Ondo Business Lines, Model, and Revenue

| Product | Detail | Time |

| Flux Finance | Flux Finance — A decentralized lending protocol that supports tokenized U.S. Treasuries as collateral assets. | Jan 12. 2023 |

| OUSG | OUSG — A tokenized short-term U.S. Treasury fund, offering stable and transparent yield exposure to institutional investors. | Jan 26. 2023 |

| USDY | USDY — A permissionless yield-bearing U.S. dollar stablecoin, backed by bank deposits and short-term U.S. Treasuries. | Aug 03. 2023 |

| ONDO Token | ONDO Token — The governance and utility token of the Ondo ecosystem, enabling participation, staking, and alignment of incentives. | Jan 2024 |

| Ondo Global Market | Ondo Global Market — A platform that facilitates tokenized U.S. equities and ETFs, offering 24/7 trading and instant minting/redemption. | Sep 03. 2025 |

| Ondo Chain | Ondo Chain — A Layer 1 blockchain purpose-built for institutional-grade Real World Assets (RWA), currently in public testnet phase. | - |

Ondo operates multiple product lines targeting distinct layers of the RWA value stack, progressing from liquid, low-risk assets to complex tokenized securities and financial infrastructure products. This roadmap follows a clear “liquidity-to-utility” expansion logic, advancing sequentially from Stablecoins → Tokenized Treasuries → Tokenized Equities/ETFs → Multi-Chain Settlement Infrastructure.

The company views stablecoins as a proof of concept for the usability of on-chain assets, demonstrating that blockchain-based settlement can function at scale. However, meaningful efficiency gains and user experience improvements are expected to arise from more sophisticated instruments such as treasuries, ETFs, and equities. In this framework, stablecoins serve as the entry point for liquidity bootstrapping and user onboarding, while tokenized treasuries act as a bridge toward fully on-chain securities.

The next phase of development focuses on tokenizing high-liquidity equities, directly connecting traditional market makers and brokers to blockchain networks. By enabling 24/5 mint–redeem operations and 24/7 secondary trading, Ondo aims to make equities and ETFs composable components within the DeFi ecosystem, substantially expanding the on-chain asset universe and extending trading hours for digital finance.

To achieve true usability of these securities, complementary financial protocols—including lending, repo, derivatives, and collateral frameworks—must evolve in parallel. Flux Finance, Ondo’s lending platform, serves as a proof of concept that tokenized securities can function as collateral within DeFi, enabling a recyclable liquidity loop.

USDY — Yield-Bearing Stablecoin

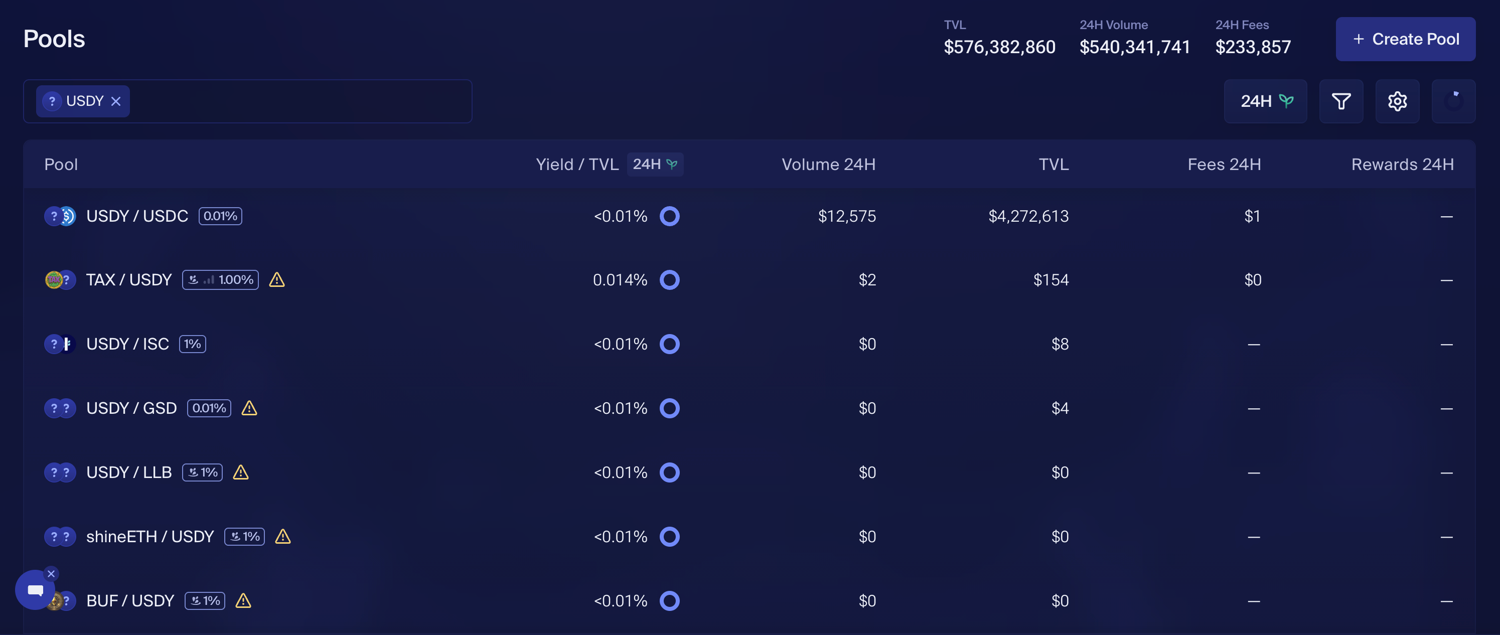

USDY is a yield-bearing stablecoin collateralized by bank deposits and short-term U.S. Treasuries. While primary issuance is restricted to KYC-verified investors, secondary market transfers remain permissionless, ensuring broader accessibility within DeFi. Ondo generates revenue by earning yield from the underlying assets, distributing the majority to holders while retaining a small interest spread and charging a 20 bps redemption fee as its primary income source.

As of September 2025, USDY distributed an annualized yield of approximately 4.2% to holders. Based on this rate, Ondo’s net interest margin stood at roughly 0.09%, translating to around $52,000 in monthly spread income. Including redemption fees—approximately $2,800 in August from 1.28 million USDY redeemed—the total monthly revenue generated by the USDY product line was about $54,000.

On the distribution side, USDY’s channel penetration remains limited, with primary listings on Bybit ($1 million in deposits) and Orca ($1 million in deposits). While most tokens are held on-chain, secondary market liquidity remains relatively weak, with daily trading volumes fluctuating between $300,000 and $1 million across CEX and DEX platforms.

