The Unfamiliar "Long-term Interest Rate Goal"

As the dust settles on the September FOMC meeting's consensus on rate reductions, the Trump administration has turned its attention to the Federal Reserve's obscure "third mandate" — "moderate long-term interest rates." The newly nominated Fed Governor Miran ignited controversy by invoking this little-known clause during a Congressional hearing, fuelling speculation that the White House seeks to manipulate long-term bond yields.

This move is widely perceived as heightened pressure on the Fed's independence, with the intention of facilitating housing market stimulus and debt financing. Miran's remarks not only unearthed a long-overlooked provision in the Fed's charter but propelled "moderate long-term rates" to the forefront of monetary policy, challenging decades of Wall Street's investment principles.

Hitherto, markets have focused on the Fed's "dual mandate" — price stability and maximum employment. The sudden emergence of this "third mandate" has caught traders unawares, sparking intense discussion in bond markets. Andrew Brenner, Vice Chairman at Natalliance Securities, noted in a September 5 report that the White House "unearthed this ambiguous clause, providing a legal basis for intervening in long-term rates," a development that, while not yet dominating trades, warrants serious investor consideration.

Yet, consensus within the Fed remains elusive. Powell, Cook, and Jefferson continue to prioritise persistent inflation, cautious of premature easing reigniting stagflation risks. Philadelphia Fed President Harker insists the 2% inflation target is inviolable; Dallas Fed President Logan cautions that weak labour market data does not justify aggressive rate reductions. By contrast, Miran leads a growing "Trump-aligned" faction of three governors advocating for rates to fall swiftly below 3%, clashing with the September dot plot's conservative faction, which supports maintaining rates above 3% until 2027.

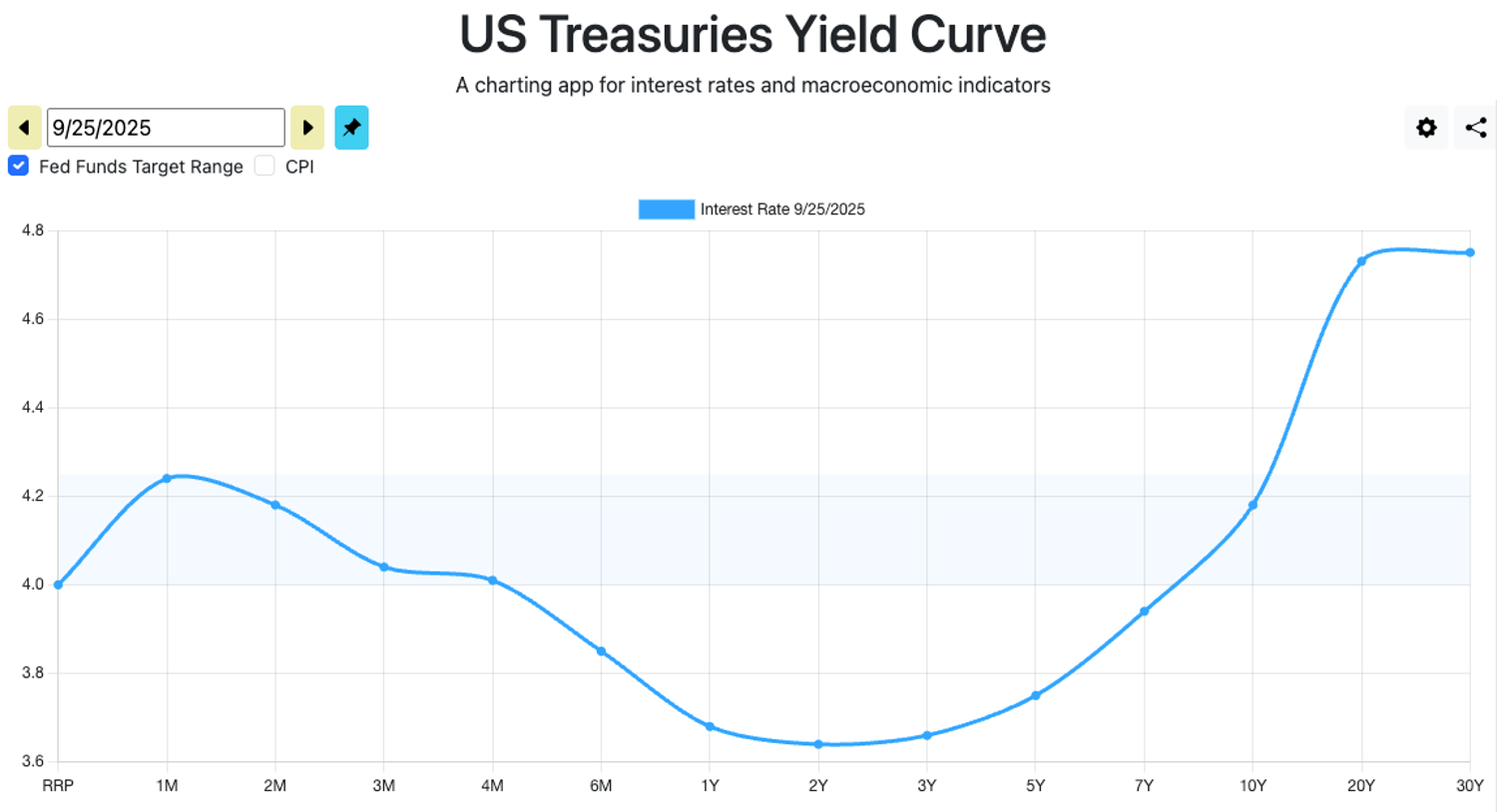

Do Long-term Interest Rates Still Matter?

