk-free assets) is likely to narrow significantly, especially in a high-interest-rate environment. Once the gap between the expected returns of risk-free and risky assets fails to widen significantly, long-term investment becomes irrational, regardless of leverage. Compared to assets like stocks and cryptocurrencies, returns based on government bonds are clearly "relatively safe."

At the same time, due to excessively high long-term borrowing rates, investors often turn to short-term borrowing or financing with short-term Treasury bonds, such as through T-bills. In this scenario, funds supporting risky asset markets must be repeatedly rolled over, significantly reducing the proportion of funds remaining in long-term holdings. This has two consequences:

Since liquidity primarily comes from short-term funds, the pursuit of the highest possible returns in a short period of time (i.e., "speculation") becomes the primary market driver, even leading to short-term counter-trend movements when fundamentals haven't significantly improved, thereby increasing market uncertainty and potential volatility.

Repeated rollovers lead to rapid fluctuations in market liquidity, resulting in repeated sell-offs and buy-backs of risky assets. Over the long term, the risk of rapid short-term liquidity fluctuations will be further incorporated into market pricing and trading risk control systems, making rapid price increases and declines more common, resulting in higher realised volatility—a factor that institutional investors are highly concerned about and keen to avoid.

In summary, it's not surprising that investors (especially institutional investors) are turning to gold. Given the cross-national and systemic nature of the rise in long-term bond yields, increasing gold exposure is a logical and reasonable choice, whether driven by a desire for a safe haven against additional stock market volatility or concerns about long-term bond defaults and macroeconomic risks.

Besides Gold, What Other Options Are There?

With the prospect of rising long-term bond yields, the role of government bonds as collateral has been significantly negatively impacted, particularly from the perspective of cross-border financing. Consequently, demand for "alternative collateral" will dramatically increase.

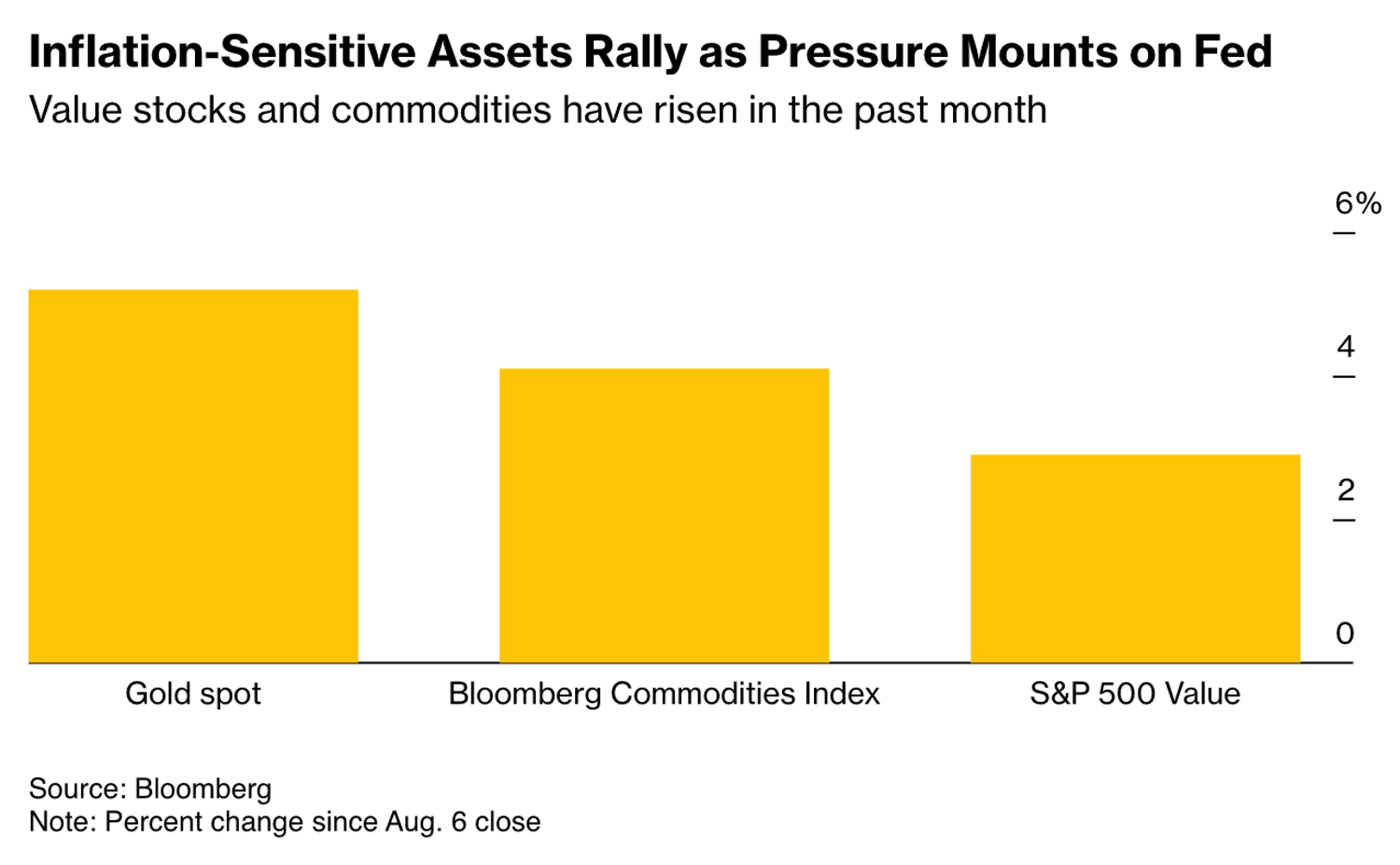

Before the invention of bonds, commodities were a natural collateral. Even today, commodities remain an option in the collateral pool. The increased potential risk of government bonds has led people to remember the old era of the Renaissance. Physical commodities are excellent collateral for offshore financing, and rising demand for collateral will also drive commodity prices higher. In fact, over the past month, commodities have outperformed S&P 500 value stocks and are second only to spot gold.

Can gold itself be replaced in an investment portfolio? Bitcoin may be a viable option. Compared to gold, Bitcoin plays a similar role in a portfolio and offers better liquidity (although also higher volatility). IBIT's average daily trading volume over the past three months has reached 4.7 times that of GLD. Furthermore, the Bitcoin derivatives market is relatively large and developed, meaning that the implied expected returns of Bitcoin itself can be realised through carry trades rather than long-term holding, something that is somewhat difficult to achieve with gold.

Therefore, it might be worth considering increasing exposure to commodities and gold in your portfolio. For risk-averse investors, holding Bitcoin carry positions brings a significantly higher, nearly risk-free return than the "risk-free return" of bonds. At the same time, for risk-seekers, buying Bitcoin directly may offer considerable returns over the longer term. However, it must be acknowledged that holding delta from underlying assets with relatively high volatility is a risky move. Good luck.