Despite offering treasury-backed yields and permissionless secondary transfers, USDY’s adoption and transaction volumes remain subdued. This highlights a fundamental challenge in stablecoin distribution — even established issuers such as Circle incur substantial costs to secure listings, integrations, and liquidity partnerships.

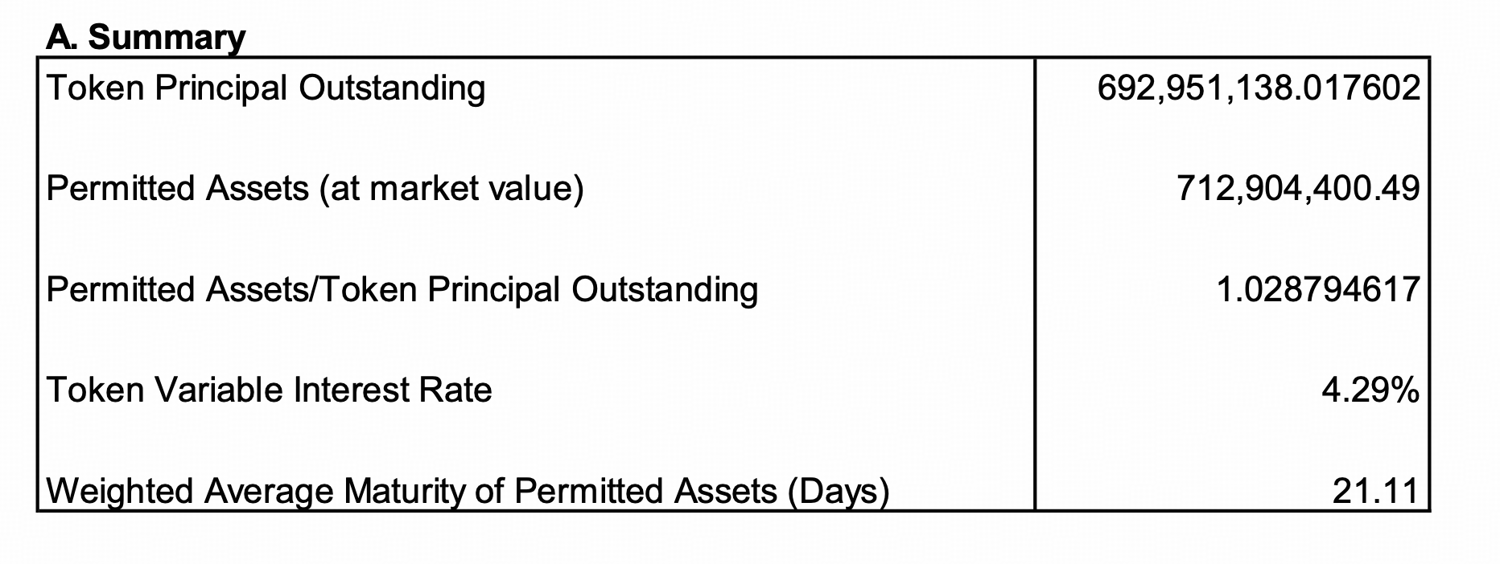

OUSG

OUSG is a tokenized short-term U.S. Treasury fund available exclusively to qualified institutional investors. The fund carries a management fee cap of 0.15%, though this fee has been waived through January 1, 2026 — a policy that has already been extended multiple times to encourage institutional adoption.

Operational expenses for OUSG primarily comprise administrative, legal, professional, and operating fees, with no active management fee accrued at the fund level. As a result, OUSG currently generates no direct revenue for Ondo — all interest income is capitalized into the fund’s NAV, benefiting investors rather than the issuer.

This structure highlights Ondo’s deliberate focus on scale over short-term profitability. The OUSG product line is designed to expand assets under management (AUM) and enhance institutional credibility, rather than to optimize revenue generation. In this sense, Ondo’s positioning aligns more closely with that of a financial infrastructure provider, emphasizing trust, compliance, and ecosystem durability as key components of its long-term competitive moat.