The White House's focus on long-term rates is not without foundation. Long-term Treasury yields significantly influence billions in mortgage and commercial loan costs. Treasury Secretary Bessent, in a Wall Street Journal column, reiterated the Fed's three statutory objectives, criticising its "mission drift" and highlighting housing market stimulus as a top priority. Lisa Hornby, Schroders' US fixed-income head, concurred in an interview, noting the administration's endeavour to suppress long-term yields to bolster the economy.

However, it must be acknowledged that historically, the impact on long-term interest rates has been relatively uncommon. Fed interventions in long-term rates occurred during wartime or crises, such as yield controls during World War II or the 1960s' "Operation Twist." Gary Richardson, a University of California professor, notes that today's economy faces no such extremes, suggesting "intervention reflects Trump's personal agenda."

With US public debt soaring to $37.4 trillion and the budget deficit exceeding 6% of GDP, controlling long-term rates (the "YCC") may be the "only viable option" to address fiscal strain, according to the Trump administration. The White House may tolerate higher inflation to compel the Fed's compromise.

In fact, Bessent is already doing just that: T-bills are being issued at record levels, with yields far below the current federal funds rate. He also intends to use these funds to finance purchases of long-term Treasury bonds, thereby reducing his debt burden. However, this is akin to "paying a mortgage with a credit card limit"—replacing long-term debt with short-term debt results in a decline in long-term sovereign creditworthiness; banks would not lend to those who rely entirely on credit cards.

Source: ustreasuryyieldcurve.com

An even greater risk is that excessive T-bills can be converted to cash via T-bills finance, potentially flooding the market and daily life with money, and causing bubbles and a rebound in inflation. Since liquidity exists more in short-term rather than long-term forms, liquidity fluctuations will be more drastic, significantly impacting economic performance.

Traders also predict this. DWS Americas' George Catrambone has shifted from short-term to 10- and 20-year Treasuries, betting on yield declines; PIMCO's Daniel Ivascyn warns that a Fed-imposed rate cap could increase risks for shorting T-bonds, prompting his team to realise profits on short-term T-bills.

Carlyle Group warns that with core PCE above 2.5%, suppressing long-term rates could prove counterproductive. Earlier this year, expectations of Trump's stimulus policies pushed 10-year Treasury yields to 4.8% once; the current 4% level, though below the previous high, remains vulnerable to inflation risks amplified by Logan's toolkit overhaul — a TGCR shift could accelerate easing transmission, risking a 1970s-style expectation spiral.

TGCR: A Potential Compromise

On 25 September, Dallas Fed President Lorie K. Logan’s speech at the Richmond Fed’s CORE Week seminar further widened the rift in the Fed. She advocated modernising the FOMC’s operating target rate, urging a shift from the fragile federal funds rate to the more robust Tri-Party General Collateral Rate (TGCR) to enhance monetary policy resilience.

Logan emphasised that this change would not disrupt the Fed’s balance sheet normalisation but could improve short-term rate control through existing mechanisms, such as overnight reverse repurchase agreements and standing repurchase facilities, avoiding rushed decisions during crises.

Whilst not directly addressing long-term rates, Logan’s proposal suggests a potential technical foundation for future yield curve management under the “third mandate,” yet it also underscores hawkish concerns about political interference undermining the Fed’s autonomy.

Logan’s hawkish tone echoed her historical caution, referencing the 1970s when the Fed curbed inflation through money supply control, subtly warning that ill-judged tool adjustments could destabilise inflation expectations. This contrasts sharply with Miran’s aggressive stance, further fragmenting the FOMC. Bloomberg reports traders view Logan’s proposal as a “toolkit enhancement,” potentially strengthening the Fed’s long-term yield transmission but increasing near-term TGCR volatility pricing.

Potential mechanisms include the Treasury issuing more short-term bills whilst repurchasing longer-term bonds or the Fed resuming quantitative easing (QE). Though Bessent has critiqued QE, he concedes its use in “genuine emergencies.” Mark Spindel of Potomac River Capital is increasing holdings in short-term TIPS to hedge Fed autonomy risks, noting the vague “moderate rates” clause could justify any policy, particularly following Logan’s technical pivot.

Trump’s reshaping of the Fed is gaining momentum, with Miran’s “third mandate” push merely the opening move and Logan’s hawkish modernisation call injecting fresh uncertainty. Despite Powell’s insistence on independence, White House pressure is likely to intensify, leaving long-term rate paths unresolved. A TGCR shift could redefine monetary transmission, amplifying both inflation and debt risks. Traders are already positioning for tail risks — the market’s next moves merit close attention.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.