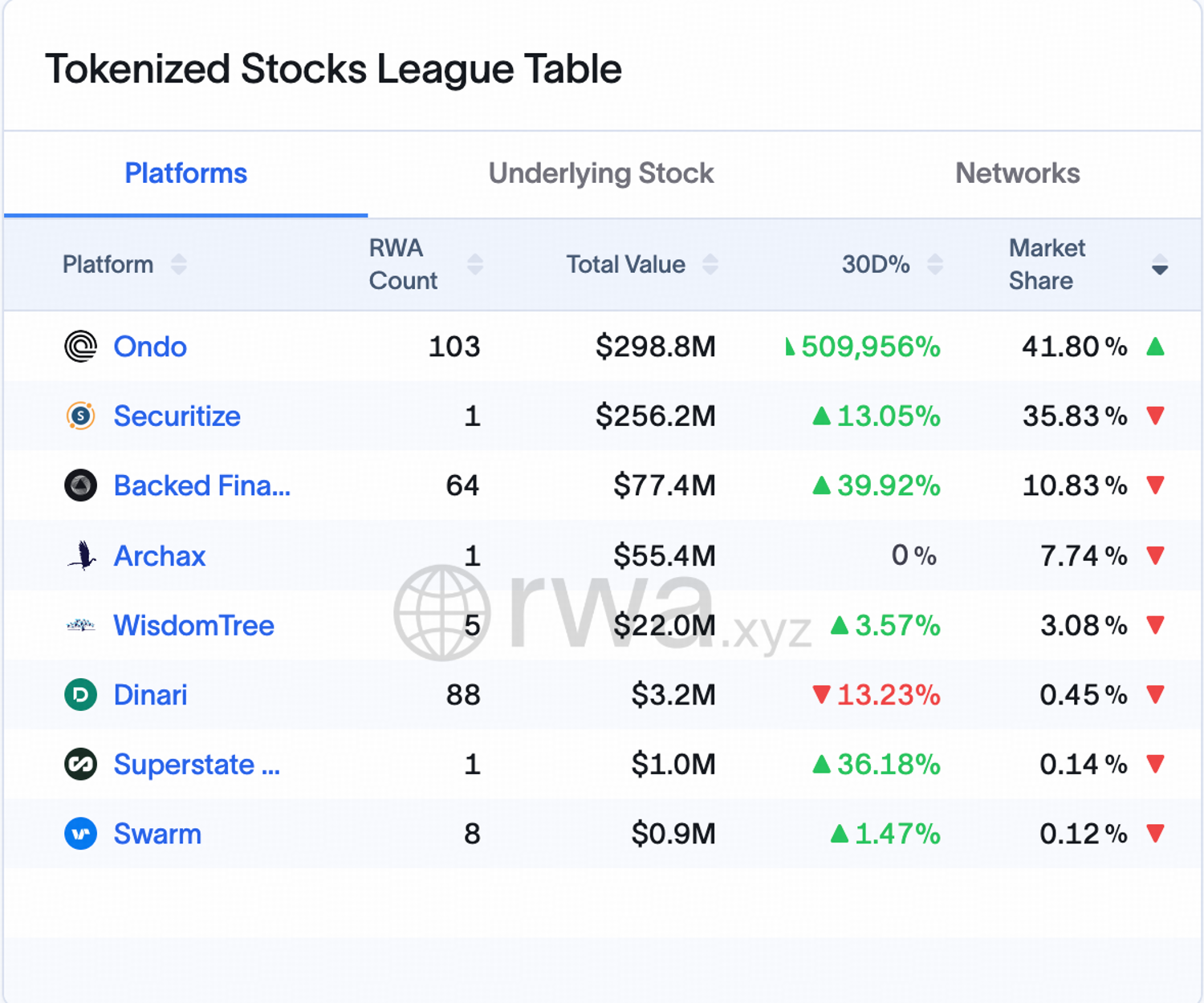

Ondo Global Market

Ondo Global Market (GM) serves as an on-chain issuance and redemption platform for tokenized U.S. equities and ETFs, functioning as a primary market facilitator rather than a full-fledged exchange. The platform supports 24/5 mint–redeem operations and 24/7 secondary trading through partnered exchanges.

Liquidity is primarily sourced from traditional equity markets, with mint and burn operations occurring almost instantaneously. While institutional investors must complete KYC verification on Ondo’s native platform, retail users gain access through partnerships with Kraken, Bybit, and Gate.io, which integrate KYC within their own systems. In this model, GM acts as a primary issuer, connecting institutional liquidity providers who then redistribute tokenized assets into secondary markets.

Currently, Ondo charges no fees for minting, redemption, or asset management; users only incur blockchain gas fees. The only potential revenue stream derives from price spreads between tokenized asset quotes and the underlying market prices. In practice, minor discrepancies between buy and sell quotes on GM and the underlying equities are captured as spread income by the platform.

This model underscores Ondo’s broader strategic alignment with crypto market dynamics, where valuation premiums often reflect ecosystem positioning rather than immediate profitability. By prioritizing market share, ecosystem integration, and product scalability over near-term revenue, Ondo reinforces its role as a foundational infrastructure player within the on-chain RWA ecosystem—a positioning that also influences the market valuation of its native token.

This approach aligns closely with crypto-native valuation frameworks, where token price and ecosystem positioning carry greater weight than short-term revenue metrics. By emphasizing network expansion and market share acquisition, Ondo positions its native token (ONDO) as a growth proxy rather than a profit-generating asset, reflecting a long-term, infrastructure-driven value narrative.

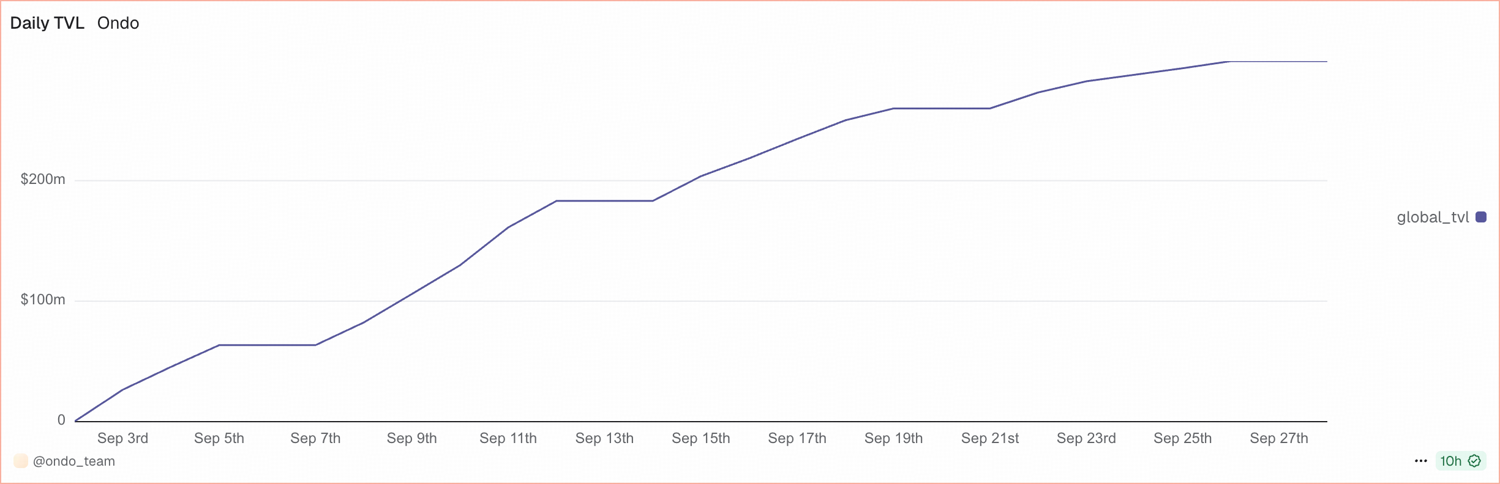

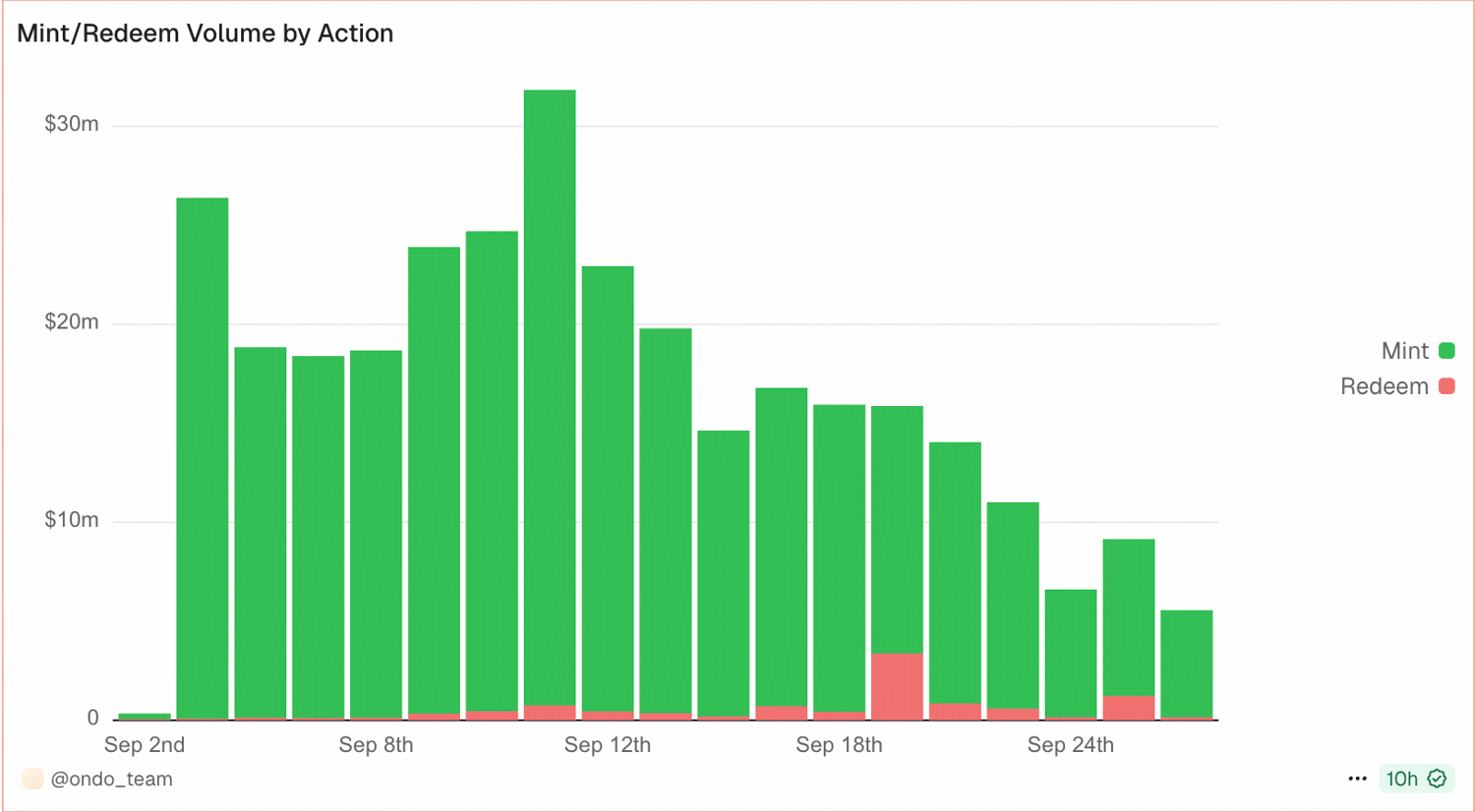

Ondo Global Market (GM) has achieved rapid initial traction, capturing approximately 45% of the tokenized equities market share and reaching a TVL of over $300 million within its first month of launch (since September 3, 2025). However, trading demand remains subdued, with weekly volumes trending downward, highlighting a disconnect between infrastructure maturity and actual user adoption.

DeFi Integration: Flux Finance

At the core of Ondo’s long-term vision lies the integration of real-world assets (RWA) with DeFi-native liquidity. To advance this objective, Ondo launched Flux Finance, a decentralized lending protocol that accepts tokenized U.S. Treasuries (OUSG) as collateral.

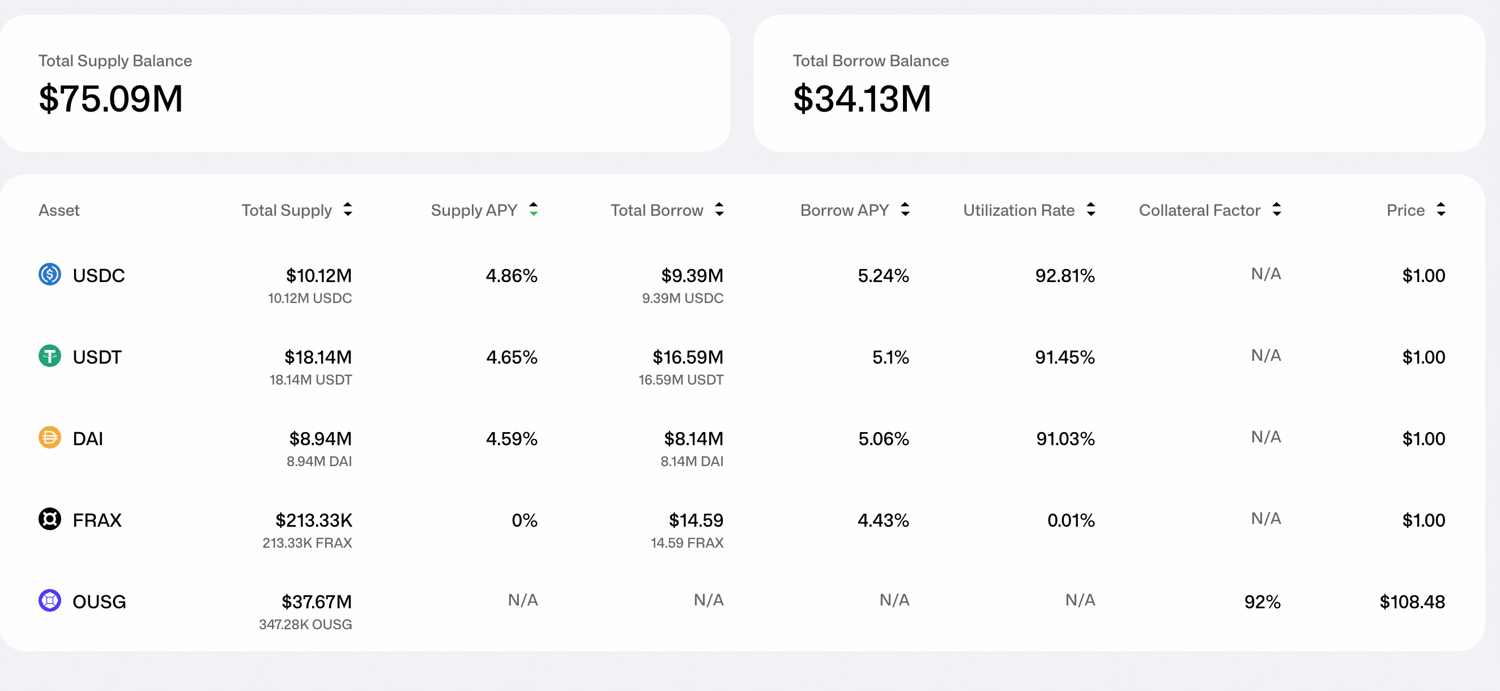

Since OUSG is a regulated instrument requiring KYC verification for both primary and secondary transfers, it demands a compliant DeFi infrastructure to enable controlled on-chain participation. Flux Finance fulfills this role as a bridge layer, facilitating secure and compliant interaction between institutional-grade RWAs and open DeFi protocols. As of October 13, 2025, OUSG collateral deposits on Flux Finance reached $37.67 million, reflecting early but tangible adoption of on-chain treasury-backed lending.

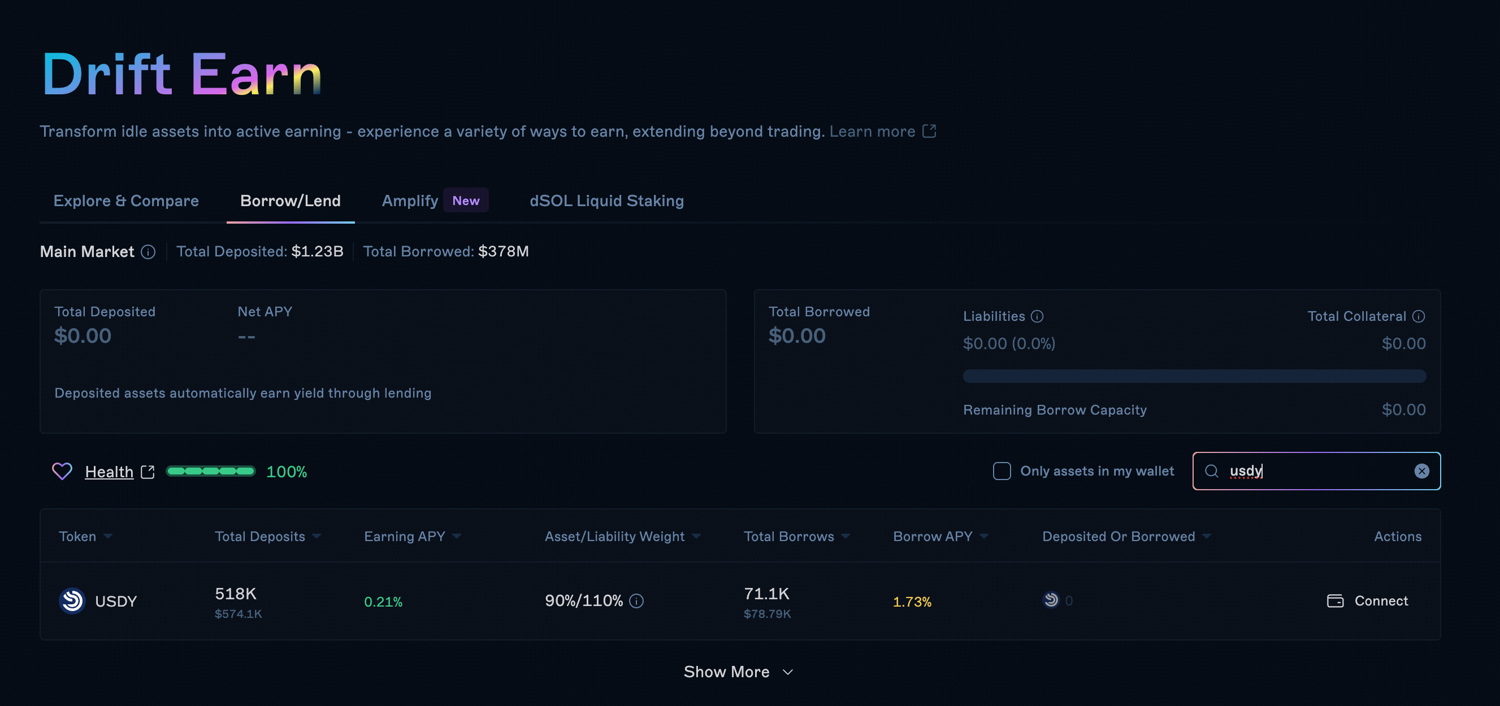

In parallel, USDY serves as a permissionless, yield-bearing stablecoin, designed for free circulation across DeFi without regulatory gating. For instance, Drift Protocol now supports USDY as collateral for lending and derivatives trading. Backed by U.S. Treasuries and featuring a native yield mechanism, USDY is highly composable across CEXs and DeFi ecosystems—notably with Bybit, where USDY trading pairs have already been launched.

However, despite technical readiness and integrations, both trading and borrowing demand remain muted—a result of limited distribution channels and low retail awareness of RWA-linked stablecoins. Ultimately, Ondo’s success in expanding USDY’s presence across DeFi and exchange ecosystems will determine whether its liquidity strategy can effectively counter declining fixed-income yields amid a shifting macro environment.

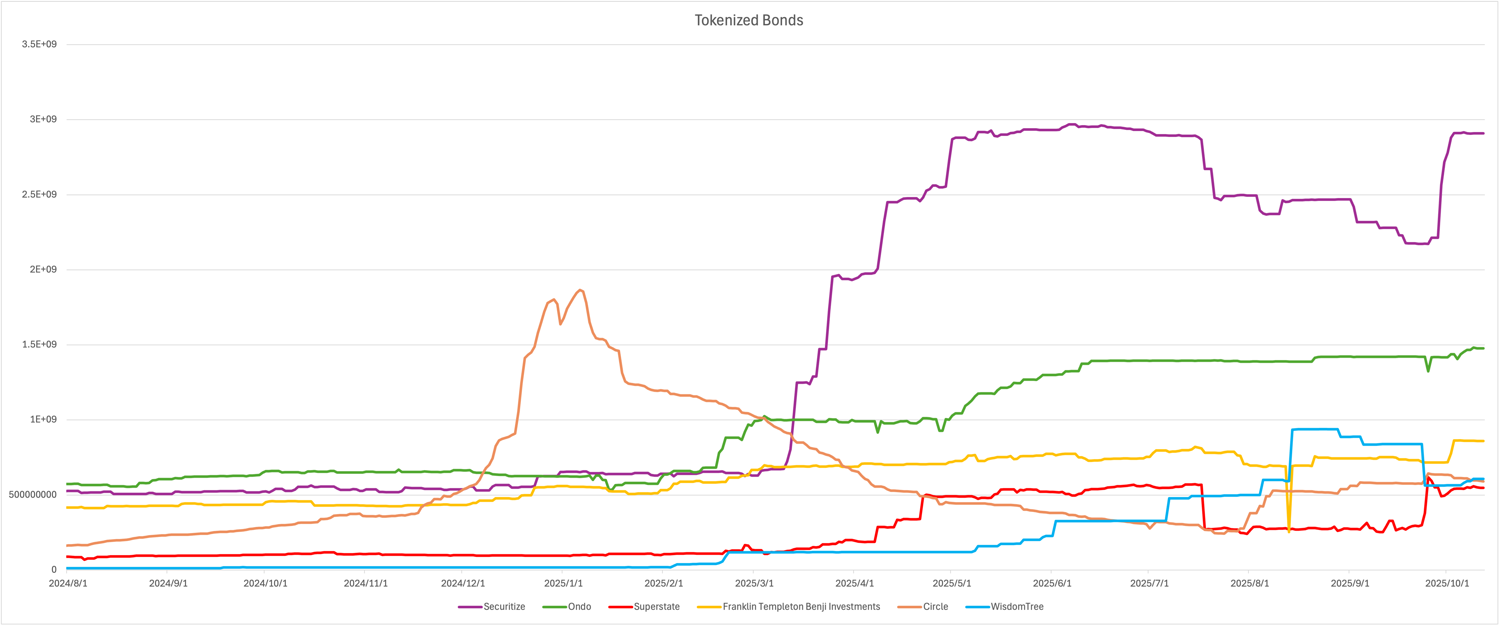

Short to Mid Term Outlook

Among the top five issuers of tokenized U.S. Treasury–backed products, Securitize currently leads the market through its BUIDL product, while Ondo Finance ranks second overall, serving as a key distribution partner for both BUIDL and Benji.

From a macroeconomic perspective, the tokenized bond market has entered a rate-cut cycle. This environment implies declining demand for tokenized Treasuries, as their yield advantage compresses in tandem with falling interest rates. Ondo’s strategic response centers on deepening DeFi integration — linking on-chain liquidity protocols to unlock additional yield sources beyond traditional Treasuries. By enhancing DeFi utility, Ondo can partially offset yield compression within its RWA product suite. Without such integration, issuance volumes are likely to remain under pressure.

From a business model perspective, Ondo’s near-term focus remains on AUM expansion rather than monetizing existing assets through management fees. Due to the structural characteristics of yield-bearing stablecoins, AUM-based profit margins are inherently limited.

For comparison, Circle’s Q2 2025 financial report indicated $61 billion in managed assets, generating an annualized reserve yield of 4.1% and quarterly reserve revenue of $634 million (total revenue: $658 million). After adjusting for IPO and equity compensation effects, Circle reported an EBITDA margin of roughly 50%.

By contrast, Ondo distributes nearly all yield to holders, retaining only minimal spread income. This approach substantially reduces profit margins relative to peers such as Tether and Circle. As a result, Ondo lacks surplus cash flow to fund liquidity incentives or secondary market support across CEXs and DeFi venues. This structural limitation helps explain USDY’s slower adoption and shallow trading depth, despite its inherent yield advantage and robust collateral backing.

Secondary Market Analysis

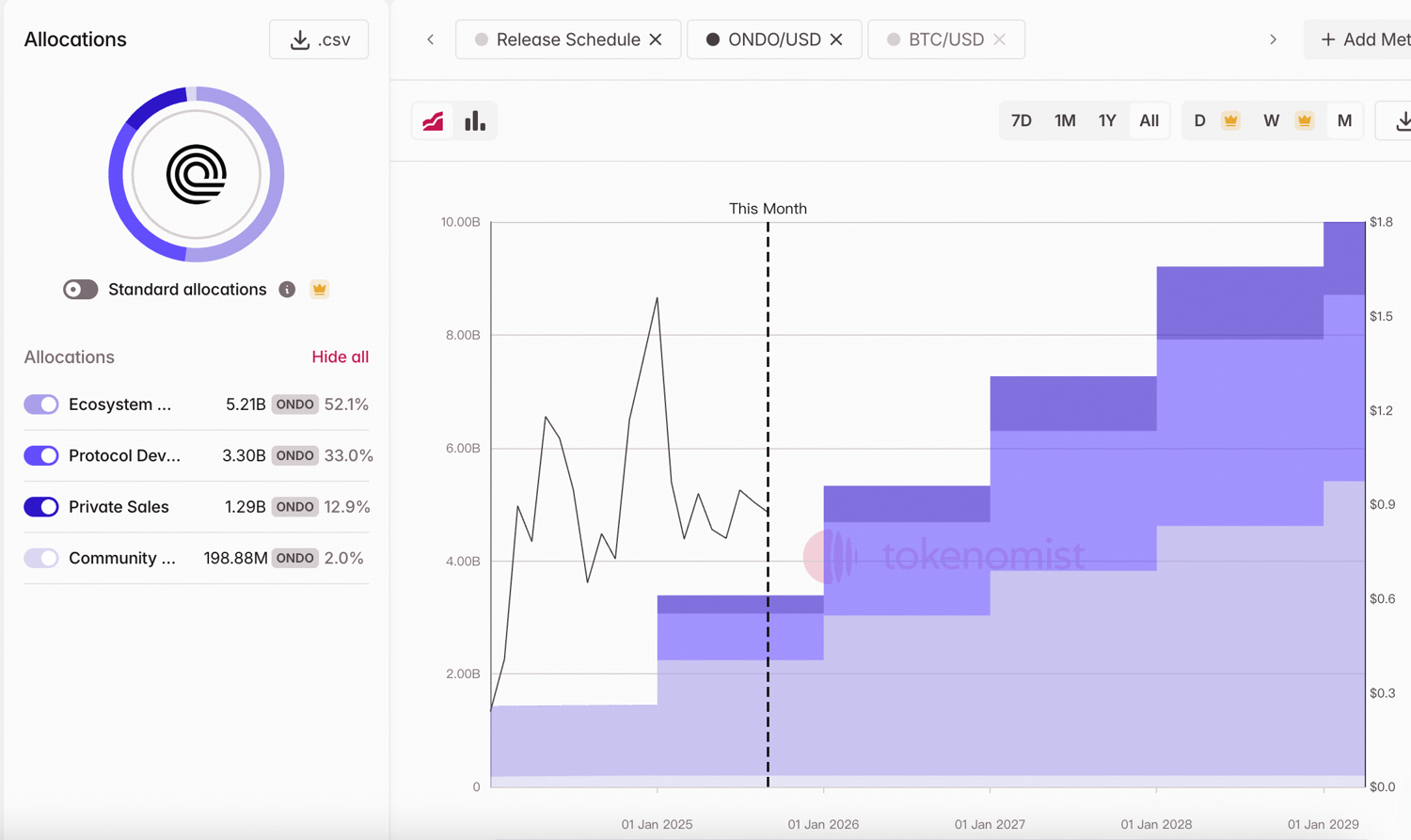

Ondo Finance has a total token supply of 10 billion ONDO, with approximately 3.38 billion tokens in circulation as of October 16, 2025. The initial token allocation is structured as follows:

Initial Circulating Supply: 1,426,647,567 (~14.3%), including 2% from CoinList sales and 12.5% reserved for ecosystem incentives.

Community Access Sale: 198,884,411 (~2.0%).

Ecosystem Growth: 5,210,869,545 (~52.1%).

Protocol Development: 3,300,000 (~33.0%).

Private Sales: 1,290,246,044 (~12.9%).

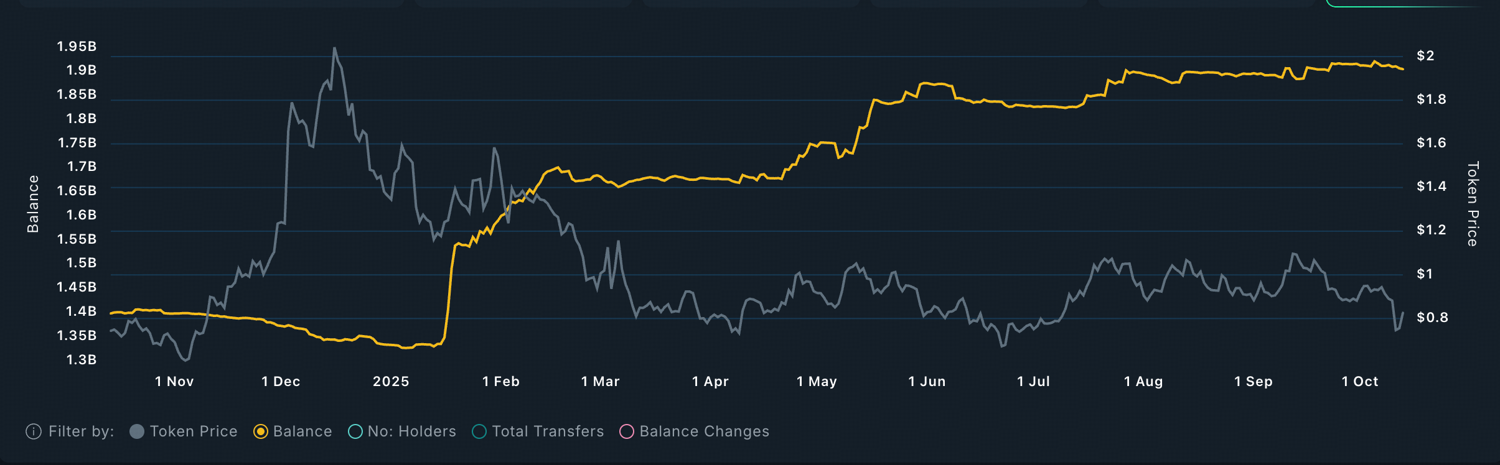

Ondo is approaching a major token unlock event that could have a significant impact on market dynamics. According to TokenUnlocks, approximately 1.94 billion ONDO tokens—valued at roughly $1.8 billion based on the current price of $0.824 per ONDO—are scheduled to unlock in January 2026. Of this total, around $260 million worth of tokens will be released from primary market sales, while approximately $680 million will come from the protocol development foundation. This large-scale unlock introduces the potential for substantial sell-side pressure in the coming months, particularly in the absence of strong secondary demand or offsetting liquidity programs.

From a fundraising standpoint, Ondo Finance has completed four rounds of financing, including two public sales. The project’s Token Generation Event (TGE) took place in January 2024 through the Bybit Launchpad. (Note: minor discrepancies exist between data reported by RootData and official figures.)

| Time | Round | Amount | Token | Value | Return October 16, 2025 | Investor |

| 2021.08 | Seed | 4m | ~7% | ~60m | ~ 137x | Pantera Capital*, Digital Currency Group, Bixin Ventures, CoinFund, Chapter One, Divergence Ventures, The LAO, Protoscale Capital , Stani Kulechov, Diogo Monica, Josh Hannah, Richard Ma, Justin Schmidt, Christy Choi |

| 2022.04 | A | 20m | ~7% | ~300m | ~ 28x | Pantera Capital*, Founders fund*, Coinbase Ventures, Tiger Global, Wintermute, GoldenTree Asset Management, Flow Traders |

| 2022.05 | Coinlist 1 | 3m | 0.3% | ~1b | ~ 8x | - |

| 2022.07 | Coinlist 2 | 5.4m | 1.7% | - | - | - |

| 2024.2.1 | Bybit Launchpool | 9m, | - | - | - |

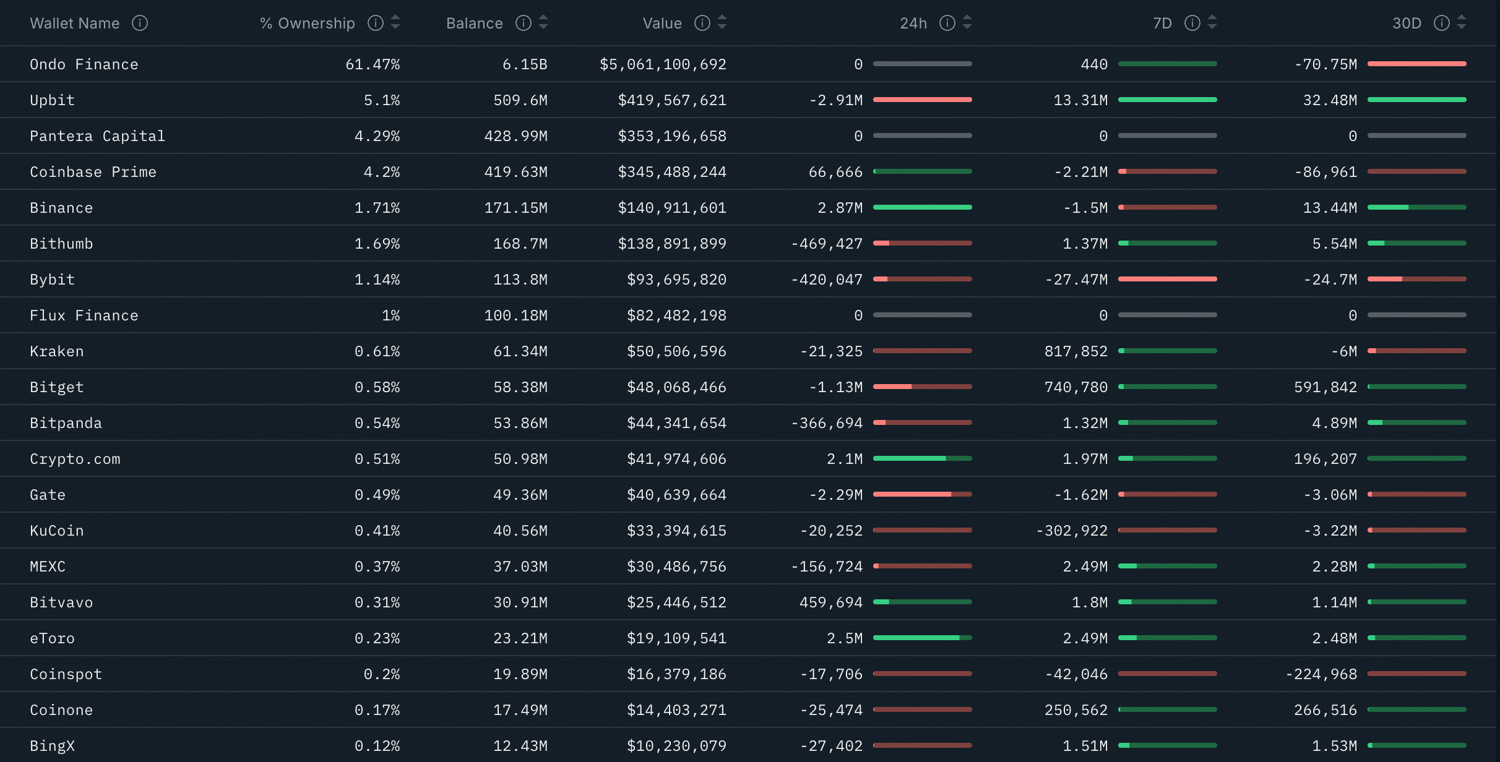

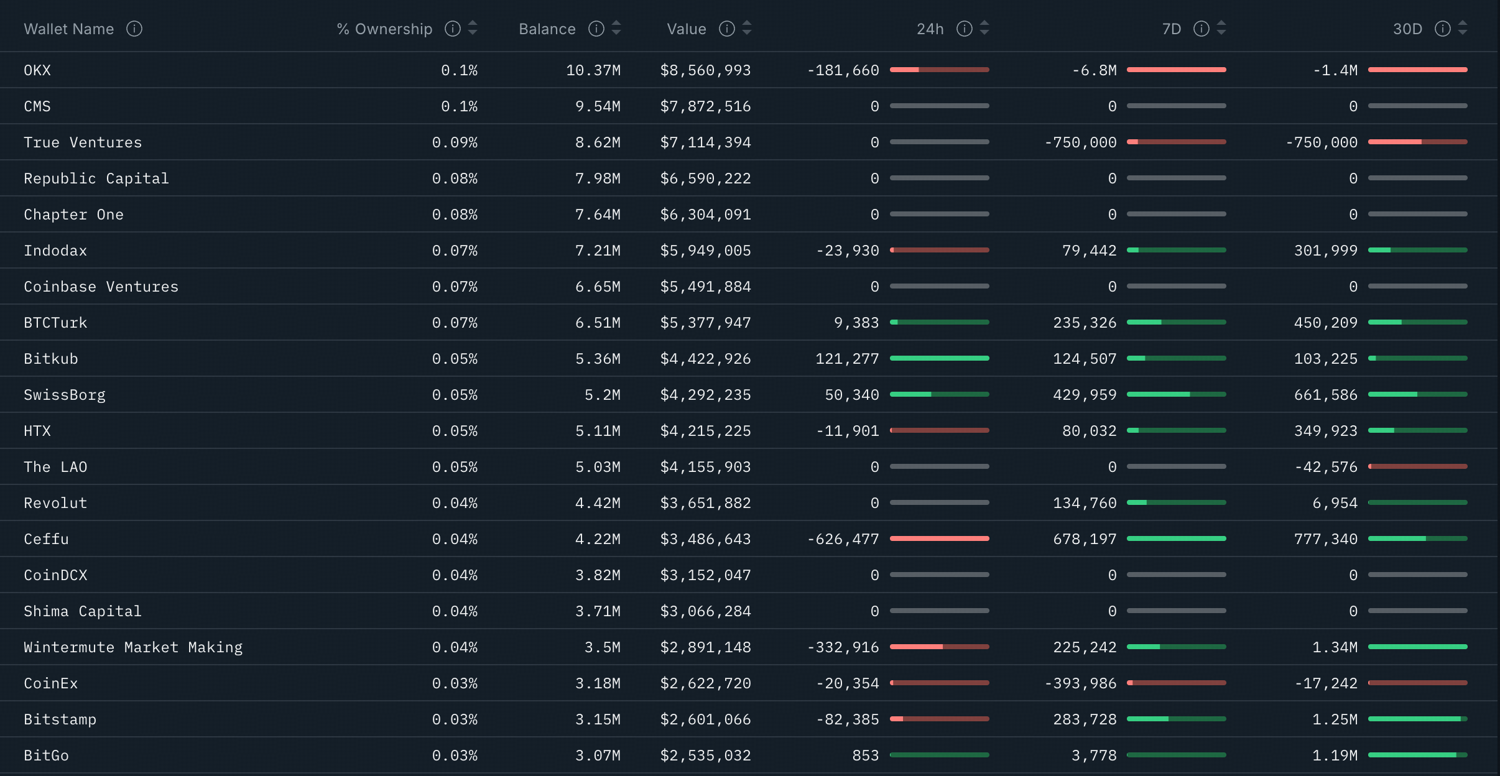

On-chain data indicates that Pantera Capital, the lead investor in both Ondo’s seed and Series A rounds, has achieved an estimated hundredfold return on investment (ROI) and currently holds approximately 4.29% of the total token supply, representing one of the largest institutional allocations. Other notable venture investors include CMS Holdings, True Ventures, Republic Capital, Chapter One, Coinbase Ventures, The LAO, Shima Capital, and Wintermute.

Among these, True Ventures has shown visible on-chain selling activity, while the remaining VCs appear to be maintaining their positions, suggesting limited early-stage profit-taking and a continued long-term holding stance across most institutional investors.